In early June, 30 hydrogen fuel cell buses have been put into operation in Zhangjiakou, China. Before that, the city has already had 710 HFCVs (hydrogen fuel cell vehicles) functioning during the Winter Olympics. There is no doubt that HFCVs are gradually entering modern Chinese society. Actually, as carbon neutral is becoming a consensus, the marketization of HFCVs is accelerating all over the world with its zero-carbon emission. According to Precedence Research, the global market for fuel cell electric vehicles will reach $35.6 billion by 2030.

Such a high demand needs more supply. So, to increase the productivity, which part of HFCV is the starting point?

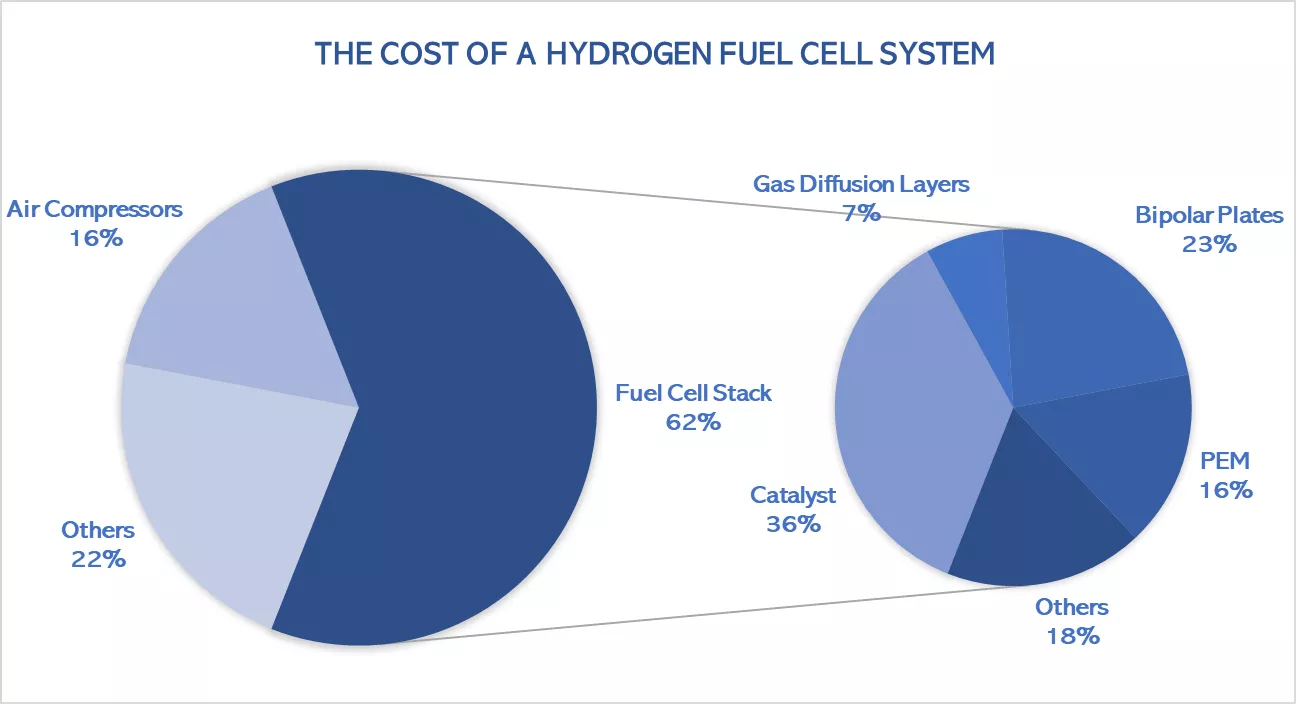

In terms of the cost of an HFCV, a hydrogen fuel cell system accounts for 40% and, within the system, PEM (Proton Exchange Membrane) is one of the most critical parts, which the hydrogen fuel cell, also called PEMFC (Proton Exchange Membrane Fuel Cell), is named for. However, R&D and production of PEMs are both costly and, consequently, constrain the mass production of PEMFCs and HFCVs. In other words, the starting point of marketization of HFCVs is the large-scale production of PEMs.

Source: China EV100

Chinese enterprises are speeding up to break monopoly in PEM market

Currently, PFSAPEM (Perfluorosulfonic Acid Proton Exchange Membrane) is the mainstream for hydrogen fuel cells, which can effectively improve battery efficiency with its strong proton conductivity and stability. However, this type of PEMs is made of perfluorosulfonic acid resins and, the technological requirement of fluoridation is extremely high. Hence, only a few companies are competent to produce PEMs on a large scale, making the market monopolized until now. Nowadays, Chemours (NYSE: CC) and Gore have the largest shares in PEM market, while 3M (NYSE: MMM), Solvay and others are also major suppliers.

In China, although PEM is a new field, under the support of government, R&D progress is fast. Up to now, some companies have already been able to mass produce commercial fuel cell PEMs, showing the ability of preliminary localization. Among them, Dongyue Group Limited (00189.HK) is the largest and, has a relatively complete PFSAPEM supply chain.

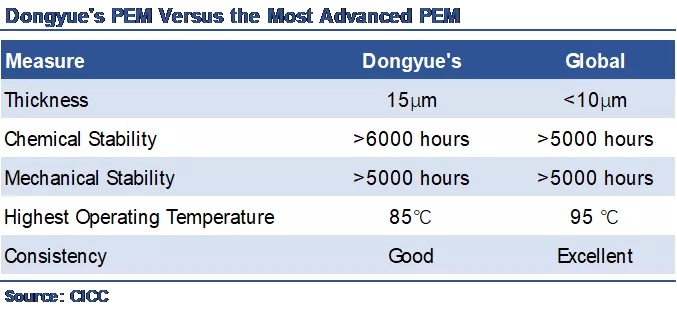

In 2020, Dongyue's new PEM project with an annual output of 1.5 million square meters was officially put into operation, of which the quantity of PEMs for fuel cells reached 0.5 million square meters, realizing mass production successfully. Although there is still a technological gap between Dongyue’s PEMs and the most advanced PEMs, the gap is acceptable in general, and it indicates a great potential to develop. Then, if the gap can be further shortened to ramp up the production of PEMs, the mass production of HFCVs in China will be strongly propelled.

Increasing demand for new methods to produce PEM

Nowadays, PEM manufacturers are going to change from PFSAPEM to other types, due to its high production cost, difficult monomer synthesis and instable proton conductivity when temperatures rise. Recently, partially fluorinated PEMs, non-fluorine PEMs and compound PEMs are main directions.

- Non-fluorine PEM

At present, non-fluorine PEMs are mostly made up of sulfonated aromatic polymers. This kind of PEMs has high stability, low price and is easy to be processed. However, its short service life cannot meet the requirement of HFCVs.

- Partially fluorinated PEM

BAM3G is one of the most successful partially fluorinated PEMs, it is invented by Ballard Power Systems Inc (Nasdaq: BLDP) and has higher thermal stability, lower price but remains hard to produce.

- Compound PEM

In the field of compound PEM, Gore's SELECT is the representative. It has better dimensional stability and less perfluorinated resins, reducing the cost of raw materials.

To conclude, in the long run, all of these new directions are likely to improve product performance and reduce costs effectively, while they still need further research. For instance, provided that materials which have the same characteristics as sulfonated aromatic polymers but longer service life are founded, then the production cost of PEMs will be greatly reduced.

As for China, because of insufficient R&D experience in PFSAPEM, it is difficult to take over the lead. In order to increase the market share of domestic products for PEMs, Chinese company should accelerate the technological breakthrough in the new directions of PEM as well as PFSAPEM, striving to lead the new market.

Growing demand and political support boost the localization of PEMs

Since Chinese government announced carbon neutrality target, plenty of automobile companies in China have entered HFCVs market proactively. According to Liu Kun, a strategic consultant of Great Wall Motor Co., Ltd. (02333.HK), 2021~2023 is a strategic opportunity for enterprises to deploy HFCV business.

The active downstream industry drives the growth of PEM demand. As CITIC Securities predicted, the total quantity of HFCVs in China will reach 100,000 in 2025, and the total consumption of PEMs for fuel cell will reach 1.8 million m², with a market size of 1.8 billion RMB.

Such a high demand for PEMs stimulates head companies to aim at Chinese market. Several PEM manufacturers have invested in China and build factories recent years. Some of them also cooperate with Chinese automobile companies, trying to seize the development opportunities.

For domestic PEM manufacturers, although their competitors have ampler R&D experience, the policy support will give them an edge.

In March 2022, NDRC of China announced Medium and long-term plan for the development of hydrogen energy industry (2021-2035), which made arrangements for PEMFC industry. It clearly pointed out that the government will provide financial support for hydrogen-related industries and propel technological innovation of PEMFC. With the support of policy and the breakthrough of PEM technology, the share of local products in Chinese PEM market will be greatly increased. Finally, the huge demand gap of PEM for fuel cells in China will be gradually completed by local companies.

Conclusion

In summary, as the key to the commercialization of HFCVs, PEM industry will thrive. Chinese enterprises now have broken the monopoly in the domestic market to some extents but, to further expand, they still need to seek for technological breakthrough in new directions. Besides, the expansion of domestic demand and policy support also give Chinese enterprises more space to develop. So, Chinese PEM manufacturers, such as Valiant Co., Ltd. (002643.SZ) and Dongyue, are expected to embrace rapid growth.

More By This Author:

Li Auto Goes From Strength To Strength. Here’s Why!

How Did Li Auto Perform In The First Quarter?

Tracking HP After It Tied The Knot With Buffett’s Berkshire Hathaway

Comments

Log in or sign up to join the conversation.