Corporate Buybacks; Connecting Dots To The F-Word

Over the course of history in the financial markets, Wall Street has continuously invented increasingly creative ways to peddle its wares under the guise of meeting investors’ “needs”. The modern era of financial alchemy began quietly enough with index investing in the early 1970’s, followed by portfolio insurance in the 1980’s (the cause of Black Monday 1987), progressed to the advent of the exchange-traded fund (ETF) and credit-default swaps (CDS) in the early to mid-1990’s, trailed by internet stocks in the late 1990’s (bubble #1). The 2000’s saw more than its fair share of ingenuity including toxic triple-A rated sub-prime mortgage-backed securities and CDO-Squared structures (bubble #2).

The latest craze in financial engineering plays to the theme of “less is more”. Share buybacks, whereby a publicly-traded company repurchases its own stock in the open market, are driving the stock market to previously unimaginably rich valuations despite weak economic growth and a lack of supporting fundamentals. Share buybacks are being conducted in record amounts without regard for whether a company actually has the cash to spend on such a plan and worse, at prices well-above intrinsic value for those shares.

The growth of stock buybacks

Data Courtesy: Compustat, Aswath Damodaran - 2015 data is estimated

The Federal Reserve (Fed) has been complicit creating this environment through not only their zero interest rate policy but indirectly via the euphoric markets which are partially the result of such policy. The instant gratification that share buybacks offer shareholders, including insiders, in combination with “free” money are so irresistible that companies are more than willing to borrow cash and exchange prudence for the gratuitous short-term pleasure of watching their stock climb on the news. Even if the Fed were to follow through with recently threatened interest rate hikes, markets are clearly not worried that the proverbial monetary stimulus punch bowl will be removed anytime soon. By maintaining crisis policy for nearly seven years and refusing to allow normal market discipline to reassert itself, the Fed has once again laid the groundwork for the third financial market bubble in only the last 15 years.

With the Fed and other government authorities providing cover and Wall Street endorsing the approach, share buybacks are being driven by a desire to both manipulate stock prices in the short term and increase already egregious executive pay. Share buybacks are the mechanism by which value creation is being buried by corporate executives seeking value extraction.

Finance and Accounting 101

A share buyback is exactly what the name suggests. At some point in the past a company issued equity to capitalize the corporation. The repurchase, or buyback, is simply buying some of those shares back either as a tender offer to specific shareholders or in the open market, effectively returning capital and leaving remaining ownership in fewer hands. Most share repurchases today occur in the open market.

From an accounting perspective a company’s true value or net worth before and after a buyback is identical. As the number of shares decrease, earnings per share (EPS) increase proportionately, seemingly making remaining ownership more valuable. However the benefits to remaining shareholders are perfectly offset by the loss of cash used to conduct the buyback. Accounting 101 teaches that assets minus liabilities equals owners’ equity. A cash buyback does nothing more than decrease the assets and the owners’ equity accounts equally, keeping the equation in the same state of equilibrium and leaving the remaining shareholders with the same amount of owners’ equity as prior to the exercise. This accounting identity is among the most basic in corporate finance and accounting.

Because of historically low interest rates, debt-funded buybacks are especially popular today. Unlike cash buybacks which do not produce neither an accounting benefit nor impairment, buybacks supported by the issuance of new debt have an adverse effect on the bottom line. In a debt-funded buyback the asset side of the balance sheet is untouched, however the liability side increases while owners’ equity drops an equal amount. The end result is the company now owes the principal on the money borrowed as well as a series of future interest payments against which future earnings are reduced.

Increased interest expenses with no change to cash flows or earnings negatively affects a company’s credit rating, which in turn increase future borrowing costs and limits future borrowing capacity. Rating agencies have warned that buybacks, especially those fueled with debt, increase the odds of credit downgrades.

From a valuation perspective there is little doubt that buybacks, over the past few years, have led to increases in share prices in the equity market. However, analysts and investors who argue for buybacks on the premise that somehow those actions add real intrinsic value to a company are misguided. These advocates are correct that earnings per shares are increased, but they fail to factor in the negative effects on future earnings when cash is used to buy back stock instead of invested in the company’s future.

When cash or debt is used to perform a buyback, then by definition those dollars cannot be used for other purposes. The question that must be answered is, “What gets sacrificed”?

A company has two options to consider when deploying capital:

- It can reinvest that money by expanding employee skills, increasing pay and benefits, hiring more people, creating new products and services or making other capital investments that make the company more profitable and competitive.

- It can repurchase its own shares and/or pay cash dividends to shareholders – “capital return”.

Deploying capital via share buybacks or dividends diminishes the ability of a company to invest in itself. The recent meteoric growth of returning capital to shareholders simply means far less capital is being deployed by corporations for reinvestment purposes. Prior to the 1980’s, major U.S. corporations employed a “retain and reinvest” approach to resource allocation in order to enhance both operational and human capital. This approach contributed to equitable, stable economic growth in the years to follow. Throughout the 1980s and 1990s however, the focus of corporate leadership shifted. In order to satisfy Wall Street’s demanding requirements for ever-higher quarterly earnings per share, executives lost sight of the long-term objectives and began using stock repurchases and other shortsighted ideas to manipulate EPS and ultimately their stock price.

This behavior ensures the seeds of future earnings growth, re-investment, are being sacrificed for current benefits. While the economic costs of this strategy may not be well publicized, they are palpable. Productivity growth for instance slowed to a paltry .10% in 2014, continuing a slowing trend of the last 30 years. New highs in stock market indices may temporarily mask important economic factors such as the lack of productivity growth, sub-trend economic growth, income disparity and an ever growing debt burden, but the costs of misallocating corporate capital are significant and will be increasingly felt for years to come.

Rationale for buybacks

Corporate executives offer three main reasons for share repurchases:

- Buybacks are investments in our undervalued shares signaling our confidence in the company’s future.

- Buybacks allow the company to offset the dilution of EPS when employee stock options are exercised or stock is granted to employees.

- The company is mature and has limited investment opportunities, therefore we are obligated to return unneeded cash to shareholders.

The logic behind each of these explanations is in the vast majority of cases is flawed, to be kind, and deceptive to be blunt. In a letter to shareholders fifteen years ago, Warren Buffett explicitly addressed the topic of share repurchases through the following direct and critical explanations:

- “Now, repurchases are all the rage, but are all too often made for an unstated and, in our view, ignoble reason: to pump or support the stock price.”

- “Usually, of course, chicanery is employed to drive stock prices up, not down.”

- “The shareholder who chooses to sell today, of course, is benefitted by any buyer, whatever his origins or motives. But the continuing shareholder is penalized by repurchases above intrinsic value.”

- “Buying dollar bills for $1.10 is not good business for those who stick around.”

- “Sometimes too, companies say they are repurchasing shares to offset the shares issued when stock options granted at much lower prices are exercised. This “buy high, sell low” strategy is one many unfortunate investors have employed – but never intentionally! Managements, however, seem to follow this perverse activity very cheerfully.”

Despite The Oracle’s sensible take, many “sophisticated” investors have opted to ignore the deception involved in buybacks and take part in the cheerleading. Rick Rieder, the Chief Investment Officer of BlackRock, the world’s largest asset management firm, recently stated “why risk cap-ex when the bar here is low and the results instantaneous?” The “low bar” and “instantaneous” results referring to the benefits of buybacks.

On the other hand, across the hall in the executive suite, BlackRock’s CEO Laurence Fink had this to say: “More and more corporate leaders have responded with actions that can deliver immediate returns to shareholders, such as buybacks or dividend increases, while underinvesting in innovation, skilled workforces or essential capital expenditures necessary to sustain long-term growth.”

For the record, we concur with Mr. Fink.

S&P 500 buybacks and dividends as a percentage of operating earnings

Data Courtesy: Standard and Poors

Two important facts bear emphasis:

- Stock buybacks do not increase the value of the company from an accounting perspective and when buybacks are done via borrowed money, there is a negative effect.

- Stock buybacks have an often overlooked cost of reducing corporate investment which is not being factored into earnings projections and valuations. By exchanging future earnings growth for hollow short-term stock price gains, CEO’s are having a deleterious effect on productivity and ultimately earnings potential.

There is a reason for everything, for everything there is a reason

So if share repurchases do not in any way enhance the intrinsic value of a company, the logic and rationale offered by executives is faulty and/or deceptive and the action itself is viewed as “chicanery”, then why are so many executives and board of directors authorizing them? What are the real reasons?

The answer, as it so often does, lies in the incentives.

Citing from his book The Practice of Management, Peter Drucker wrote “There is only one valid definition of a business purpose: to create a customer.”

In the mid-1970’s Michael Jensen and William Meckling, Finance Professors at the University of Rochester, proposed in an article published in the Journal of Financial Economics that, contrary to Drucker’s philosophy, the singular goal of a company should be to maximize the return to shareholders. The professors argued that in efforts to re-prioritize the objective of maximizing shareholder value ahead of executives’ self-interest, executive incentives should be altered through stock-based compensation. Unfortunately, this concept ultimately became the conventional wisdom of the last 35 years.

In a 2009 article in the Financial Times, Former GE CEO Jack Welch said “On the face of it, shareholder value is the dumbest idea in the world. Shareholder value is a result, not a strategy… your main constituencies are your employees, your customers and your products. Managers and investors should not set share price increases as their overarching goal.”

In a 2011 Forbes article The Dumbest Idea in the World: Maximizing Shareholder Value, author Steve Denning highlights that between “1960 and 1980, CEO compensation per dollar of net income earned for the 365 biggest publicly traded American companies fell by 33 percent. By contrast, in the decade from 1980 to 1990, CEO compensation per dollar of net earnings produced doubled. From 1990 to 2000 it quadrupled.”

As an important side-bar the Securities Exchange Commission in 1982, allowed companies to buy back their own shares with virtually no regulatory oversight.

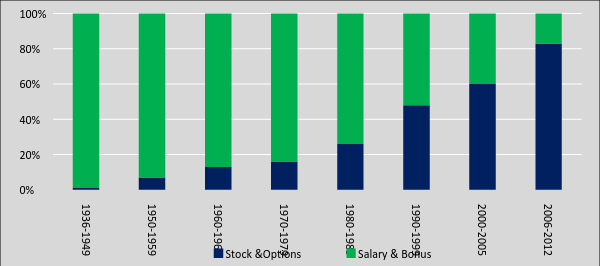

Corporate executive compensation has become much more dependent on current EPS and ultimately stock prices as an incentive metric with stock option grants and outright stock awards increasing dramatically. In 2012, average CEO pay for S&P 500 companies was $30 million of which 83% was comprised of stock options and awards as shown below.

S&P 500 executive compensation structure

Data Courtesy: Roosevelt Institute

As executive compensation has soared, the reasons for buybacks becomes more apparent. First, buybacks allow companies to manipulate their stock price in the short term to please investors and analysts. Second, they are a means of increasing pay for top executives resulting in their personal financial gain at the expense of innovation, employees and job creation.

Fraud ( frôd/ noun) : wrongful or criminal deception intended to result in financial or personal gain.

This should be required reading - thanks for bringing attention to an increasingly problematic issue.

Thanks for the share!

Excellent article, thank you for sharing.