Image Source: Pixabay

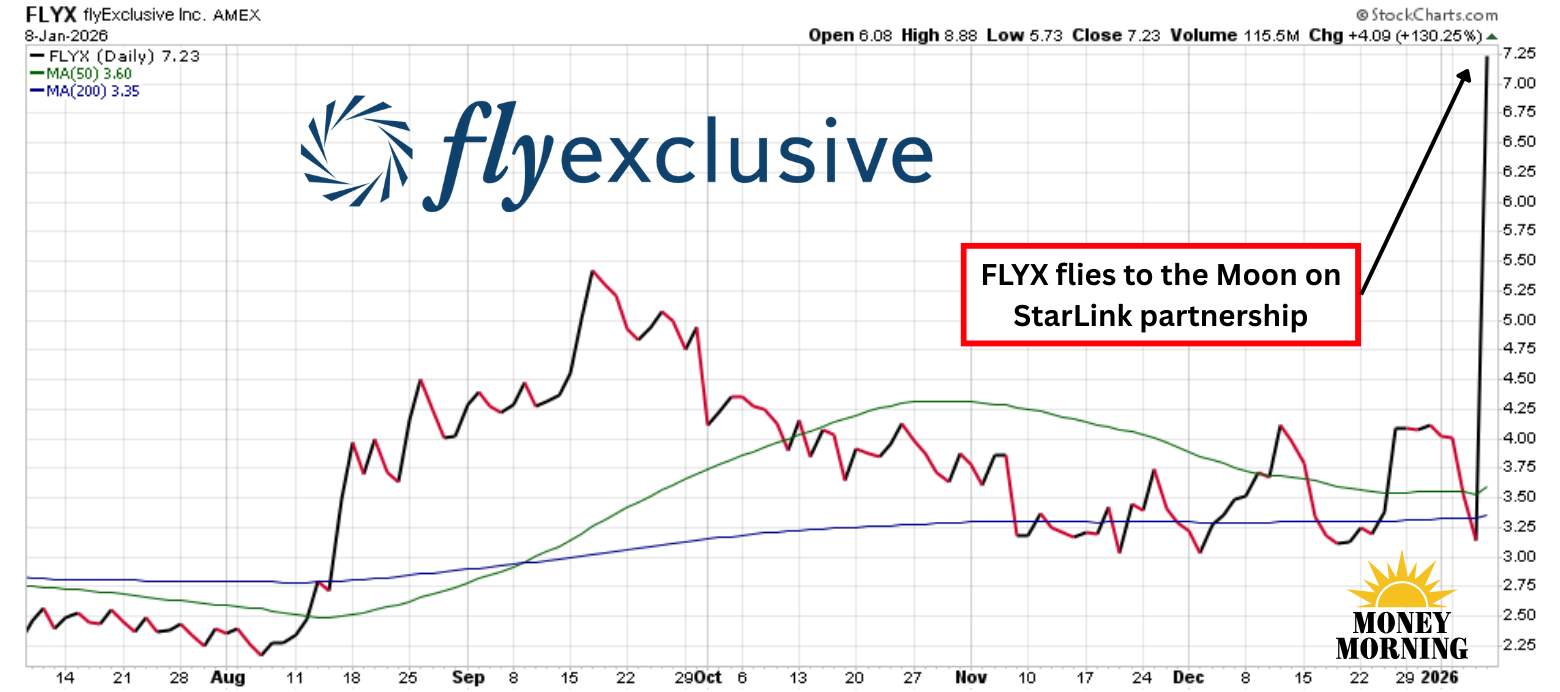

flyExclusive (FLYX) surged 130% after signing on as an authorized dealer of Starlink, SpaceX's satellite internet service. The partnership positions flyExclusive as a certified dealer and installer for Starlink's high-speed, low-latency aviation connectivity system, with installations starting on its Challenger 350 fleet early this year and it will off third-party operators services through its maintenance, repair, and overhaul (MRO) division.

Before the news, flyExclusive was a small, microcap stock trading around $3.00 per share that had largely gone nowhere but down since its December 2023 SPAC merger debut. Even after its massive gain yesterday, FLYX still sits 25% below the $9.70 price it began trading at.

Does the StarLink deal now make flyExclusive a stock to buy or is it bound to crash land?

Who Is flyExclusive Anyway?

flyExclusive is a private jet services provider through on-demand charters, Jet Club memberships, and fractional ownership. It operates a large fleet focused on Citation aircraft while maintaining vertical integration for cost control. It also offers MRO services at its Kinston, North Carolina base.

The new deal gives flyExclusive to StarLink's broadband internet service that is delivered through its massive low-Earth-orbit constellation of 8,000 satellites. StarLink is witnessing rapid growth, with subscriber rolls reaching 9 million in December, double the number it had the year before. Such expansion is also driving revenue higher, with estimates suggesting as much as $10 billion for 2025.

As an authorized dealer, flyExclusive will be able to tap into that revenue stream to install and support Starlink on its aircraft and sell services to external clients, creating a potential new revenue channel for its MRO division.

(Click on image to enlarge)

While third-party installations could generate meaningful income – similar integrations in aviation often involve substantial hardware costs and ongoing fees – flyExclusive didn't provide any specific revenue guidance. Still, the deal complements flyExclusive's fleet modernization efforts but may not immediately unlock a meaningful financial benefit as the private aviation market remains highly competitive.

Starting to Gain Traction

flyExclusive has seen sharp growth on its own, however, with third-quarter revenue jumping 20% to $92.1 million from the year-ago period, helping gross margins surge 45%. Adjusted EBITDA soared 1,480 basis points higher in the period as well, though its was still reporting losses of $1.9 million.

Even so, FLYX shares have only drifted lower after the report, like due to its microcap status and persistent net losses. In a competitive sector like the one it operates in, it needs something to make it stand out as a potential winner.

Bottom Line

I'm not certain flyExclusive's partnership with StarLink is that defining moment. While the deal certainly adds value through enhanced offerings and potential ancillary income, the sharp rally appears driven simply by investor enthusiasm. If you're interested in taking a flyer on flyExclusive, maybe a small bite for the speculative portion of your portfolio, but I wouldn't be a buyer yet. Such meteoric jumps are often followed by a swift decline caused by profit-taking and the market having more time to digest the news.

If flyExclusive truly has wings, there is no need to chase momentum. There will be plenty of opportunities to buy in later.

More By This Author:

Meta Fuels Vistra Surge With Nuclear Pact. Here's Why You Should Buy

Is The Dam Breaking? How Morgan Stanley's Crypto ETFs Could Reshape Finance

Why Bloom Energy Is The Surprising Winner From AI's Insatiable Power Appetite

Comments

Log in or sign up to join the conversation.