Broadcom Inc. (Nasdaq: AVGO) has been a dominant player in the semiconductor and software markets, with strong potential for future growth driven by artificial intelligence (AI) technology.

Recent reports that Google may partner with MediaTek to produce its next-generation AI chips have raised concerns about Broadcom’s market share in the AI sector.

I will use the IDDA (Invest Diva Diamond Analysis) to research Broadcom and determine if it is a buy despite these recent developments.

IDDA Point 1 & 2 – Capital & Intentional

The capital and intentional analysis need to be conducted by you.

- Select your assets in alignment with your financial goals.

- Listen to your intuition about each asset, but remember to invest based on your own values, not just because of recommendations from others.

IDDA Point 3 – Fundamental

Google Considers Ending Broadcom’s Exclusive AI Chip Partnership

Broadcom has been Google’s exclusive supplier for AI chips for the last nine years — but that could change soon.

Reports from The Information suggest that Google is considering partnering with MediaTek to produce the next version of its Tensor Processing Units (TPUs), which are essential for powering Google’s AI infrastructure.

Why Google Might Choose MediaTek

Cost Savings: MediaTek reportedly charges less per chip than Broadcom, which could help Google cut production costs.

TSMC Relationship: MediaTek has a strong partnership with Taiwan Semiconductor Manufacturing Company (TSMC), giving it an edge in chip production.

Diversification: Partnering with MediaTek would give Google more flexibility and reduce reliance on a single supplier.

What This Means for Broadcom

TPUs are critical for Google’s AI strategy, helping to reduce its reliance on Nvidia (Nasdaq: NVDA) and improve AI processing efficiency.

- Google reportedly spent between $6 billion and $9 billion on TPU production last year.

- Broadcom has been projecting billions in future revenue from TPU and custom AI chip sales.

- Losing part of this business would impact Broadcom’s AI revenue stream, but the company’s diversified product lineup could help offset the loss.

Broadcom’s Strong Financial Performance

Despite the potential loss of some TPU business, Broadcom’s recent financial results remain strong:

- Revenue Growth: Up 24% year-over-year (YoY) in Q1 2025.

- Earnings Per Share (EPS): Increased from $1.10 to $1.60

- Free Cash Flow: Generated $5.4 billion in free cash flow in Q1, even after higher debt payments.

Strategic Partnerships and Acquisitions

Broadcom has positioned itself as a leader in AI and software through key deals:

VMWare Acquisition: Strengthens Broadcom’s presence in enterprise software and adds recurring revenue.

Alphabet and Meta Partnerships: Broadcom’s ability to create custom AI chips gives it an edge in the competitive AI market.

CA Technologies and Symantec: These acquisitions expanded Broadcom’s reach into mainframe software and cybersecurity.

- Losing part of the Google TPU business would reduce AI revenue, but Broadcom’s strong cash flow and diversified product mix should limit the impact.

- The company’s dominance in AI chips and high-margin products makes it well-positioned for long-term growth.

IDDA Point 4 – Sentimental

Overall Market Sentiment for AVGO is Bullish

Bullish Outlook

AI Leadership: Broadcom remains a key player in the AI semiconductor market, with projected AI revenue growth of 42% YoY in Q2 2025.

Strong Financial Results: Broadcom continues to outperform market expectations, with consistent revenue and EPS growth.

Wall Street Confidence: Seven analysts reiterated “Buy” ratings after the latest earnings report.

VMWare Integration: 70% of Broadcom’s largest VMWare customers have already adopted the company’s highest-tier bundle, strengthening recurring revenue.

Bearish Outlook

Competitive Pressure: The potential Google-MediaTek deal could reduce Broadcom’s dominance in the AI chip market.

Market Volatility: Broader market concerns about inflation and tariffs could weigh on semiconductor stocks.

Geopolitical Risks: Trade tensions and supply chain issues could limit growth in certain regions.

Broadcom faces competitive pressure from the potential MediaTek partnership, but Wall Street remains largely bullish on the company’s long-term prospects.

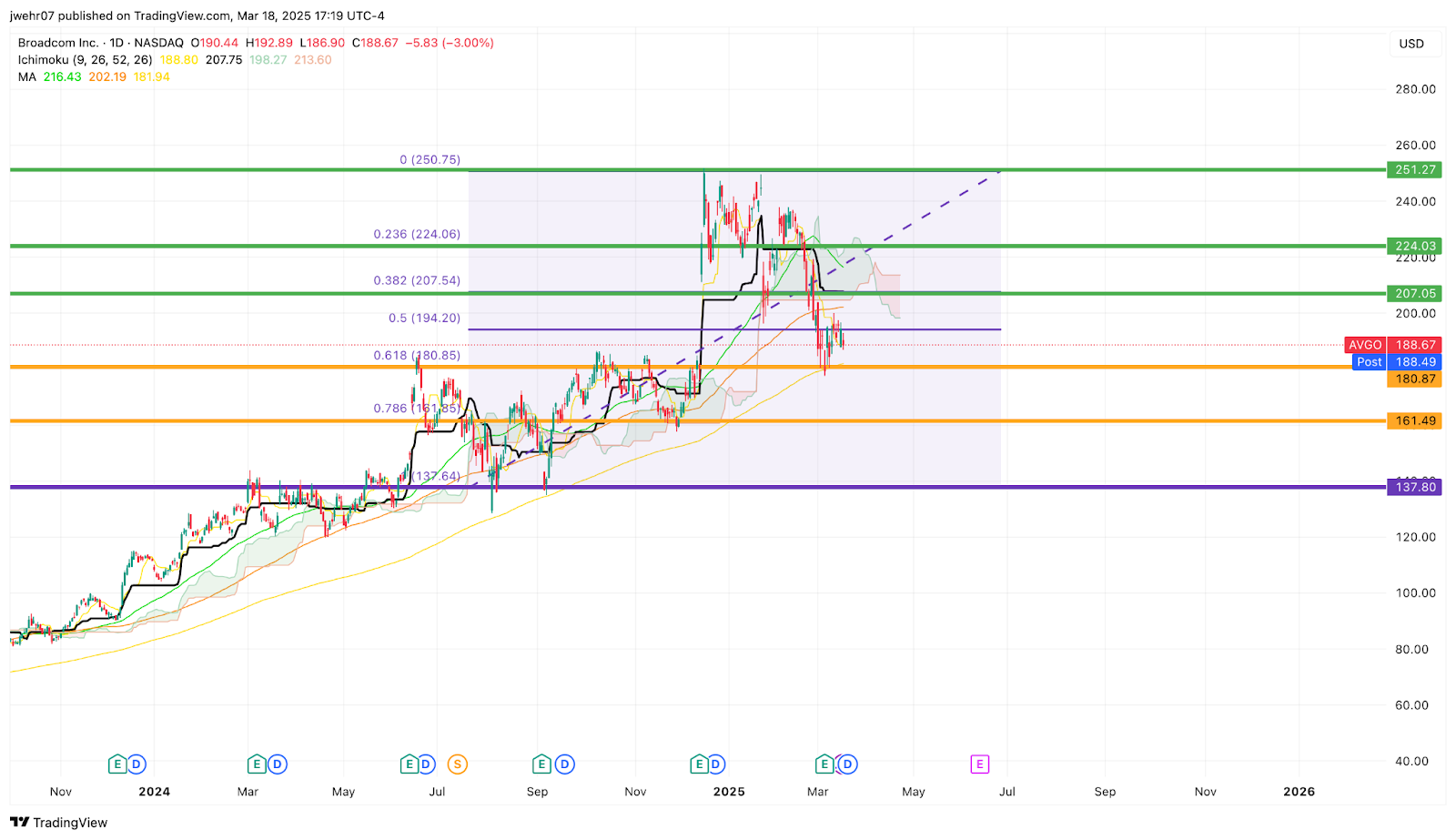

IDDA Point 5 – Technical

Chart Setup

Ichimoku Cloud: On the daily chart, price is trading below the cloud- a bearish signal indicating downward pressure.

Bearish Tenkan-Kijun Crossover: The conversion line crossed below the baseline- indicating short-term weakness and potential downward momentum.

100-Day Moving Average: Broadcom’s stock is trading below the 100-day moving average- a bearish signal that suggests sellers are gaining control in the medium term.

RSI: Currently at 41.15 — indicating neutral momentum, but trending downward.

200-Day Moving Average: Currently at $181.69 — a key support level. If Broadcom drops below this level, it could trigger further selling pressure.

Broadcom’s stock is showing bearish signs in the short term, but strong support at $180 could limit downside momentum.

For those considering adding Broadcom to their portfolio, here are some suggested Buy Limit entry points:

$180.87 – (High Risk)

$161.49 – (Moderate Risk)

$137.80 – (Low Risk)

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

1. If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your CONFIDENCE in the asset you’re planning to invest in).

2. If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

(Click on image to enlarge)

Overall IDDA

Broadcom remains a strong player in the AI market with solid financial performance, high-margin AI chips, and a successful VMWare integration that supports long-term growth.

Its diversified business model and dominant position in AI chips provide a foundation for stability and future expansion.

The potential MediaTek deal introduces competitive pressure and could reduce Broadcom’s share of the Google TPU business, which has been a key revenue driver.

Broadcom also faces broader risks, including market volatility, supply chain disruptions from TSMC, and challenges in maintaining profitability from VMWare integration.

Despite these risks, Broadcom’s strong balance sheet and proven ability to adapt position it well to navigate any near-term challenges.

️ Recommendation:

Buy– Broadcom remains a strong AI and semiconductor play despite short-term headwinds from the Google-MediaTek news. If the stock pulls back further, it could offer an even better entry point for long-term investors.

More By This Author:

Realty Income Stock Update: Steady Dividends In A Stormy Market

Apple’s AI Innovation Crisis: Should Investors Be Concerned?

Intel Stock Update: New CEO’s Crucial 3 Part Strategy To Turn Around Struggling Business

Comments

Log in or sign up to join the conversation.