Bullish exuberance is returning to the markets and the economy in a big way following the Presidential election. Such is particularly the case with recent executive orders signed by Trump, which fulfill Trump’s promises to “Make America Great Again.” Given that short-term market dynamics are driven primarily by sentiment, as investors, we can not dismiss the rapid turn in optimism over the last few weeks. We addressed this point in this past weekend’s “Bull Bear Report,” which I want to build on in today’s commentary.

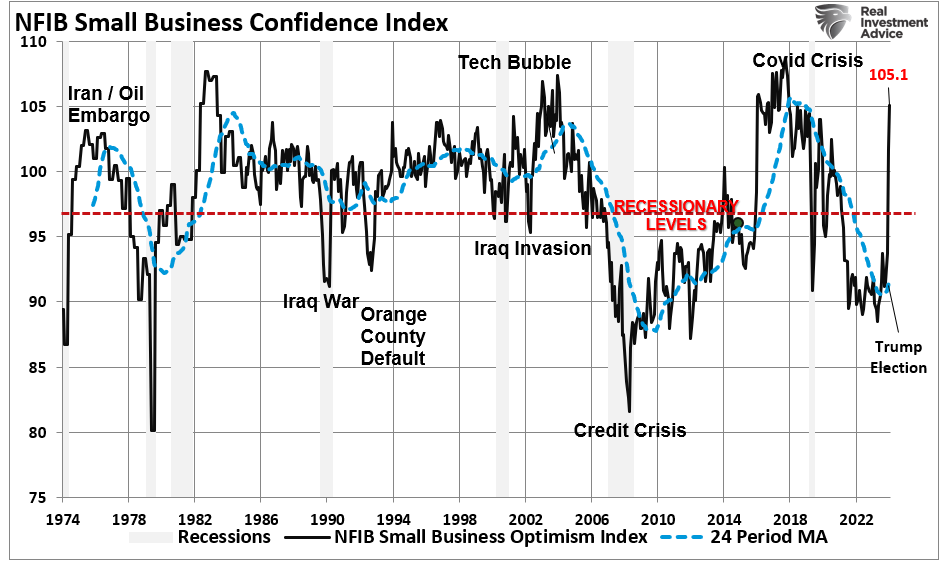

As discussed in that report, the NFIB confidence index has surged from some of the lowest readings on record for the past four years to some of the highest.

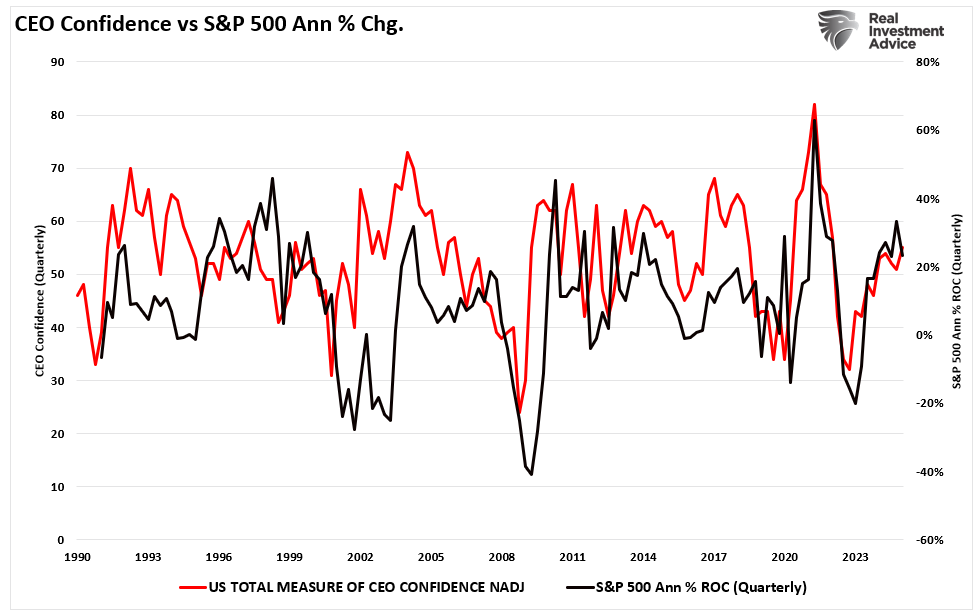

Consequently, as small business owners’ confidence improves, the CEOs of large companies are also becoming much more optimistic. As shown, and unsurprisingly, there is a correlation between the improvement or decline in CEO confidence and the annual rate of change in the financial markets. Higher asset prices, which impact CEO compensation through stock options, have certainly lifted their spirits.

The improvement in optimism is unsurprising given the many anti-business policies and regulations implemented by the former administration. With many of the previous regulatory hurdles either being immediately repealed or promised to be, business owners are “feeling” much more confident about the future of their businesses.

Note that I put “feeling” in quotes.

This is because the NFIB, CEO, consumer confidence, and most business surveys are based on “sentiment.” While sentiment is important to business decision-making, economic outcomes can easily reverse it. In other words, optimism must be supported by improving economic activity. However, the “hope” is certainly high that such will be the case, and increased activity will lead to an extension of the current bull market.

Consumer Confidence: A Critical Driver

In a previous article, we discussed the importance of consumer confidence in the economy and the stock market. This is why, in 2010, the Federal Reserve clearly expressed its reasoning for launching the second round of “Quantitative Easing.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began anticipating the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.” – Ben Bernanke

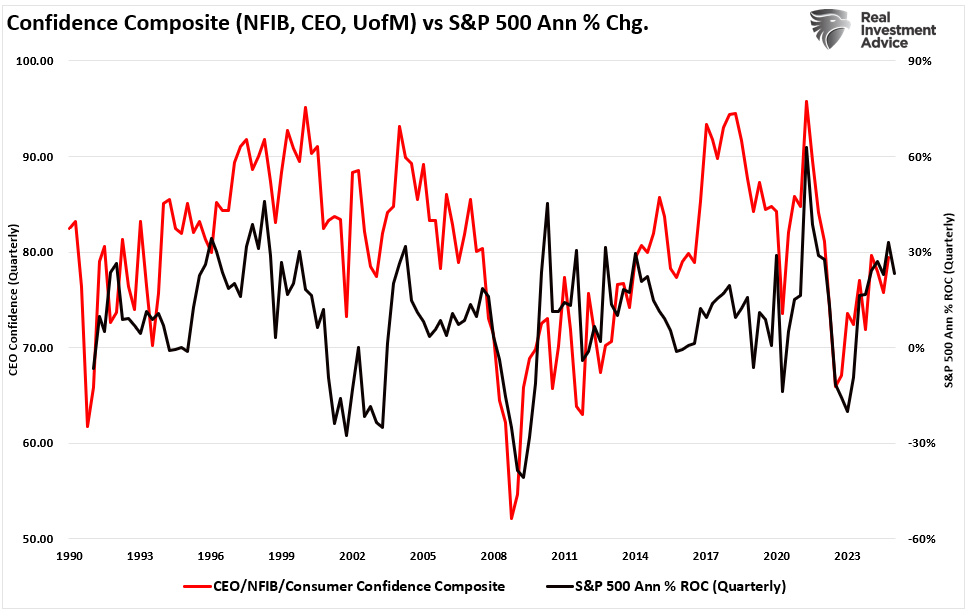

Specifically, Bernanke was referring to two things. First, creating the “wealth effect” by lifting asset prices was crucial to getting consumers “feeling better” about spending money in the economy. As their wealth rose, their economic activities increased business demand, thereby lifting the sentiment of business owners and CEOs. The chart below shows a composite index of Consumer, Small Business, and CEO confidence compared to real GDP growth.

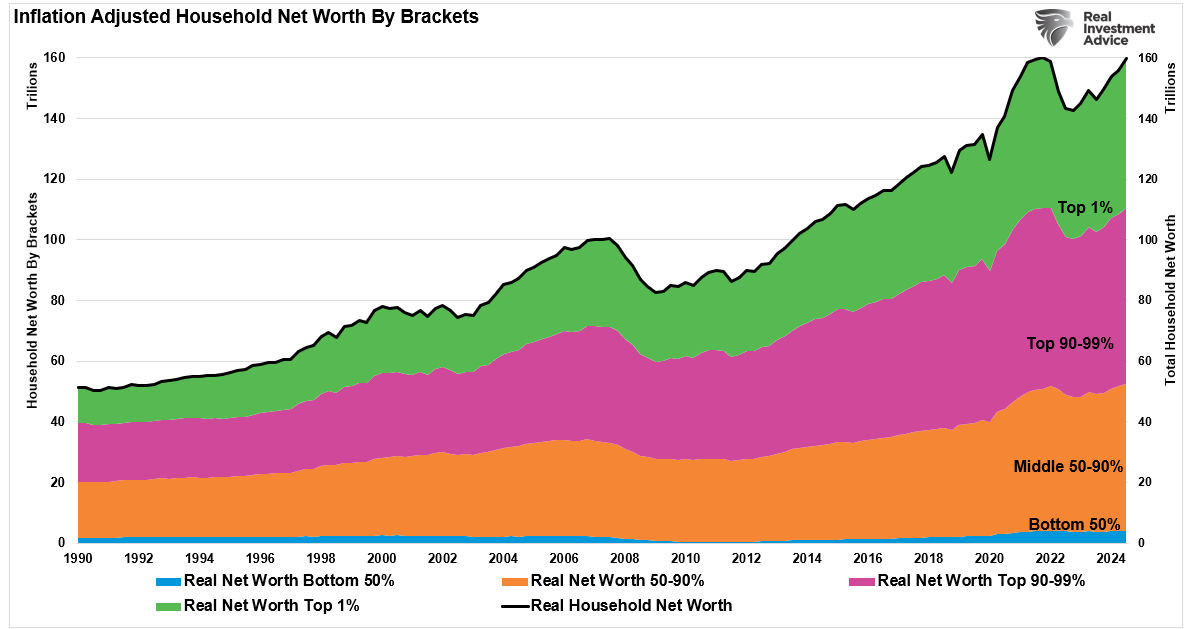

While the high correlation is unsurprising, it is worth noting that not all periods of high confidence led to increasing strong economic activity rates. Such was particularly the case following the financial crisis as sentiment rose sharply, but economic activity was mired around 2% annualized growth rates. That was because the wealth effect creation following the “Financial Crisis” was not broad-based. As shown, the inflation-adjusted household net worth for the bottom 50% of the population failed to change substantially.

Furthermore, while asset price inflation certainly lifted overall confidence, the benefit was concentrated in the top 10% of income earners. That group owns roughly 88% of all household equity ownership. That concentration of wealth kept economic growth rates suppressed as the bottom 50% of economic participants could not substantially increase consumption.

Nonetheless, the current levels of bullish exuberance in the markets are understandable. As shown, there is a high correlation between the confidence composite index and the market’s annual rate of change.

So, while Trump’s recent inauguration and his policy agenda have certainly boosted the market’s “bullish exuberance,” there is a risk.

The Risk Of Bullish Exuberance

The risk to “bullish exuberance” is that it depends on “expectations” being met by reality. Investors and Wall Street analysts are very optimistic about a continued bull market in the years ahead. However, I suggest there are potential headwinds as the economy normalizes following an era of monetary interventions.

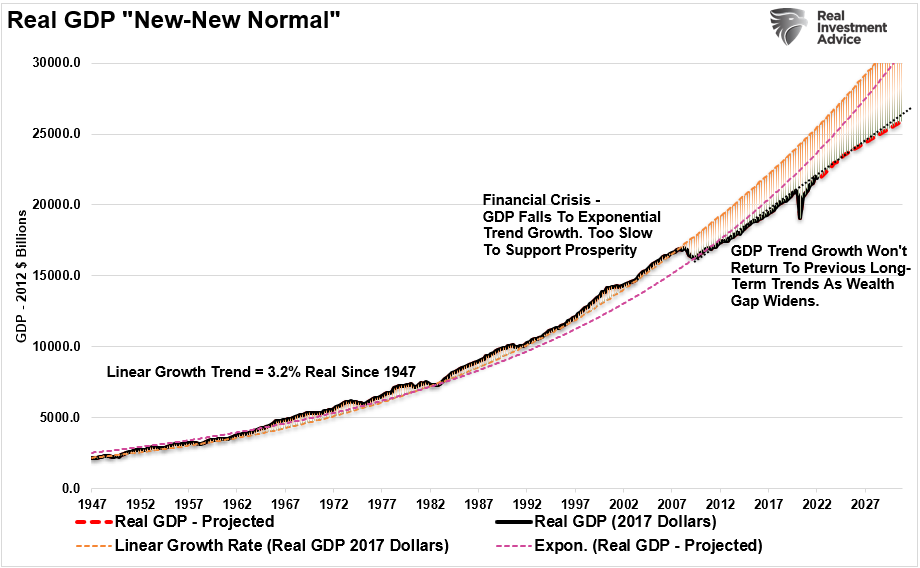

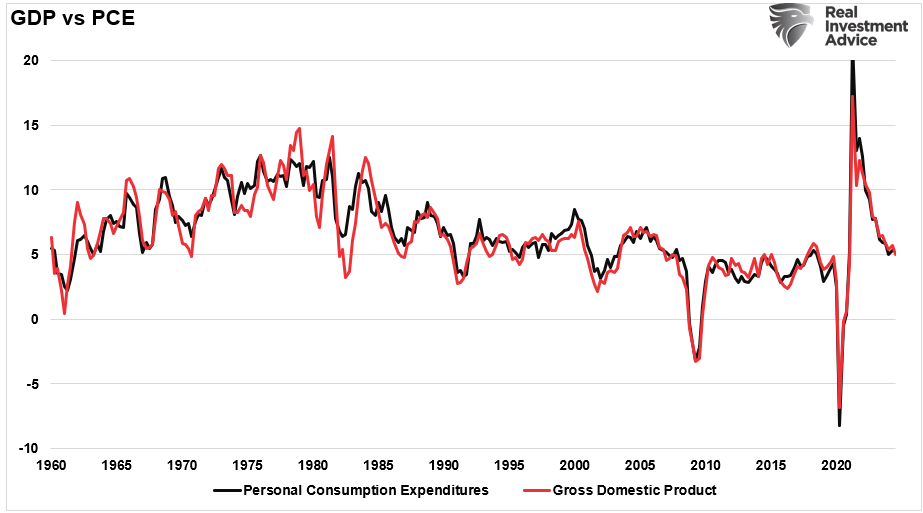

One of those headwinds is earnings growth. Earnings are a function of economic activity. To visualize this data, we must look at the correlation between the annual change in earnings growth and inflation-adjusted GDP. There are periods when earnings deviate from underlying economic activity. However, those periods are due to pre- or post-recession earnings fluctuations. Currently, economic and earnings growth are very close to the long-term correlation.

However, earnings growth will also slow as economic growth normalizes toward its post “Financial Crisis” 2% long-term trajectory.

In an economy roughly 70% dependent on consumption, that consumption generates the revenues to create corporate earnings. As that consumption rate declines toward its 2% trend, so too will the corporate earnings growth rate.

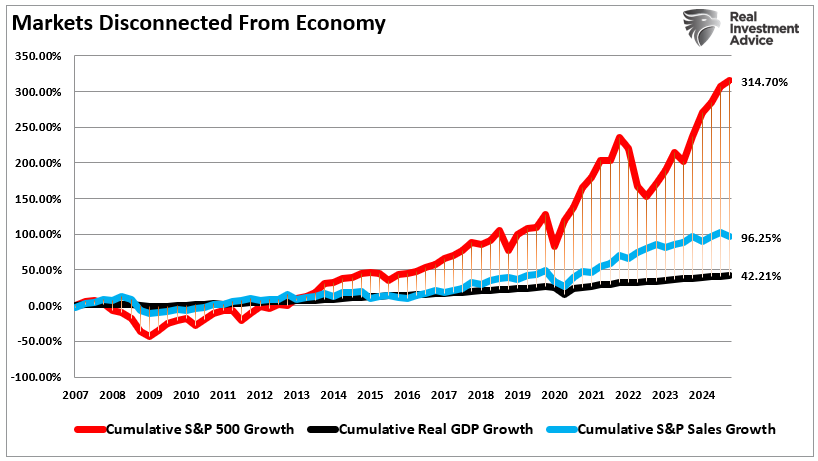

Secondly, since the “Financial Crisis,” the market has vastly outgrown the underlying fundamentals of corporate revenue and economic growth. With the wealth gap widening, it will become more difficult to “pull forward” future consumption. Since the 2007 peak, the stock market has returned over 300%. That increase is more than 7x the growth in real GDP and roughly 3x the growth in corporate revenue.

(I have used SALES growth, which is not as subject to accounting manipulation.)

Conclusion

For investors, the biggest risk to “bullish exuberance” in 2025 is “disappointment.” With the bar set for “perfection,” a slower-growing economy or economic disruption leaves investors open to a large reversal in sentiment. As discussed, optimistic sentiment is important for business owners and CEOs to increase wages, employment, and CapEx. However, those plans will be reversed if consumer demand fails to appear.

Will such a thing happen with certainty? No one knows, but the underlying data certainly suggests the risks are elevated.

As investors, we must analyze the risks to our capital and adjust accordingly. As we concluded in “Curb Your Enthusiasm:”

- Tighten up stop-loss levels to current support levels for each position. (Provides identifiable exit points when the market reverses.)

- Hedge portfolios against significant market declines. (Non-correlated assets, short-market positions, index put options)

- Take profits in positions that have been big winners. (Rebalancing overbought or extended positions to capture gains but continuing to participate in the advance).

- Sell laggards and losers. (If something isn’t working in a market melt-up, it most likely won’t work during a broad decline. It is better to eliminate the risk early.)

- Raise cash and rebalance portfolios to target weightings. (Rebalancing risk regularly keeps hidden risks somewhat mitigated.)

“Investing in 2025 will require a blend of optimism and caution. With slowing economic growth, fiscal policy uncertainties, global challenges, overconfident sentiment, and ambitious earnings expectations, investors have plenty of reasons to approach the markets carefully. There will be a time to raise significant cash levels. A good portfolio management strategy will ensure exposure decreases and cash levels rise when the selling begins.”

That remains our suggestion as “bullish exuberance” increases.

More By This Author:

MSFT And TSLA: Earnings Create Quite The ConundrumRate Cuts Put On Hold

The Chart That Should Worry The Fed

Comments

Log in or sign up to join the conversation.