Cash Crunch Intensifies

This morning, stock and commodity markets are plunging amid news of escalating stress at systemically significant investment bank Credit Suisse (CS). The bank’s share price is -24% this morning and -96% since its cycle peak in 2007.

Years of destructive financial incentives, treating cash as trash, and lax risk management, are yielding another financial crisis.

All over the world, people are moving cash out of low-yielding bank accounts and into higher-yielding deposits. At the same time, the economy is producing less free cash flow, and operating cash is being drawn out of bank accounts. To fund the surge in withdrawals, some banks must sell some of their longer-dated securities, like Treasuries and mortgage-backed bonds, that they had previously intended to hold to maturity. The price of these assets dropped sharply in 2022 as central banks launched rapid tightening, so moving them to the available-for-sale category forces capital losses.

Shareholder equity and retained earnings (tier-one capital) are the primary funding source for banks. When share prices tank, tier-one capital follows with a need to raise cash. The trouble is that selling your shares to investors is hard to do when sentiment is intensely hostile, and doing so caves your share price even further.

As bank equity tumbles, it’s important to understand that not only have smaller lenders been funding higher-risk start-ups and small businesses this cycle, but they have also been a significant source of funding for commercial real estate in many countries. This is all connected. See Looming Liquidity Question for NY Commercial Real Estate:

The closure of Signature Bank will remove a significant source of liquidity in the New York commercial real estate market. In a response to a WSJ article earlier this year, Signature Bank noted that they have “been a top three multi-family lender in the New York metro area since 2009; in some years, the Bank was the leading multi-family lender.”

As if this doesn’t seem like enough of a bad omen for mortgage liquidity in one of the highest-cost metros in the country, the response goes on to note that Signature Bank was “one of the largest financiers of low-to-moderate income multifamily housing in New York.” Other lenders may increase their activity to fill the gap left by Signature Bank, but it seems unlikely in the current environment. Higher interest rates, looming mortgage maturities, questions about real estate demand – in particular the office sector – and the emergence of a banking crisis all spell trouble for commercial real estate funding.

The US bank stock index (BKX, comprised of the 24 largest regional and national banks) has fallen 17% year to date and 42% since it topped in January 2022. Since peaking in February 2022 (with Canada’s housing bubble), Canada’s financial index (XFN) was down 18% as of last night’s close and has more downside work.

What happens in banks doesn’t stay in banks. Losses in the sector manifest in less lending and economic activity, as well as broad market losses. Financial shares comprise about 14% of the S&P 500 and 31% of Canada’s TSX market cap.

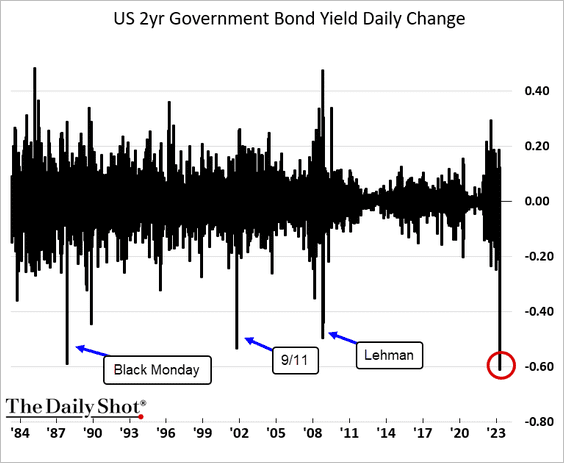

Unsurprisingly, future markets have gone from last week’s pricing rate hikes through the end of 2023 to 100bps of Fed cuts over the next 12 months. Confident predictions are all up for review. Stay tuned.

More By This Author:

Backstops For Depositors, Not Risk Markets

Loonie And Treasury Yields Diving Together

Fed Hangs Tough