Lululemon Athletica Inc. (LULU) posted blowout second quarter earnings results in early September and provided upbeat guidance as proves it can successfully navigate higher costs and a slowing economy.

The yoga clothing firm turned sportswear powerhouse’s valuation levels are now in line with Nike, yet LULU’s growth outlook is far more impressive as it expands its reach and its higher income customers keep on spending.

Investors might want to consider Lululemon at the moment given its top and bottom line growth outlook, valuation levels, and its ongoing drive for expansion through diversification.

From the Gym to the Office & Beyond

Lululemon first made waves in the apparel world through its expensive women’s yoga clothing, which is still a part of its business. The company has also evolved into a well-rounded sportswear and apparel company that’s helped transform the way countless people dress.

Lululemon sells an array of clothing for both women and men that are fit for the gym, the office, a date night, the golf course, and practically anywhere. Lululemon makes everyday pants, shirts, and tops. LULU’s outwear and jacket segment is growing, alongside its various accessories, and self-care products. The company still sells tons of leggings, athletic shorts, and workout gear as well.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Lululemon has introduced its own women’s footwear segment. And one of its newest expansion effort is its very own resale shop that allows users to sell and buy used Lululemon apparel. Other major higher-end brands with loyal consumers such as Patagonia have found success with their own resale sites, as the segment gains traction with online shoppers.

Outside of clothing and shoes, Lululemon bought digital-focused at-home fitness company Mirror in 2020. The company in early October launched its new Lululemon Studio to pair with its Mirror tech, which starts at $795. The new Studio membership costs $39 per month and requires the Studio Mirror. It allows users to access tons of workout content, along with 10% off Lululemon purchases, and other perks.

(Click on image to enlarge)

Image Source: Zacks Investment Research

Growth and Outlook

Lululemon grew its 2021 sales by 42% to $6.3 billion to help its adjusted earnings by 66%. This growth wasn’t artificially boosted by easy comparisons, since LULU posted 11% revenue growth in the pandemic-hit 2020 and it averaged 17% sales growth between FY20 and FY16.

LULU reported strong Q2 results on September 1, with revenue up 29% YoY and comparable sales 23% higher. The company’s key direct-to-consumer revenue jumped by 30% and 32% on a constant dollar basis. It is worth noting that a large chunk of its sales still come from North America and the U.S. This is helpful as the strong U.S. dollar hurts many firms that do tons of business outside of the U.S.

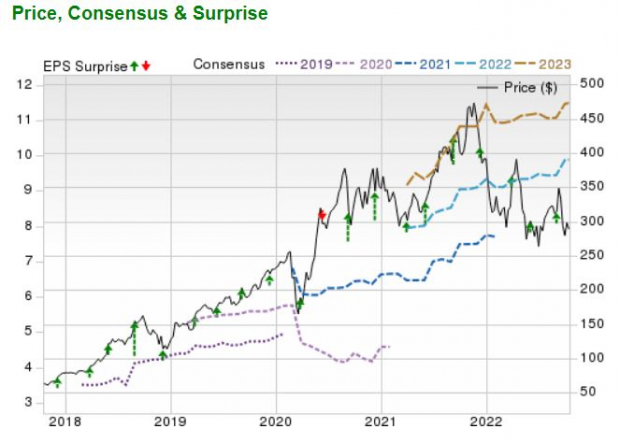

Lululemon’s gross profit jumped 25% to $1.1 billion, with adjusted earnings 33% higher to help it blow away our Zacks consensus by 18%. The company also provided upbeat guidance for the current quarter as well as for fiscal 2023 to prolong its upward earnings revision momentum. The bottom-line positivity also helps it land a Zacks Rank #1 (Strong Buy) at the moment.

Zacks estimates call for its revenue to surge by 27% in 2022 to hit $7.93 billion and then climb to another 15% to $9.1 billion in FY23. Lululemon’s adjusted earnings are projected to climb 27% in FY22 and another 16% in 2023 to come in at $11.49 per share.

Wall Street also loves that the firm is committed to expansion. For instance, its so-called Power of Three x2 initiative aims to double its sales from 2021’s $6.26 billion to $12.5 billion by 2026. To help achieve this goal LULU executives are aiming to “double men's, double direct to consumer, and quadruple international net revenue relative to 2021.”

(Click on image to enlarge)

Image Source: Zacks Investment Research

Other Fundamentals

Lululemon’s higher price tags such as $90 shorts and $120 leggings help it post strong margins. Plus, it operates a mainly direct-to-consumer business via its own stores—finished Q2 with 600 locations—and its digital segments to help boost margins further.

The company’s high-end prices bring with it higher-income shoppers. This means that its customers aren’t feeling the impact of 40-year high inflation as much as many others.

Lululemon is a well-run company that continues to grow its top and bottom lines even as it's forced to navigate plenty of the same obstacles as the wider retail industry. LULU also has a nice balance sheet with nearly $600 million in cash and equivalents and $4.9 billion in total assets vs. $2.06 billion in total liabilities. And it repurchased about $125 million worth of its own stock last quarter even as it funds growth efforts.

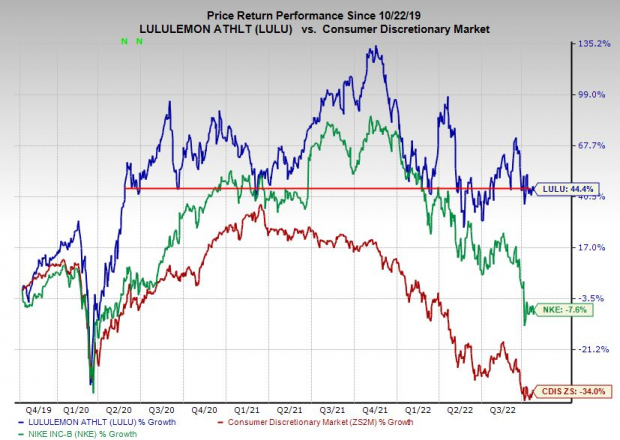

In terms of performance, Lululemon stock has soared 360% in the last five years to crush Nike’s (NKE Quick QuoteNKE - Free Report) 64%, its industry, and the S&P 500. LULU is, however, down 10% in the past two years vs. the S&P 500’s 6% climb. At around $295 per share, Lululemon trades roughly 40% below its November 2021 records.

The apparel firm’s valuation has been recalibrated along with the entire market. And its current P/E ratio is looking rather enticing, with Lululemon trading at a 27% discount to its five-year median and 65% below its highs at 26.6X forward earnings. LULU shares are trading nearly in line with Nike’s 25.1X despite LULU’s far more impressive growth outlook.

Image Source: Zacks Investment Research

Bottom Line

Wall Street is high on Lululemon, with 67% of the 21 brokerage recommendations Zacks at “Strong Buys,” with only one “Sell.” Some might be nervous about considering an apparel company stock with the possibility of a significant economic slowdown on the horizon. But Lululemon is bucking many of the current trends by posting big growth and providing upbeat guidance, as it keeps setting the trends in the fashion world.

More By This Author:

Bear Of The Day: Nike, Inc.Bull of the Day: DexCom, Inc. (DXCM)

Bear of the Day: Papa John's International

Comments

Log in or sign up to join the conversation.