Thursday’s Commentary led with a discussion of how sales at major retailers were slowing appreciably. The takeaway from the piece is that personal consumption, accounting for two-thirds of GDP, is slowing. A reader emailed us, “Not so fast with your judgment. “You may be right, but you should also look at spending on food for confirmation.” We agree. Grocery stores, restaurants, and beverage and food distributors can provide more clarity about personal consumption trends.

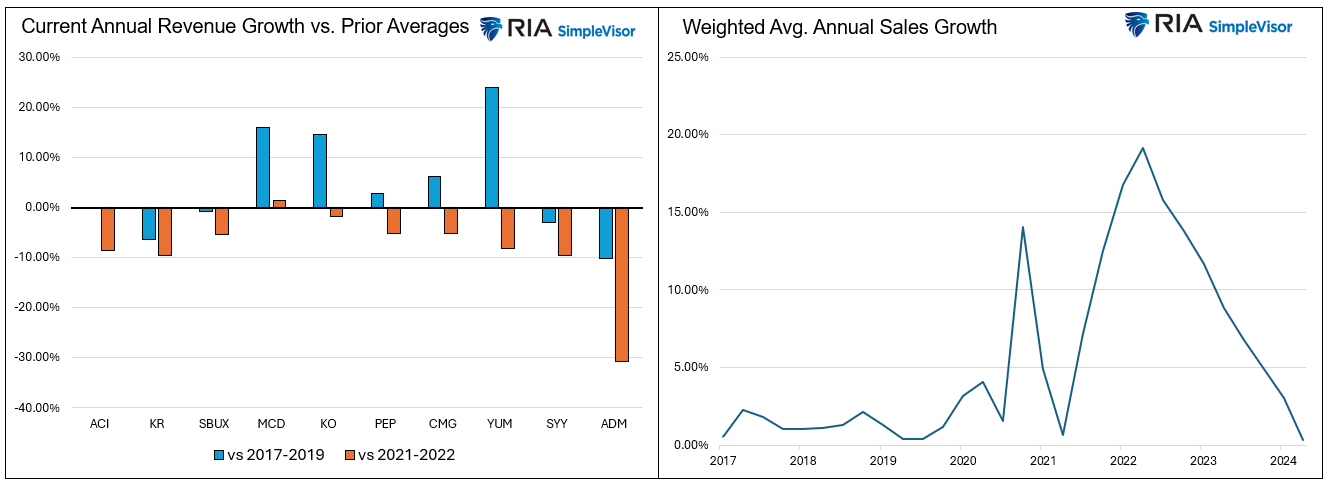

Our food analysis, shown below, is based on sales from the following companies: Albertsons (ACI- data since 2020), Kroger’s (KR), Starbucks (SBUX), McDonald’s (MCD), Coke (KO), Pepsi (PEP), Chipotle (CMG), YUM Brands (YUM), Sysco (SYY), and ADM (ADM). We took the same approach and compared each company’s current annual revenue growth to 2021-2022 and the three years before the pandemic. We also weighted their revenue growth and calculated a weighted aggregate sales growth. Remember that the graphs and the results from the first Commentary do not account for inflation.

The first graph shows that five of the nine food companies have higher sales growth today than in the pre-pandemic period (we exclude ACI as there is no data for the period). However, all ten companies except McDonald’s have lower sales growth than in 2021-2022. The graph on the right shows that the weighted annual sales growth is now the lowest since 2017. This analysis confirms our prior work that personal consumption growth has slowed considerably. Now, considering inflation is about 2% higher than in the pre-pandemic period, our thesis strengthens.

(Click on image to enlarge)

What To Watch Today

Earnings

- No notable earnings announcements\

Economy

(Click on image to enlarge)

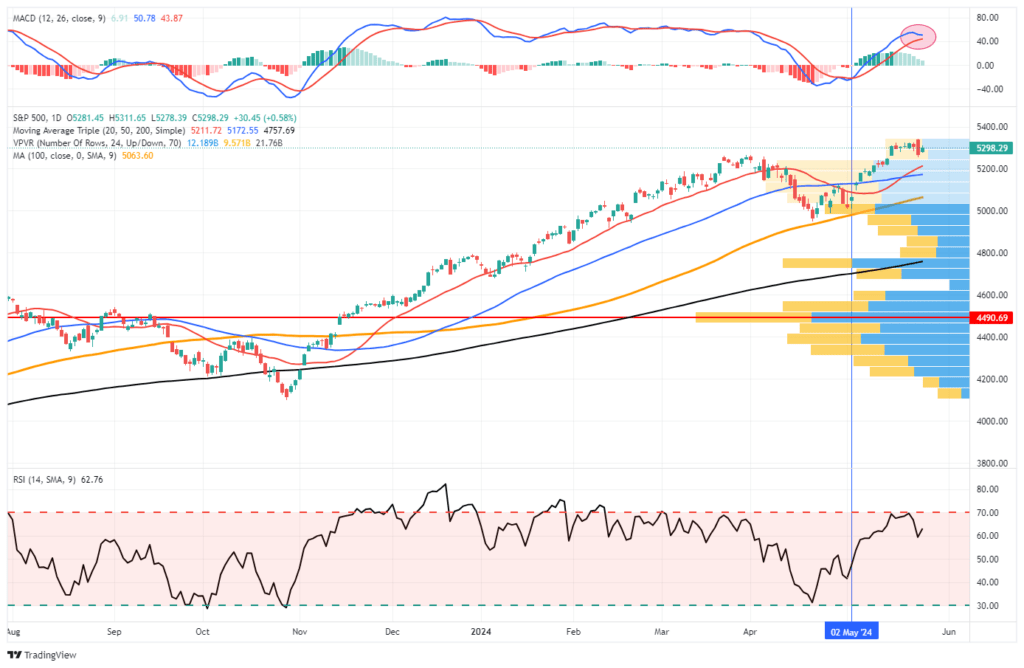

Market Trading Update

Last week, we discussed that the markets surged to all-time highs as a plethora of bad economic data and a weaker-than-expected inflation print lifted hopes of Fed rate cuts in the coming months. Over the last few trading days, the markets had to focus on the minutes from the last FOMC meeting and earnings from Nvidia.

The FOMC minutes revealed little new information. Inflation remains stickier than expected, keeping the Fed on pause from cutting rates. However, recent speeches by Fed members did not indicate any real consideration of hiking rates. The market was fairly calm following that release as all eyes focused on Nvidia earnings.

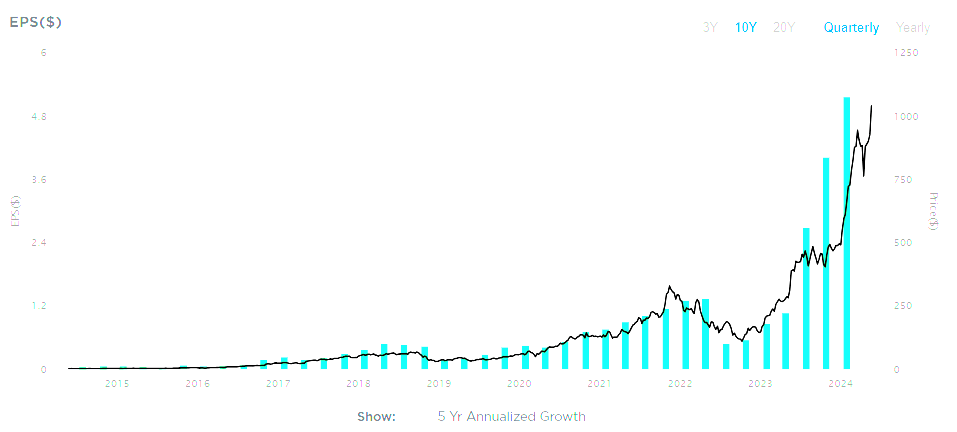

As has been the case over the last few quarters, Nvidia failed to disappoint. It announced earnings and revenue that beat expectations, announcing a 10-1 stock split in the process.

“Nvidia reported revenue for the first quarter ended April 28, 2024, of $26.0 billion, up 18% from the previous quarter and up 262% from a year ago. For the quarter, GAAP earnings per diluted share was $5.98, up 21% from the previous quarter and up 629% from a year ago. Non-GAAP earnings per diluted share was $6.12, up 19% from the previous quarter and up 461% from a year ago.”

(Click on image to enlarge)

Such lifted the stock by 10% on Thursday, but the rest of the market sold off as traders took profits from the FOMC announcement.

From a technical perspective, the markets remain on a current MACD “buy signal” and have cleared all previous resistance levels. Furthermore, the 20-DMA crossed above the 50-DMA, providing additional support to any short-term market correction. The 20-DMA will now become running support for the market. While corrections should be expected, any pullback should be contained by the 20-DMA, which will provide an entry point to add exposure as needed.

(Click on image to enlarge)

When the MACD signal crosses, such will provide the next signal to reduce risk and rebalance exposure as needed. For now, the bulls maintain control of the market narrative. Trade accordingly.

The Week Ahead

The holiday-shortened week should be quiet. The only notable economic release will be the PCE data on Friday. Core PCE, the Fed’s preferred gauge for inflation, is expected to increase by 0.2% monthly and 2.7% annually. Both are 0.1% below last month’s figures. Given the recent slowdown in retail sales and our recent sales analysis of retail and food distributors, it will be interesting to see if the PCE personal spending numbers confirm a weakness in consumption.

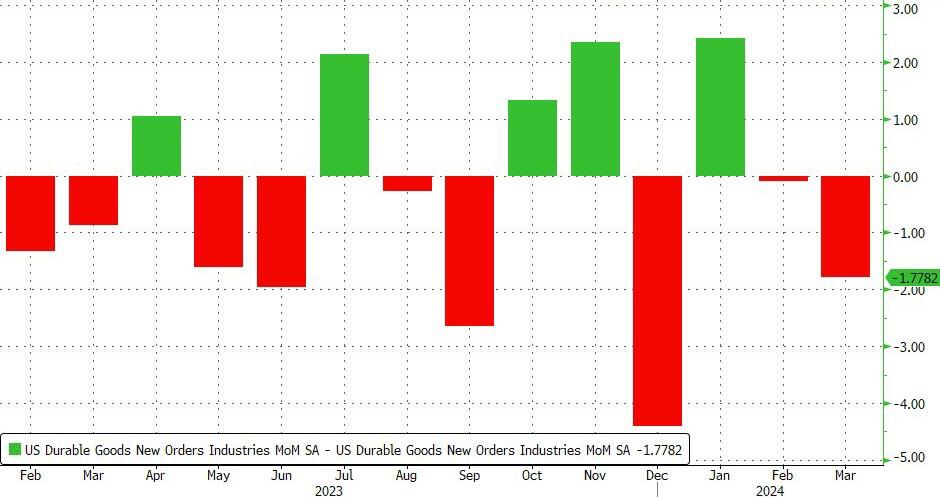

Mind The Revisions

At first glance, the March durable goods data was much better than expected, coming at +0.7% versus expectations of -0.8%. While the beat of 1.5% is very impressive, March was revised significantly lower from +2.6% to +0.8%. The graph below, courtesy of Zero Hedge, shows this is not a one-off instance. Per Zero Hedge:

Over the last 14 months, durable goods orders have been revised lower 9 times (and the downward revisions are considerably larger than the upward revisions).

(Click on image to enlarge)

It’s not just durable goods that have recently seen revisions lower. The four graphs below show significant downward revisions to the BLS payroll data, manufacturing new orders, industrial production, and new home orders. While not shown, PPI has been revised lower in four of the last seven months by a net -0.8%.

Most economic data is revised, as surveys and limited data make it challenging to furnish the market with both accurate and timely results. While this is widely accepted, we find the preponderance of negative revisions versus positive ones unusual. Some will blame the revisions on politics, and others will say these are clear signals that recession is near. Regardless of whether either or both are correct, it is essential to consider the current data points and the trend of the last three and six months, which capture revisions.

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

(Click on image to enlarge)

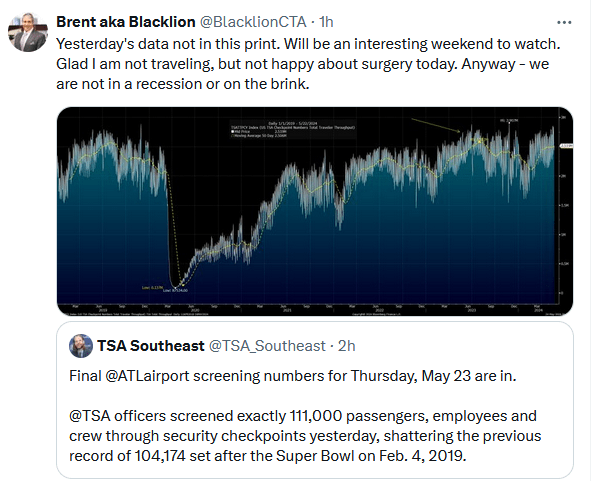

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

More By This Author:

The Risk Of Recession Isn’t ZeroTarget's Sales Woes Are The Norm In The Retail Sector

Market Divergence Prompts An Important Question

Comments

Log in or sign up to join the conversation.