Is The Bear Market Over Already?

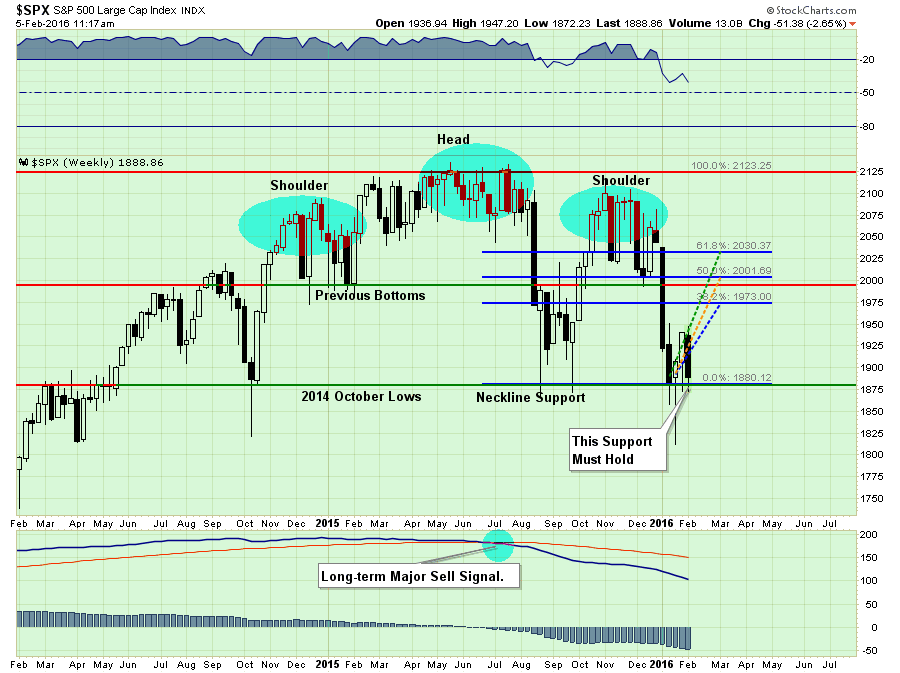

At the end of January, I discussed the potential for a reflexive rally in the markets and laid out three retracement levels at that time.

“The good news, if you want to call it that, is that the market is currently holding above the recent lows as short-term oversold conditions once again approach. It is critically important that the market holds above that support, which is also the neckline of the current “head and shoulders” formation, as a break would lead to a more substantive decline.”

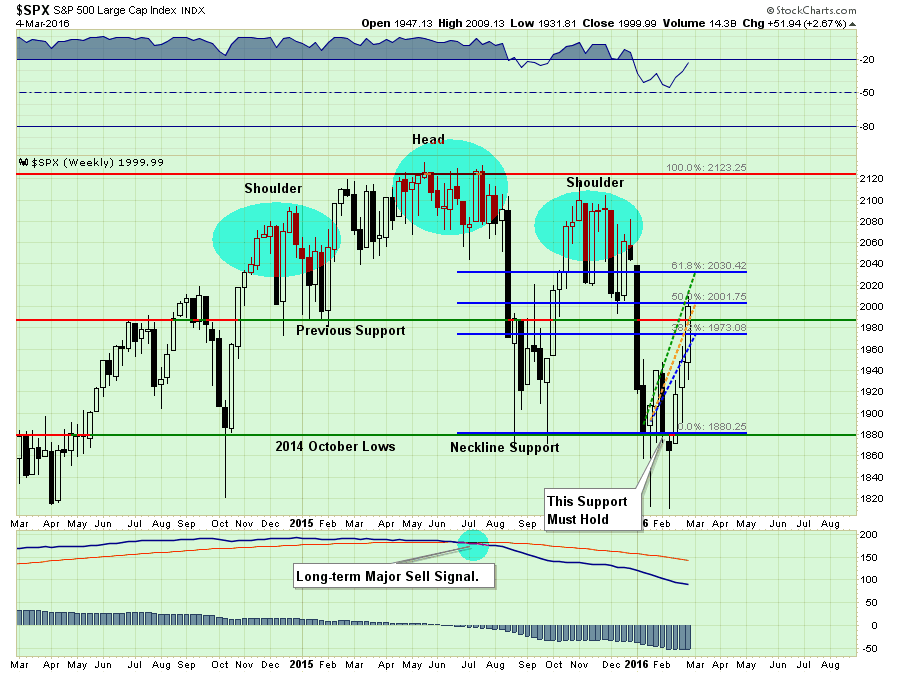

Here is the same chart updated through Friday’s close:

I pointed out last week that:

“The good news is that the market was able to break above 1940, and the 50-dma, which now clears the way for a push to the 1970-1990 where the next levels of resistance will be found.“

The markets were not only able to push into the 1970-1990 level last week but also complete a 50% retracement from the recent lows as shown above. The 8% advance from the closing lows just 4-weeks ago has sent “shorts” scrambling to cover pushing stock prices sharply higher.

But does this change any of the recent analysis?

I’M MISSING IT

“OMG!!! I am missing it. Don’t we need to be jumping back in?”

It is not surprising that the recent surge in the markets has awakened the “bullish spirits.” However, that is an emotionally based response to short-term market volatility rather than a decision to increase equity risk based on a defined and disciplined approach.

This goes to the heart of the portfolio management discipline and philosophy. The chart below shows the model allocation changes since 2013.

As you will note, portfolios have been grossly underweight equity related exposure since April of 2015 creating a positive performance gap between the index and the portfolio. That positive performance gap allows for a more relaxed approached to increasing portfolio allocations when the market re-establishes a positive price trend without sacrificing long-term performance.

The final reduction at the end of January protected portfolios from the decline in February, but has led to a minor performance drag over the last two weeks. But given that risk is still prevalent to the downside, I am willing to give up a potential “bear market rally” for the sake of protecting client capital from loss.

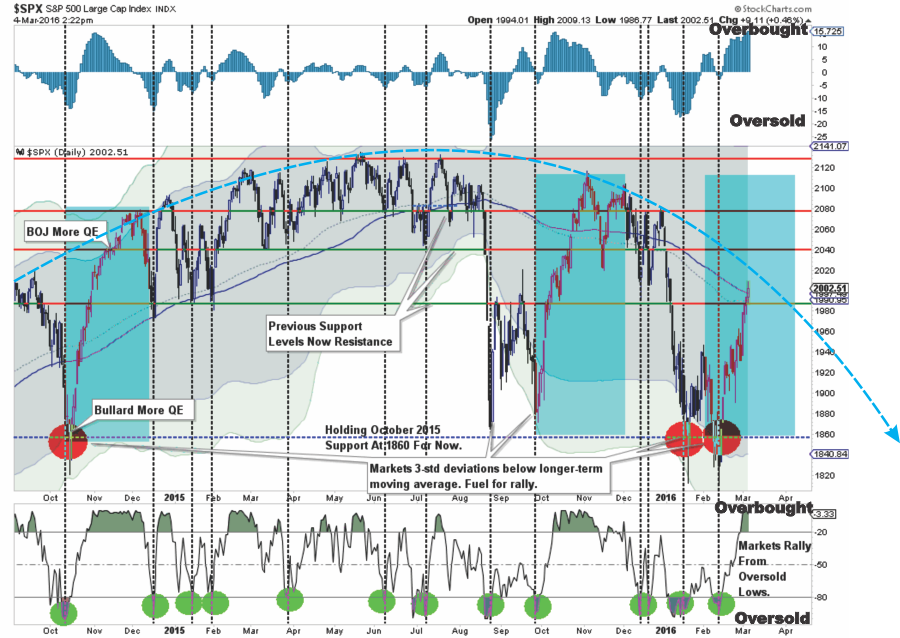

As I have stated before, when the market re-establishes a positive trend, I will recommend putting preserved capital back to work. However, for such an equity increase to be warranted, the market will need to break the current declining price trend and work off some of the currently extreme overbought conditions. This is shown in the updated chart from last week.

There are quite a few moving pieces here, so let me explain.

- The shaded areas represent 2 and 3-standard deviations of price movement from the 125-day moving average. I am using a longer-term moving average here to represent more extreme price extensions of the index. The last 4-times prices were 3-standard deviations below the moving average, the subsequent rallies were very sharp as short positions were forced to cover. The vertical blue bars show the previous two periods where bulls regained footing and pushed markets from lows towards new highs. The current setup is indeed similar to those previous two attempts.

- The top and bottom of the chart show the overbought/sold conditions of the market. The vertical dashed lines show that oversold conditions lead to fairly sharp rallies. The recent rally has responded as expected from recent oversold conditions. With the oversold condition now exhausted, the potential for further upside has been greatly reduced.

- With the 125-day moving average trading below the 150-dma, and with both averages declining rather than advancing, the easiest path for prices continues to be lower as downward resistance continues to be built. The arching dashed red line shows the change of overall advancing to now declining price trends.

The last sentence above is the most important. The signal to increase equity related exposure in portfolios will require a breakout above the currently negative price trend. Until that happens, we remain confined in a “bear” market.

Disclosure: The information contained in this article should not be construed as financial or investment advice on any subject matter. Streettalk Advisors, LLC expressly disclaims all liability in ...

more