Departmental stores have started reported their earnings for the quarter ended March 2020. While no one was expecting anything meaningful out of the results, given the store closures observed across the country beginning March amid the widespread transmission of coronavirus wreaking havoc globally. However, the results reported from Dillard's (DDS) were direful, to say the least, with Q2 bringing more pain in the offing is prescient.

Q1 2020 Results

The company reported sales of $787mn, down 47% YoY compared to the corresponding period in-line with most estimates expecting a 50% dent. While the payroll expenses declined 35% YoY due to furloughing measures implemented by the company to boost its operating cash flows, payroll expenses as % of sales spiked up almost 4 percentage points from 17.5% to 21.4% in the current quarter highlighting the massive decline in sales proves the measures to be skimpy. The company began aggressively discounting the merchandise products leading the retail gross margins to tumble 2500 bps to just 12.8% and post a much wider than anticipated loss, even beating down the most pessimist analyst estimate by a wide margin with an adjusted loss per share of $6.94 compared to a profit of $2.99 in the previous period.

Is Everything Abominable?

There were several silver linings in the quarterly release from the company. First and most importantly was the update on the store reopenings which led the stock rally up to 12%. DDS has already reopened 149 stores and expects to reopen the remaining stores in the coming week, a benefit for DDS to be a Southern-focused retailer. Also, given most of the stores are fully owned by the company, there are very little rental expenses to put through. It also significantly reduced the inventory decreasing 14% and have also significantly reduced merchandise purchases, down 33% YoY in a bid to conserve cash. It also repaid the $779m borrowed under the previous credit facility and has no borrowings in the current credit facility of $800m. With the only maturity of $45m coming in Jan 2023, the company's default risk is technically nil.

Valuation Alignment

Management cited that the 45 stores opened on May 5 are only producing 56% of their last year's performance due to reduced operating hours. The company is still carrying several incremental promotions on most of the products without which we believe the outlook would be much grim. We expect Q2 2020 to be another washout quarter with 42% sales degrowth and EPS of ($7.46) on aggressive discounting expected to drive sales. We expect the company to post 2020E EPS of ($11.1) boosted by some recovery in the second half of the year.

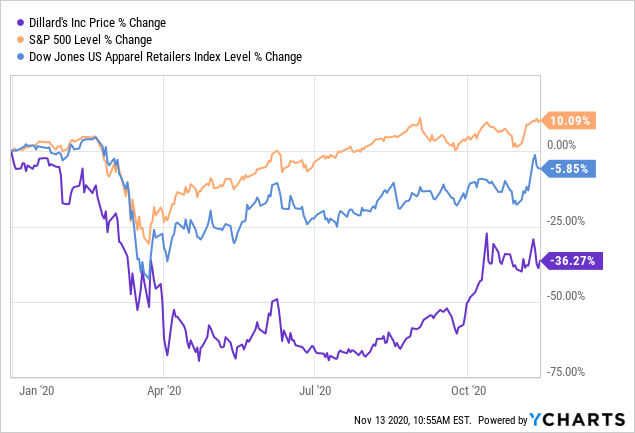

(Click on image to enlarge)

Data by YCharts

We expect 2021 sales to grow by 25% and EBIT margin expansion of 600 bps, however, we do not expect the company to be profitable through 2021E and expect the EPS of ($1.20) per share. DDS has traded at an average 1 Year Fwd multiple of ~5x and we base our valuations at 3x 2021E EBITDA as we expect the company to underperform the department stores industry. Based on the EBITDA of $225m 2021E EBITDA, we value the shares at 3x 21E EBITDA and assign a target price of $17.7. Initiate with SELL.

Comments

Log in or sign up to join the conversation.