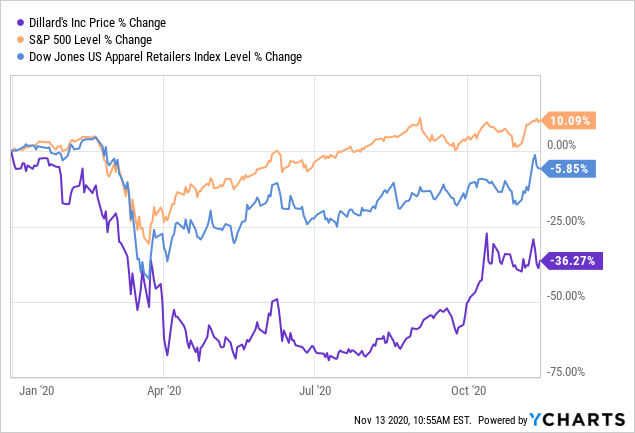

The stocks of department stores have wreaked havoc, tumbling almost 60-70% on average in YTD terms, although, supported by some bargain hunting and renewed optimism of store re-openings lifting the stocks from their all-time lows. The fall, although accelerated by the unprecedented spread of COVID-19 pandemic across the world and especially in the US, coincided with the sector's continued weakness observed due to declining footfalls, lower same-store sales growth and significant competition, particularly from online e-commerce retailers, the likes of Amazon.

Given Trump's push on reopening the economy in a phased manner in the coming weeks, however, it remains to be seen how much of that translates into footfalls for the apparel retailers as shoppers are likely to be wary of the continued rise in the number of cases. At the department stores, covenant breaches are possible if the EBITDA declines by around a third, in which case lenders may have the option to force a default. We take a deeper look at the company's liquidity and solvency as well as possible covenant breaches that could impact the company's refinancing needs.

Data by YCharts

Holiday Season

Most of the departmental stores announced the closing of stores in the week beginning March 16, 2020, which implies the Q1 would primarily have a marginal impact as it is affected by just ~2 weeks, the major impact would be felt in Q2. The sector has been grappling to ensure they have sufficient financial flexibility by furloughing employees, cutting non-essential expenses and utilizing the revolver facilities. Department stores generate roughly 23% of their revenue in Q2, EBITDA contribution in Q2 is around 19%, on average which would likely see a severe erosion due to the store closures. It's interesting to understand Dillard's could be among the least affected as the EBITDA contribution is the lowest in Q2. The Holiday Season of 2020 would be of utmost importance as the retailers generate most of the EBITDA (40%) in Q4 with Macy's being the highest at 50%. Also, upcoming maturity of $500 million coming in for Macy's in Jan-21, if it coincides with poor holiday sales and a choppy high yield market could cause challenges for the company to re-finance.

Revenue Contribution (3 Year Average):

| Q1 | Q2 | Q3 | Q4 | |

| Macy's | 22% | 22% | 21% | 34% |

| JCP | 22% | 24% | 22% | 32% |

| Kohl's | 21% | 22% | 23% | 34% |

| Nordstrom | 22% | 25% | 24% | 29% |

| Dillard's | 23% | 23% | 22% | 31% |

| Average | 22% | 23% | 23% | 32% |

EBITDA Contribution (3 Year Average):

| Q1 | Q2 | Q3 | Q4 | |

| Macy's | 17% | 18% | 15% | 50% |

| JCP | 22% | 22% | 12% | 40% |

| Kohl's | 18% | 28% | 21% | 33% |

| Nordstrom | 19% | 26% | 22% | 34% |

| Dillard's | 44% | 1% | 13% | 42% |

| Average | 24% | 19% | 16% | 40% |

Source: Company filings.

Covenant Review

We detail below the financial covenants and EBITDA declines which when breached could affect the valuation and share price of the stock. For M, EBITDA decline of ~30% could breach the leverage threshold, while a ~20% decline could breach JWN's leverage covenants. Similarly, a 34% decline in DDS EBITDA and 23% in KSS EBITDA could trip its leverage covenants. A breach could trigger an event of default, however, lenders are more likely to reset the threshold and work with the companies in these unprecedented times.

|

|

Leverage Threshold |

Interest Coverage Threshold |

Liquidity ($mn) |

|

|

Cash |

Revolver Drawn |

|||

|

Macy’s |

3.75x (current: 2.6x) |

3.25x (current: 10.0x) |

685 |

1,500 |

|

Kohl’s |

3.75x (current: 2.9x) |

N/A |

723 |

1,000 |

|

Nordstrom |

4.0x (current: 3.25x) |

N/A |

853 |

800 |

|

Dillard’s |

3.5x (current: 2.3x) |

2.5x (current: 5.4x) |

277 |

779 |

|

JC Penney |

N/A |

1.0x (current: 2.0x) |

386 |

1,250 |

Source: 10-K filings.

M was recently downgraded to high-yield from investment grade, DDS and JCP are already rated high yield, while JWN, KSS also faced downgrades and are just one notch above high yield. The recent downgrades for M, JWN and KSS has led to widening of credit spreads which when exacerbated by the closures would lead to EBITDA erosion and potential credit deterioration.

We believe things would perk up by Q4, also for the fact that most of the people deferred their non-essential apparel purchases for the most part of the year would lead to increase in footfalls and store sales, however a prolonged store closure could act as a deterrent. M and JWN face maturity of $551 million and $500 million in Jan 2021 and Oct 2021 respectively in the next 12 months. Kohl's and Dillard's don't have any principal maturities in the next 12 months while the most at-risk company remains JC Penney. This comes to no surprise given it has now became a penny stock and could potentially file for bankruptcy due to its high leverage leaving little value for its equity holders. Also, while Dillard doesn't have any immediate maturities, the recent drawing of its credit facility has led to a breach of its leverage threshold at ~5x which when exacerbated by EBITDA erosion could quickly catapult into a difficult scenario. However, the lower EBITDA contribution in Q2 provides support.

We expect KSS and JWN to weather the storm efficiently. DDS and M could face pressure moving through the world after Covid-19. JCP, we believe, potentially will be filing for bankruptcy.

Comments

Log in or sign up to join the conversation.