Dillard’s (DDS) , a Zacks Rank #1 (Strong Buy), is a long-term market winner within the Zacks Retail – Wholesale sector. The stock has held up extraordinarily well this year while the general market continues to hover in bear territory. Stocks that are able to show resilience during bear markets and weather the volatility tend to lead the upside once the market turns the corner.

DDS sports the highest-possible ‘A’ rating in our Zacks Value Style Score category, indicating an increased likelihood that the stock continues to propel higher. Dillard’s is trading at just a 7.53 forward P/E. The powerful combination of relative undervaluation and positive earnings estimate revisions should serve bullish DDS investors well into the future.

Dillard’s is a component of the Zacks Retail – Regional Department Stores industry, which currently ranks in the top 37% out of approximately 250 industry groups. Because it is ranked in the top half of all Zacks Ranked Industries, we expect this group to outperform the market over the next 3 to 6 months. Quantitative research studies suggest that approximately half of a stock’s future price appreciation is due to its industry grouping. By targeting stocks contained within leading industry groups, we can dramatically improve our odds of success.

Company Description

Dillard’s operates retail department stores where it offers merchandise, cosmetics, home furnishings, and other consumer goods. DDS is also one of the nation’s largest fashion retailers. The company operates approximately 280 stores as well as an online presence. Dillard’s was founded in 1938 and is headquartered in Little Rock, AR.

DDS is much more than just a department store chain. The company owns a real estate investment trust (REIT), which helps it to enhance its liquidity position. In addition, Dillard’s owns a captive insurance company, enabling it to manage risks more efficiently and provide access to reinsurance markets. The retailer is also engaged in the general contracting construction business.

Recent Earnings and Future Estimates

DDS has been on a hot streak in terms of earnings surprises, beating estimates in each of the past four quarters. Back in August, the company reported Q2 EPS of $9.3/share, a +222.92% surprise over the $2.88 consensus estimate. Dillard’s has posted a trailing four-quarter average earnings surprise of +214.96%. When a company is consistently exceeding estimates by this wide of a margin, it typically creates a ‘tailwind’ and boosts price momentum.

Sales for the second quarter of $1.59 billion also topped estimates by 2.23%. DDS has surpassed revenue estimates in each of the last four quarters.

In the past 60 days, analysts have raised their full-year EPS projections by +38.34%. The Zacks Consensus EPS Estimate now stands at $36.23 per share. Revenues are anticipated to climb 4.79% to $6.8 billion.

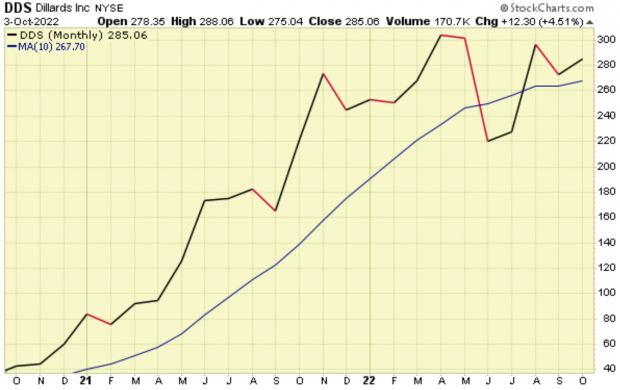

Charting the Course

DDS is up nearly 17% this year alone, widely outperforming the major indices. Only stocks that are in extremely powerful uptrends are able to weather bear markets and corrections so gracefully. This is the kind of stock we want to include in our portfolio – one that is trending well and receiving positive earnings estimate revisions.

Image Source: StockCharts

Notice how the 10-month moving average (as evidenced by the blue line) is sloping up. The stock is forming a bullish cup-with-handle pattern and is showing relative strength versus the market. With both strong fundamentals and technicals, DDS has been one of the biggest winners over the past several years.

Empirical research shows a strong correlation between near-term stock movements and trends in earnings estimate revisions. And as we know, Dillard’s has seen a recent batch of positive revisions. As long as this trend remains intact (and DDS continues to post earnings beats), the stock should continue its bullish run this year.

Other Factors to Consider

Dillard’s remains focused on maintaining a strong balance sheet and liquidity. The company owns 90% of its retail stores and 100% of its corporate headquarters, distribution and fulfillment facilities. DDS has relatively low long-term debt obligations.

Earlier this year, management approved a $500 million share repurchase plan. Additionally, Dillard’s board increased its quarterly dividend to 20 cents/share, equating to a yield of 0.29%.

Bottom Line

As an established veteran in the industry, Dillard’s core business remains strong despite competitive challenges. Buoyed by an undervalued and leading industry group along with a maximum overall Zacks VGM score of ‘A’, it’s not difficult to see why DDS is a compelling investment.

A history of large earnings surprises along with a strong technical trend certainly warrant a closer look at this top-rated stock. Recent positive earnings estimate revisions should also serve to create a ‘floor’ in terms of any sudden or unexpected downside moves. If you’re looking for a way to diversify your portfolio, make sure to put DDS on your shortlist.

More By This Author:

Best Buy Gains But Lags Market: What You Should Know

Don't Panic, And Look To These 2 Big Tech Stocks After The Selloff

3 Top-Ranked Small-Caps Shrugging Off Market Woes

Comments

Log in or sign up to join the conversation.