Image: Shutterstock

Many investors enjoy parking cash in small-cap stocks (under $1 billion market-cap), and for an easy-to-understand reason – their growth potential is very enticing. After all, we all dream of getting in early on the next big thing.

Unfortunately, there is a lot of negative sentiment surrounding the stocks. Why? Small-cap stocks are typically seen as more volatile investments, can carry a higher risk of going bankrupt, and many believe fraudulent activity is widespread. While all these reasons are more than valid, the negative sentiment seems to be a bit overdone.

Plenty of small-caps turn into major long-term winners. Further, they typically have less analyst coverage, allowing investors a window to get in “early” before the crowd catches on. And, of course, as mentioned above, the growth potential is incredible.

Still, small-caps may not suit more conservative investors, as their price swings can sometimes be intimidating. In 2022, there are several top-ranked stocks shrugging off the broader market’s woes, including TravelCenters of America LLC (TA - Free Report), Designer Brands (DBI - Free Report), and Modine Manufacturing Company (MOD - Free Report).

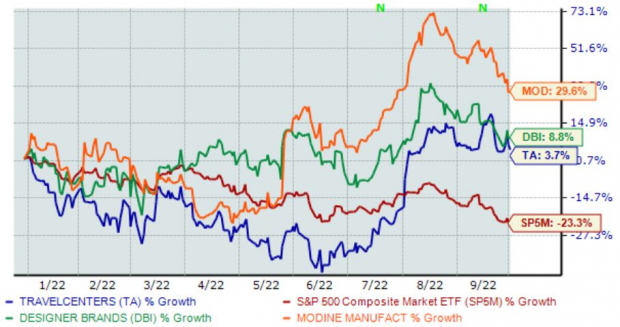

Below is a year-to-date chart illustrating the performance of all three stocks with the S&P 500 blended in as a benchmark.

Image Source: Zacks Investment Research

For those interested in small-caps, let’s dive deeper into each one.

TravelCenters of America

TravelCenters of America is a full-service national travel center chain in the U.S. In addition, TA has nationwide locations serving hundreds of thousands of professional drivers and other highway travelers each month, including virtually all major trucking fleets.

TA’s earnings outlook has turned visibly bright across the board over the last several months, helping push it into a Zacks Rank #1 (Strong Buy).

Image Source: Zacks Investment Research

TA is forecasted to grow at a breakneck pace; the Zacks Consensus EPS Estimate of $8.08 for FY22 pencils in a steep 96% year-over-year uptick in earnings.Revenue projections are also commendable, with estimates calling for 43% year-over-year top-line growth in FY22.

TravelCenters Of America’s earnings track record is undoubtedly a major highlight as well. In its latest quarter, TA reported EPS of $4.34, crushing the Zacks Consensus EPS Estimate by a triple-digit 290%. In fact, the company carries a four-quarter trailing average EPS surprise of a spectacular 1700%.

Designer Brands

Designer Brands is a retailer with a focus on apparel, such as shoes, boots, sandals, sneakers, socks, handbags, and other accessories. DBI sports a favorable Zacks Rank #2 (Buy). Analysts have raised their bottom-line outlook across nearly all timeframes over the last 60 days.

Image Source: Zacks Investment Research

Similar to TA, DBI carries a rock-solid growth profile, with estimates calling for 23% and 10% bottom-line growth in the current and next fiscal year, respectively.

Top-line estimates are also inspiring, with the Zacks Consensus Sales estimate of $3.4 billion for DBI’s current fiscal year (FY23) suggesting year-over-year revenue growth of 7%. And in FY24, revenue looks to expand an additional 3.4%.

In addition, shares are more than reasonably priced, further reinforced by its Style Score of an A for Value. DBI’s 0.3X forward price-to-sales ratio is just a tick below its five-year median of 0.4X, representing a sizable 75% discount relative to its Zacks Retail & Wholesale Sector.

Image Source: Zacks Investment Research

Modine Manufacturing Company

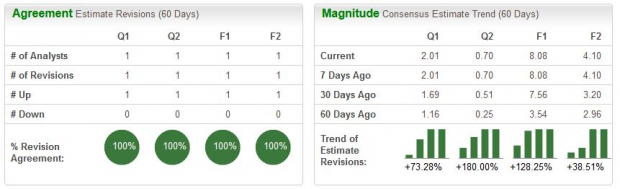

Modine Manufacturing Company operates primarily in a single industry consisting of manufacturing and selling heat transfer equipment, including heat exchangers for cooling all types of engines. Currently, MOD rocks a Zacks Rank #2 (Buy). Analysts have primarily been bullish across nearly all timeframes as of late.

Image Source: Zacks Investment Research

Look out for MOD’s upcoming quarter – the Zacks Consensus EPS Estimate of $0.37 reflects year-over-year earnings growth of a massive 150%. And for the company’s FY23 and FY24, the bottom-line is projected to expand by 40% and 30%, respectively.

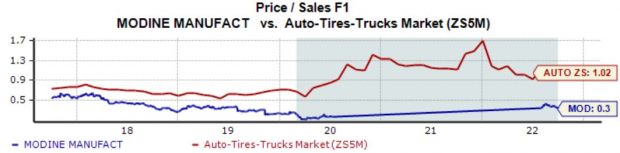

MOD’s top-line is also in good health; revenue is projected to climb 12% in FY23 and a further 2% in FY24. Further, Modine Manufacturing Company shares sit at enticing valuation levels, bolstered by its Style Score of an A for Value. The company’s 0.3X forward P/S ratio sits just at its five-year median, representing a steep 67% discount relative to its Zacks Sector.

Image Source: Zacks Investment Research

Bottom Line

Many could see small-caps as a double-edged sword; the growth potential is substantial but so is the downside risk. However, the negative sentiment these stocks carry feels a bit overdone. There are many examples of small-caps turning into big-time winners. Plus, fewer analysts cover them, causing them to fly under many investors’ radars.

All three small-cap stocks above – TravelCenters of America LLC (TA - Free Report), Designer Brands (DBI - Free Report), and Modine Manufacturing Company (MOD - Free Report) – have crushed the general market in 2022 and carry a favorable Zacks Rank, telling us their near-term earnings outlook is bright.

For those with higher risk tolerance, all three deserve a watchlist spot.

More By This Author:

Bear of the Day: Mohawk IndustriesBull Of The Day: Cracker Barrel Old Country Store

Here's How Levi Strauss Looks Just Ahead Of Q3 Earnings

Comments

Log in or sign up to join the conversation.