Is It Time To Buy This Fast Food Chain?

Sonic Corp (SONC) Consumer Discretionary - Hotels, Restaurants & Leisure | Reports June 23, After Market Closes

Key Takeaways

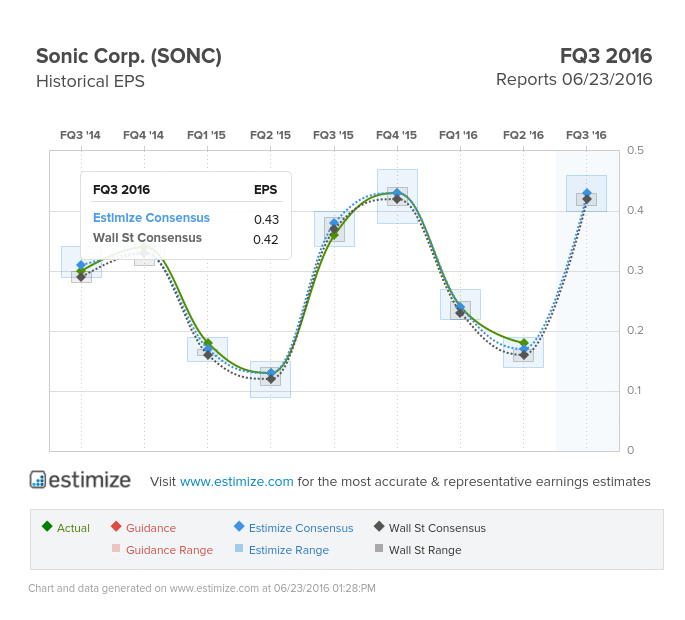

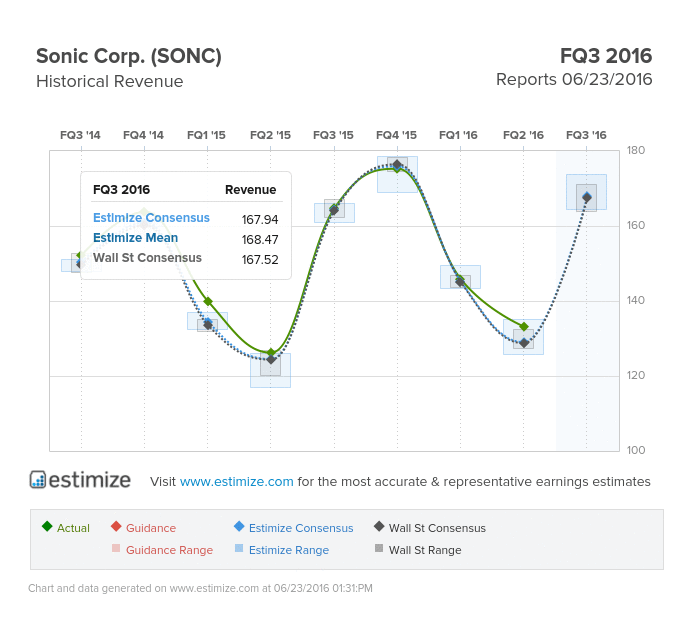

- The Estimize consensus is looking for earnings per share of 43 cents on $167.94 million, 1 cent higher than Wall Street on the bottom line and right in line on the top

- Sonic continues to see strength in core menu items, value based promotions and limited time items

- The company is indicating that same store sales would fall in the range of flat to a 4% increase, lower than reported in its annual guidance

Lately we are seeing a buying opportunity in the fast food space. The trends that favored fast casual 5 years ago are shifting back to fast food dining. This past earnings season we saw Yum Foods (YUM), McDonald’s (MCD), and Wendy’s (WEN) beat earnings expectations on increasing demand and rising comparable store sales. Sonic has its sight set high that tomorrow’s earnings will cause a spike in share prices

The Estimize consensus is looking for earnings per share of 43 cents on $167.94 million, 1 cent higher than Wall Street on the bottom line and right in line on the top. Compared to a year earlier this reflects a 19% increase in earnings with sales growing as much as 2%. Shares are currently down 10% year to date and typically don’t make any gains following a report.

Sonic is best known for its quick services restaurants that bring a nostalgic 1920’s drive in appeal at an inexpensive price. The company continues to see strength in core menu items, value based promotions and limited time items. The combination of sales leverage and a favorable commodity cost environment helped Sonic deliver a strong second quarter. Q2 featured a 6.5% increase in same store sales driven by 5 new store openings and improving margins. The company has invested heavily in technology initiatives to sustain its recent momentum and further differentiate themselves from its peers in the fast food industry.

Unfortunately, the company is already indicating softer same store sales trends. In May, management indicated same store sales would range from flat to a 4% increase lower than its annual guidance for growth of 4% to 6%. The company’s strengths such as growing net income, earnings a and expanding profit margins should be enough to outweigh weak operating cash flow and the early reports of declining sales.

Photo Credit: Mike Mozart

Disclosure: There can be no assurance that the information we considered is accurate or complete, nor can there be any assurance that our assumptions are correct.

Even if profits rise, softer sales at fast food stores tend to lower stock prices rather than raise them and are not a positive sign. Higher prices to offset such declines may help a quarter but tend to create a vicious cycle that ends badly. I think the company and analysts have overestimated its growth in the coming quarter being the company is indicating a miss. The stock should suffer.

In the long run, I hope the company does well, I like their burgers and will keep an eye on it. The fast food business is really getting brutal. Too much competition.