Don't Get Too Comfortable: The Crash May Be Coming

There is extensive froth in the stock market right now, and you don't have to go far or dig deep to see what I mean.

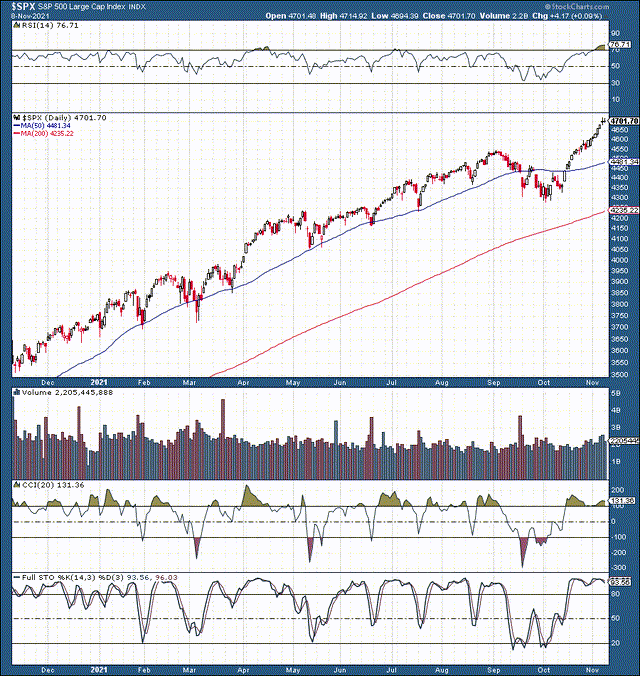

The S&P 500/SPX (SPX)

Source: StockCharts.com

The S&P 500 has now gained about 10% since I began calling to an end to the recent pullback at the lows several weeks ago. We've seen remarkable gains in a short time frame, as the SPX has appreciated in 18 out of its last 20 trading sessions. Moreover, the major stock average is up by about 35% over the previous year.

Technically, the image is significantly overheated right now. The relative strength index ("RSI") is nearing 80, the highest level in over a year. The last time the RSI surged to 80 was right before the 10% correction last September. Moreover, the full stochastic is elevated and looks ready to turn downward, implying a possible shift in sentiment.

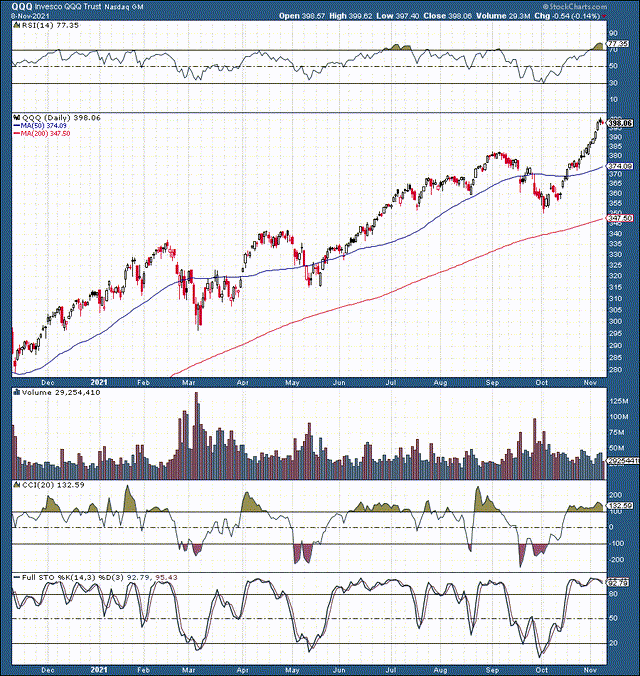

Invesco Nasdaq 100 ETF (QQQ)

Source: StockCharts.com

The Nasdaq 100 is even worse. QQQ looks like it topped out at $400, about a 15% gain from recent lows just several weeks ago. The RSI reached the absurdly high 80 levels and is hovering around 77, signaling highly overbought technical conditions. Incredibly, were looking at about a 43% gain over the last year here. Several other technical elements jump out. QQQ's price is now about 7% above its 50-day moving average. Again, the last time we saw anything close to this disconnect was the short-term top going into September 2020. Now we see the full stochastic turning downward, and the black candle at the recent top could mean that high-flying tech stocks are ready to head lower for now.

Tech Stocks Gone Wild

There is no shortage of froth in the tech sector today. I don't mean just technically, as fundamentally, some valuations seem absurd right now.

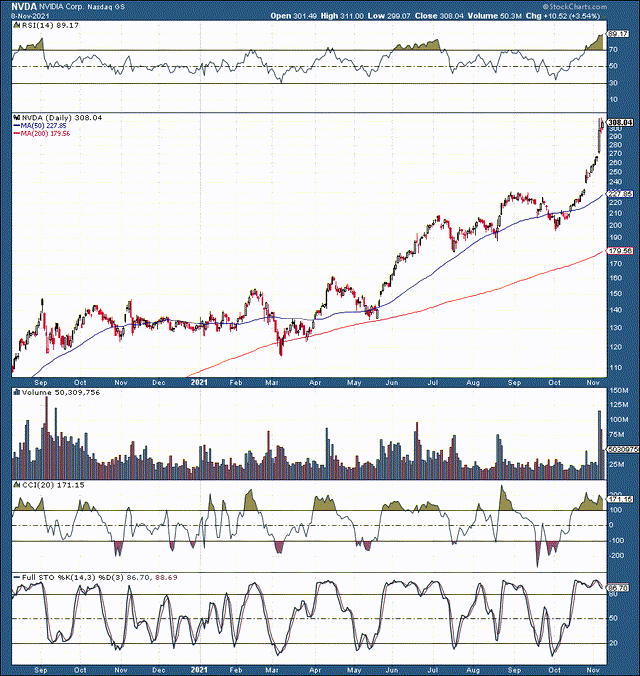

NVIDIA (NVDA)

Source: StockCharts.com

Nvidia is a great company, and the stock has performed exceptionally well lately. Possibly too well, as shares have nearly tripled in just about one year, and the company is approaching a forward P/E valuation of 80 now. Also, if you thought an RSI of 80 was high, check out Nvidia pushing up to around 90 right now. In some cases, an 80 P/E ratio could make sense, but Nvidia is not likely to show exceptional earnings growth in future years. On the contrary, projections illustrate the probability of modest EPS growth in upcoming years.

Therefore, Nvidia with a forward P/E ratio of 80 doesn't make sense in my mind. Additionally, the company is now around a $750 billion valuation with just about $25 billion in revenues set to come in this year. Thus, Nvidia is trading at about 30 times sales right now.

Thirty times sales, what? Is Nvidia a rapidly growing small-cap tech or biotechnology firm? No, it is not. Nvidia is the top tech stock gone wild lately. It is now a mega-cap tech name, the number 7 weight wise company in the S&P 500, and it looks hugely overvalued at this point.

I am no Nvidia bear, and I owned shares in prior quarters. Possibly the only reason I don't own Nvidia now is that I have AMD in my portfolio. However, with the stock now 36% above its 50-day MA on essentially no news, things are getting absurd.

Nvidia could drop by 33% from here, and it would still be relatively expensive at $200 with a forward multiple above $50.

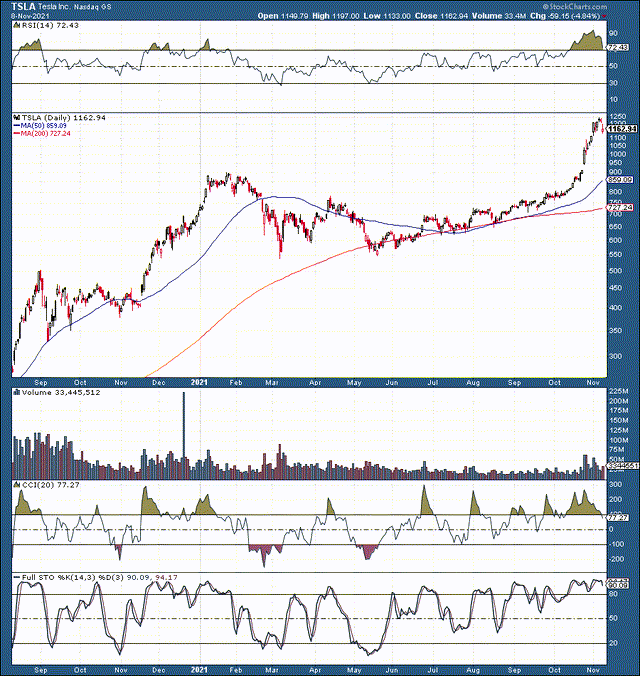

Tesla (TSLA)

Source: StockCharts.com

If you thought Nvidia's valuation was an end to the madness, it's not, likely only the beginning. Let's talk about Tesla for a minute. Now, I am a long-term supporter of Tesla, I've owned the company's shares for a long time, and I've written many positive articles about the company. The first article I ever wrote on Seeking Alpha was "Will Tesla Become A Trillion Dollar Company?" Now, Tesla became a trillion-dollar company much sooner than I anticipated, and I took profits in the stock at around $1,200 recently.

I still like Tesla longer-term, but let's face it, we're dealing with a stock that has expanded by about 4.5X over the last year (this is on top of a remarkable runup the previous year). While it might not be fair to judge Tesla's valuation on its 190 forward P/E multiple, I think the stock is richly priced at 22 times sales.

Technically, the image is mind-boggling, as Tesla recently surged to 50% above its 50-day MA and hit an RSI level well above 90. Tesla is now the fifth-largest S&P 500 component and accounts for about 2.5% of the major average's weight.

Tesla is not the only stock to go wild in the EV space. We see other players like Lucid (LCID) hitting ludicrous valuations. Lucid now trades at a valuation of around $70 billion, while analysts anticipate the company to bring in about $1.7 billion in revenues next year. We're looking at a forward P/S ratio of about 40 here now. Lucid is another stock that has been up by about 4.5X over the last year, and this is another name I took profits in recently.

Tesla could drop to around $800 - 900 support, roughly around a 25-33% pullback from recent highs. The stock would look far more attractive then.

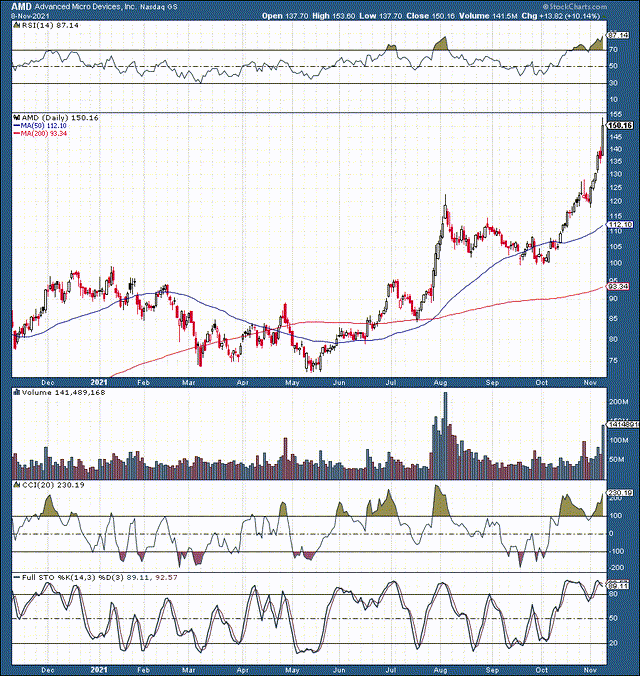

Advanced Micro Devices (AMD)

Source: StockCharts.com

AMD has been one of my favorite stocks recently, and this is one that I'm still long for now. However, the recent runup has been intense. We see an RSI closing in on 90, and this name has nearly doubled over the last year. Yet, at about ten times sales and a forward P/E below 50, it seems relatively cheap to names like Nvidia and others right now. Incredibly, right?

The list of big tech stocks surging lately can go on and on, but I want to look at the most prominent tech stock in the world that is not surging lately. I think it is pretty telling what Apple's stock is doing right now.

AMD could use about a 20% discount around here. A forward P/E ratio closer to 40 would make the stock much more attractive at approximately $120 a share. I am using spreads to hedge my position here. Otherwise, I would take profits now.

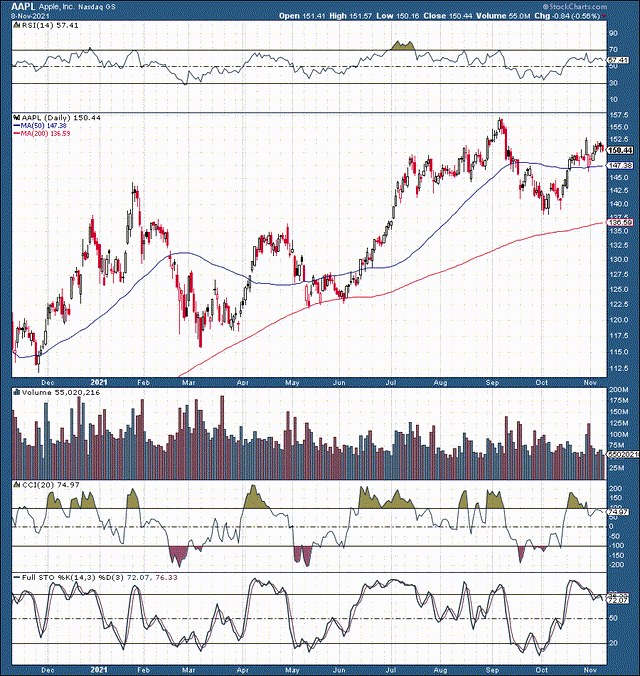

Apple (AAPL)

Source: StockCharts.com - Apple could get its P/E ratio compressed to around 20, implying a price of about $112 for its shares.

So, what is Apple doing lately? Well, not much, as the stock is not skyrocketing to new ATHs as many other technology names are right now. It appears that Apple topped out in early September and has failed to make new highs since. Now, we see a lower high being put in, and Apple looks like it could trade sideways or even head lower for now.

Now, I spoke about Apple being dead money in my previous article on the company, but there is a good reason for this, in my view. While Apple is not trading at 80 or 50 times forward earnings projections, the company is trading at about 27 times forward earnings expectations. The problem is that while AMD, Nvidia, Tesla, and others are still strong growth stories, Apple likely has minimal growth potential in the next few years.

Analysts are typically bullish on Apple but predict low single-digit revenue and EPS growth in future years. So, why is Apple trading at such a premium multiple? After all, 27 times forward earnings are not cheap, and even in the current environment, a company should have robust growth prospects for the next several years.

Apple seems overvalued here, and the company does not deserve such a premium multiple given the probability for stagnant growth in the next several years. Therefore, we could see multiple compression in Apple from now on, and the company's downturn could drag the broader down as well.

The problem is that Apple accounts for a substantial portion of the S&P 500's weight (6%). Another problem is that Apple is not alone, and this may come as a surprise to many people, but Apple is not even the most significant component of the SPX.

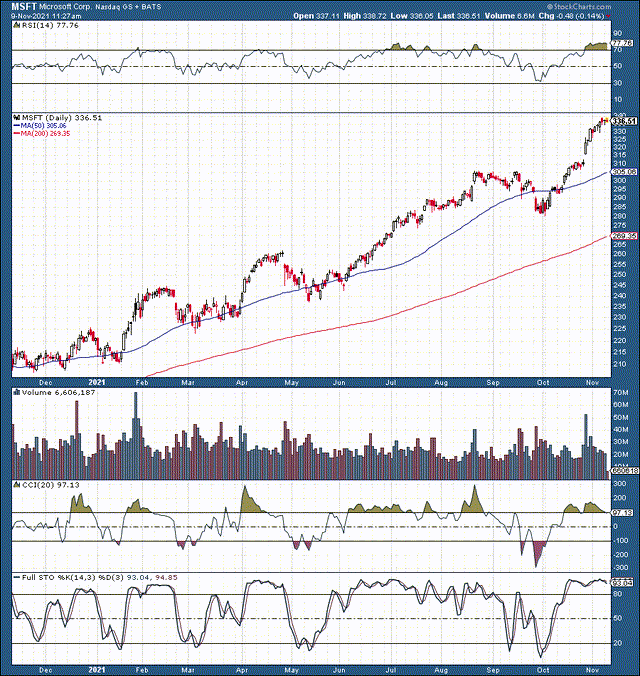

Microsoft (MSFT):

Source: StockCharts.com - Microsoft's stock would look much more attractive with a forward P/E ratio of about 30, suggesting a 20% correction for the stock. Microsoft at $270 looks like a much better buy than it is now.

Talk about being overbought technically. Just look at Microsoft. The RSI here is approaching 80, the stock is up by nearly 60% over the last year, and Microsoft is now the most valuable company globally. Yes, this $2.52 trillion behemoth now accounts for around 6.35% of the SPX's weight. Now, I wish I could say that Microsoft is relatively inexpensive, but that is far from true. On the contrary, Microsoft trades at a whopping 37 times forward earnings expectations.

Granted, Microsoft offers better growth prospects than Apple in future years, but nearly 40 times forward estimates for a stock that could increase earnings by about 10-15% next year is very expensive. We don't typically value huge companies relative to their sales, but Microsoft now trades at a ridiculously high 15 times TTM sales.

I also want to emphasize the growing influence of big tech in the S&P 500 and other major averages. The top seven weighted holdings in the S&P 500 are seven giant tech companies that account for a whopping 27% of the index's weight. It's not difficult to imagine what will happen to the S&P 500 and other major stock indexes when this massive tech bubble unwinds or corrects down the line.

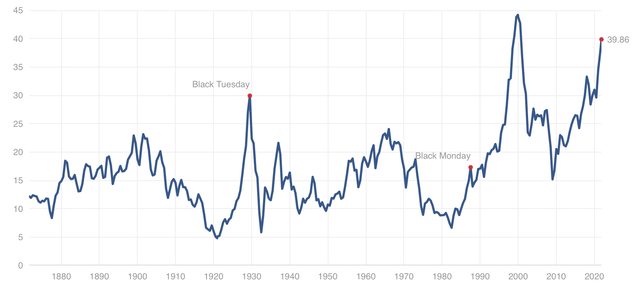

S&P 500 Shiller P/E ratio

Source: multpl.com

I spoke about Microsoft's lofty forward P/E ratio, but it is essentially in line with the Shiller/cyclically adjusted P/E ratio on the entire S&P 500 right now. So, we see that this phenomenon of remarkably high valuations is not only concentrated in tech but is widespread right now. We also see that similar valuations have only been observed once before in history. Yes, around the height of the dot-com bubble, some of us know how that turned out, and the outcome was unfavorable for stocks.

Another factor I want to go over is that while I use a forward P/E in many instances, no one knows what company earnings will be next year. We saw quite a few misses last quarter, far more disappointing results than was expected. Apple and Amazon (AMZN) are just a couple of examples, but many more big names missed guidance.

Therefore, if we look at TTM P/E multiples:

- Microsoft: 42

- Apple: 27

- Nvidia: 90

- Tesla: 228

- AMD: 63

- Lucid: N/A

The Bottom Line

We see many names trading at extremely high valuations right now. Moreover, many prominent companies and major stock market averages are grossly overbought technically. While I focused primarily on the dominant tech companies that account for a massive part of the S&P 500's total weight, the frothy valuations go well beyond technology. The stock market, in general, looks frothy here technically, as well as from a fundamental perspective. Now, we could see a dynamic where the ultra-high multiple names that have skyrocketed lately begin to pull back. Simultaneously, we could see companies like Apple trade sideways or ever move lower due to growth concerns and subsequent multiple contractions. The result could be a "deflation" of the current bubble, which could cause a correction or even a mini-crash to occur as we advance into next year.

Disclosure: I/we have a beneficial long position in the shares of AMD either through stock ownership, options, or other derivatives.

Disclaimer: This article expresses solely my opinions, is ...

more

With pricing and buying being based so much on emotions, these conditions are of course believable and expected. For how long is a guess. Will there be an end? Certainly. Pain and suffering as a result? Of course.