Breaking Down Upcoming Bank Earnings

Banks are in the news for all the wrong reasons in the wake of what appeared to be idiosyncratic issues at the Silicon Valley Bank. The failure of this California bank and the travails of First Republic Bank (FRC - Free Report) have put a harsh spotlight on the entire regional banking space.

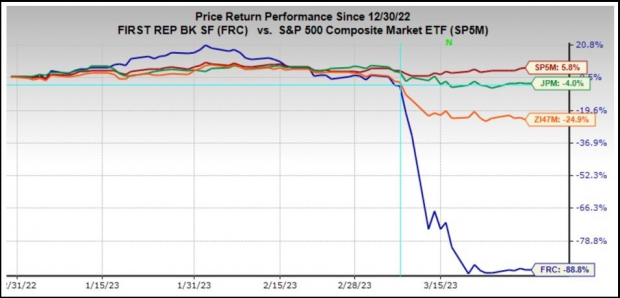

The chart below should give you a sense of the strain in the regional banking space. The chart shows the year-to-date performance of First Republic Bank and the Zacks Banks & Thrifts industry. The chart also shows JPMorgan (JPM - Free Report) as a proxy for the large money-center banking group and the S&P 500 index.

Image Source: Zacks Investment Research

This isn’t a replay of what the industry went through in 2008, but it nevertheless adds to uncertainty about macroeconomic stability at a time when the U.S. Fed’s unprecedented monetary policy tightening has been weighing on the economy’s growth trajectory.

We should also note that the regulatory changes implemented through Dodd-Frank following the 2008 crisis have effectively ringfenced the large banks. These large banks and financial institutions routinely go through ‘stress tests’ by the U.S. Fed that ensures that they are able to operate in a variety of stressful market conditions.

We can say with a high degree of confidence that the exemption that these regional and smaller banks enjoyed from Dodd-Frank’s strenuous regulatory oversight will end after the ongoing crisis is resolved.

We don’t know the specifics of the new regulations that these regionals will be required to face in the future, but they will definitely have more capital requirements. This additional capital cushion will come at the expense of reduced profitability and lower returns from the group going forward.

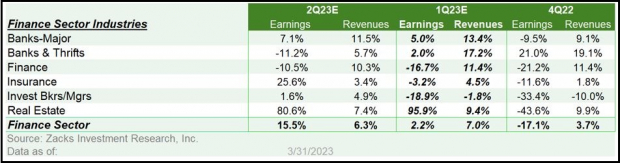

The Zacks Finance sector, which includes all the banks, is expected to achieve +2.2% higher earnings in 2023 Q1 on +7% higher revenues.

The Finance sector is then divided into six mezzanine industry groups, including Banks & Thrifts, where all the regional and local banks are placed. The other banking industry in the Finance sector is the Major Banks industry which includes the money-center players like JPMorgan and some of the very big regionals.

Please note that over the preceding four-quarter period, the Zack Major Banks industry accounted for 44.1% of the Zacks Finance sector’s total earnings, while the Zacks Banks & Thrifts industry accounted for only 3.2% of the total. This should give you a give good sense of the relative earnings power of the two banking-related industries in the Finance sector.

The table below shows the Zacks Finance sector’s 2023 Q1 earnings and revenue growth expectations at the mezzanine industry level.

Image Source: Zacks Investment Research

The going will most likely be tougher for operators in the Banks & Thrifts space in the wake of the Silicon Valley debacle as they will need to compete more vigorously for deposits. This will have negative implications for their net interest incomes.

Operators in the Major Banks space likely benefited from their perceived safety in attracting deposits, but they faced plenty of other headwinds that weighed on profitability. Investment banking receipts were down, as were most other fees, partly offset by gains on the trading side.

Loan portfolios should be up, with gains in credit cards and C&I (commercial and industrial) partly offset by weakness in autos, real estate, and mortgages, helping drive strong net interest income growth.

Credit quality still remains good, though it has started softening from the historically low level of recent quarters. The magnitude of provisions in the Q1 earnings releases will be the big swing factor for year-over-year comparisons for the group.

Estimates for bank earnings have started coming down lately, with the negative revisions trend most pronounced for the regional players. For example, take a look at First Republic (FRC), which is currently expected to bring in $1.13 per share on $1.28 billion in revenues in its March quarter release on April 12th. This represents a -43.5% decline in EPS from the year-earlier level on -8.4% lower revenues. In terms of estimate revisions, First Republic’s current $1.13 per share estimate is down from $1.38 two weeks back and $1.66 at the start of January 2023.

Unlike First Republic, estimates for JPMorgan have largely remained stable. JPMorgan is expected to bring in $3.43 per share in earnings on $36.03 billion in revenues, representing year-over-year growth of +30.4% and +17.3%, respectively. The current Zacks Consensus EPS of $3.43 for 2023 Q1 is a hair below the $3.44 level on March 3rd and $3.41 on January 6th.

The contrasting revisions trend for Frist Republic and JPMorgan notwithstanding, it is reasonable to expect that bank earnings estimates will be under pressure going forward.

The Earnings Big Picture

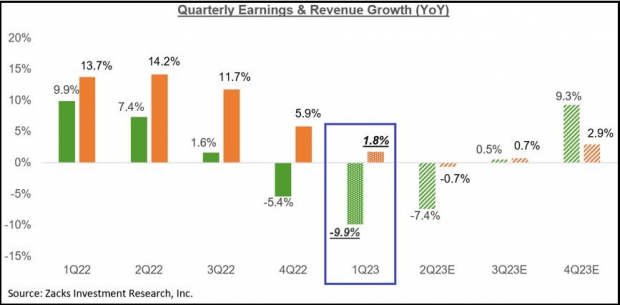

To get a sense of what is currently expected, take a look at the chart below that shows current earnings and revenue growth expectations for the S&P 500 index for 2023 Q1 and the following three quarters.

Image Source: Zacks Investment Research

As you can see here, 2023 Q1 earnings are expected to be down -9.9% on +1.8% higher revenues. This would follow the -5.4% earnings decline in the preceding period (2022 Q4) on +5.9% higher revenues.

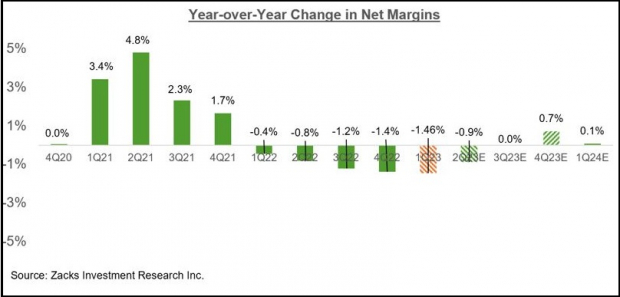

Embedded in these 2023 Q1 earnings and revenue growth projections is the expectation of continued margin pressures, which has been a recurring theme in recent quarters. The chart below shows the year-over-year change in net income margins for the S&P 500 index.

Image Source: Zacks Investment Research

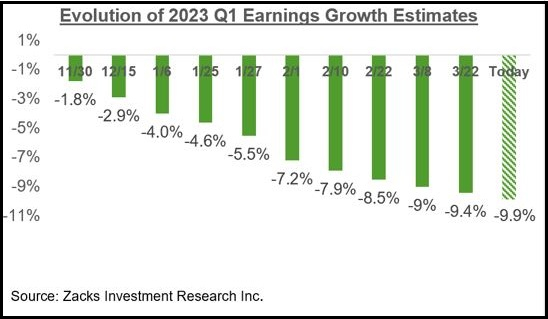

Analysts have been steadily lowering their estimates for Q1, a trend that we saw ahead of the start of the last few of reporting cycles as well.

To give full context, this behavior of negative estimate revisions just ahead of the start of the reporting cycle for that period is on par for the course, historically speaking. We saw this shift during Covid when estimates began increasing for some time. But that trend ‘normalized’ last year and hence the negative revisions to 2023 Q1 estimates, as the chart below shows.

Image Source: Zacks Investment Research

Please note that while 2023 Q1 estimates have come down, the magnitude of negative revisions compares favorably to what we saw in the comparable periods in the preceding couple of quarters. In other words, estimates haven’t fallen as much as they did in the last few quarters.

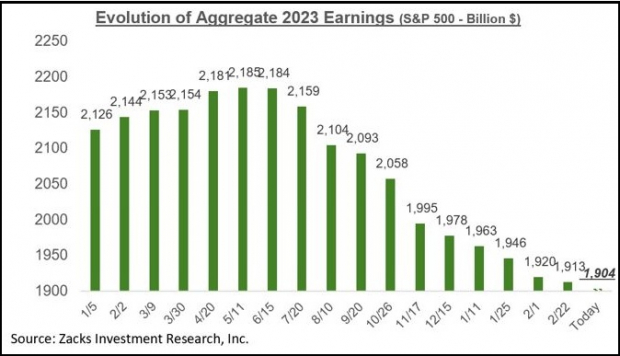

Estimates for full-year 2023 have also been coming down as well, as we have been pointing out consistently in these pages. The chart below shows how the aggregate 2023 S&P 500 earnings.

Image Source: Zacks Investment Research

As we have been pointing out all along, 2023 earnings estimates peaked in April 2022 and have been coming down ever since. Since the mid-April peak, aggregate earnings have declined by -12.6% for the index as a whole and -14.4% for the index on an ex-Energy basis, with the declines far bigger in several major sectors.

You have likely read about the roughly -20% cuts to S&P 500 earnings estimates, on average, in response to recessions.

Many in the market interpret this to mean that estimates still have plenty to fall in the days ahead. But as the aforementioned magnitude of negative revisions in excess of -14% on an ex-Energy basis show, we have already traveled a fair distance in that direction. Importantly, some key sectors in the path of the Fed’s tightening cycle, like Construction, Retail, Discretionary, and even Technology, have already gotten their 2023 estimates shaved off by a fifth since mid-April.

We are not saying that estimates don’t need to fall any further. If nothing else, estimates for the Finance sector will need to come down in the wake of the ongoing banking industry issues. But rather that the bulk of the cuts are likely behind us, particularly if the coming economic downturn is a lot less problematic than many seem to assume or fear.

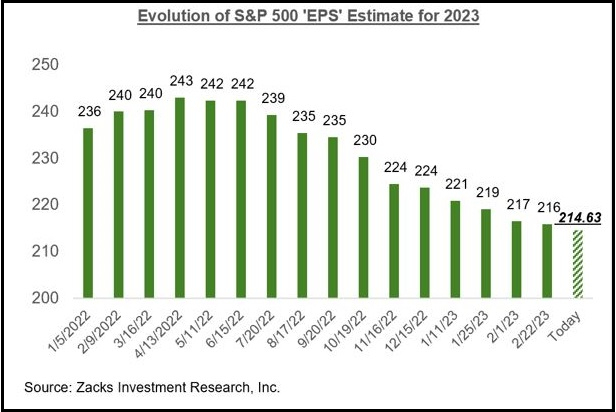

Please note that the $1.904 trillion aggregate earnings estimate for the index in 2023 approximates to an index ‘EPS’ of $214.63, down from $221.08 in 2022. The chart below shows how this 2023 index ‘EPS’ estimate has evolved over time.

Image Source: Zacks Investment Research

The chart below shows the earnings and revenue growth picture on an annual basis.

Image Source: Zacks Investment Research

This Week’s Reporting Docket

The Q1 earnings season will really get underway when JPMorgan (JPM - Free Report) and the other big banks come out with their quarterly results in mid-April. But the reporting cycle has actually gotten underway already, as we saw with results from several bellwether operators like FedEx, Nike, and 15 other S&P 500 members in recent days.

The results from FedEx, Nike, and the other index members that reported in recent days were for their fiscal quarters ending in February. JPMorgan and the banks will report results for their fiscal periods ending March. We and other data vendors count these February-quarter results as part of the 2023 Q1 tally.

We have another 3 S&P 500 members on deck to report such February-quarter results this week, including Conagra, Constellation Brands, and Lamb Weston.

For the 17 S&P 500 members that have reported results already, total earnings are down -26.9% from the same period last year on +4.6% higher revenues, with 82.4% beating EPS estimates and 76.5% beating revenue estimates. The comparison charts below put the Q1 EPS and revenue beats percentages in a historical context.

Image Source: Zacks Investment Research

More By This Author:

Analyzing The Evolving Q1 Earnings Landscape

Analyzing Banking Woes And The Shifting Earnings Landscape

2023 Q1 Earnings Preview: What Are Estimates Telling Us?

Disclosure: Zacks.com contains statements and statistics that have been obtained from sources believed to be reliable but are not guaranteed as to accuracy or completeness. References to any specific ...

more

Priced in Lmao notice banks went down during rally.