T. Rowe Price Group (TROW) the global investment management firm with $1.31 trillion of assets under management, is a sound investment for investors looking for long-term high returns and stable returns in the current bear market.

The company has increased its dividend for over 30 consecutive years, making it a Blue Chip stocks stock, which is a group of more than 350 companies with at least 10 consecutive years of dividend increases.

We see these stocks as among the better dividend stock buys in the market today, simply because of their willingness and ability to return more and more capital to shareholders each year.

This article in the 2022 Blue Chip Stocks In Focus series will analyze T.Rowe Price, including recent earnings, growth prospects, and total returns.

Although the stock has taken a substantial hit due to the weak equity market following the fast tightening of the economy by the FED, it has historically fought back drawdowns. Moreover, the company is positioned in every possible way to be a winner in the long run.

Business Overview

T. Rowe Price Group provides investment management services through its subsidiaries in North America, EMEA, and APAC. The offered products include U.S. mutual funds, sub-advised funds, separately managed accounts, collective investment trusts, and other T. Rowe Price products such as open-ended investment products.

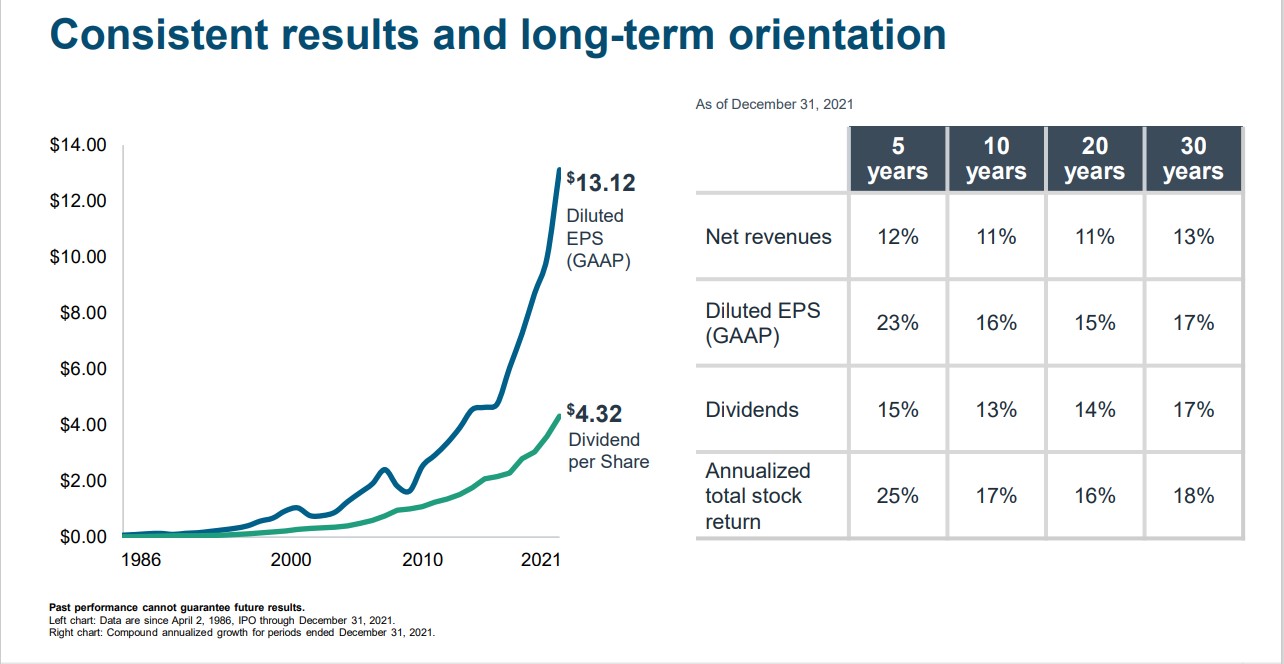

The company has a long track record of generating strong growth.

Source: Investor Presentation

Investment advisory services also provide related administrative services, including distribution, mutual fund transfer agent, accounting, and shareholder services; participant record-keeping and transfer agent services for defined contribution retirement plans; brokerage; trust services; and non-discretionary advisory services through model delivery.

Around 90% of the revenues consist of investment advisory fees. The fee-based revenue model makes T Rowe dependent on its AUM.

Source: Investor Presentation

Growth Prospects

The asset manager has a lot of room for organic growth. Although there have been net outflows in the last two quarters, and the company expects further outflows in the coming months, this does not mean the firm cannot attract new investments. When the time is right, T Rowe has a lot of ways through which it can get cash inflows.

For example, funds that are closed to new investors can be opened. Last year, T. Rowe announced reopening the $38.9 billion fund T. Rowe Price Mid-Cap Growth after closing it in 2010. This is just one example of how the asset manager can increase its AUM, which will increase revenues.

However, the time to attract more AUM would come towards the year-end when there would be more clarity over the looming recession. Thus, the short-term headwinds are not a big concern for this stock.

Additionally, the company’s attempts to enhance its investment capacity, expand its reach, invest in state-of-the-art technology, and strengthen its distribution channels in the US, EMEA, and APAC regions will allow it to maintain sustained growth for the times to come.

T Rowe’s capital management is something one cannot help but admire. The company sits on $2.1 billion cash in Q2 2022, with insignificant long-term debt. This liquidity and cash flow generation have allowed it to return cash to its shareholders in terms of dividends and buyback shares while benefiting from low prices during a volatile environment.

In addition, the company repurchased $510.5 million worth of common stock in the most recent quarter. With a strong balance sheet, the company has also started to look for expansion opportunities through major acquisitions.

T Rowe has been striving for organic growth with only small steps towards inorganic growth through limited and small deals. The acquisition of OHA, completed in December 2021, is a shift in deploying capital towards buying growth. At a time when organic growth in traditional business seems to be slowing down, and competition is becoming intense, the OHA acquisition allows T Rowe to diversify and expand its offerings in alternative investments.

With $57 billion capital under management and 300 employees in global offices, OHA has expanded the global footprint of T Rowe, and we see numerous synergies from these acquisitions in investments as well as distribution channels. We can expect further acquisitions in the future, as hinted in the annual report 2021:

“In order to maintain and enhance our competitive position, we may review acquisition and venture opportunities and, if appropriate, engage in discussions and negotiations that could lead to the acquisition of a new equity or other financial relationships.”

Competitive Advantages & Recession Performance

The competitive environment in asset management will require T Rowe to lower its fees. However, the impressive operating margins of 45-47% are above the industry average, so T Rowe still has the capacity to become more competitive and benefit from increased growth while lowering fees.

T Rowe Price became public in 1986. Since then, the company has fought through various recessions, such as the early 1990s recession, the dot-com bubble of 2001, the great recession due to the financial crisis of 2007-2009, and, more recently, the short-lived COVID-19 recession. We can see in the price chart that the stock took a hit following every recession but followed a prolonged period of sustained growth.

The economic crisis made the stock tumble for a short period; the stock tends to grow during a stable macroeconomic environment. This is because the performance of asset managers is directly related to the economic environment, but also because T Rowe’s management, business model, strategy, and growth prospects are capable enough of getting through these headwinds and carrying on its journey towards growth.

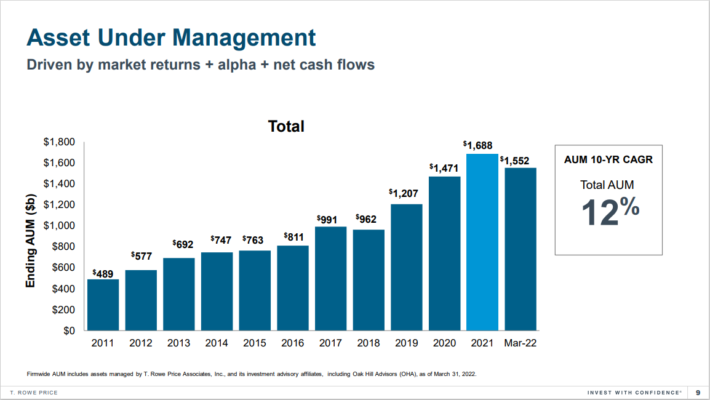

The company employs active investment strategies to generate alpha for its clients. For this purpose, it employs fundamental as well as quantitative analysis, using high-quality data and machine learning techniques to devise its strategies. In addition, it has maintained a record of introducing new strategies and investment vehicles from time to time to expand its offerings and meet the competitive challenge in the industry. As a result, AUM’s 10 YR CAGR, ending 2020, has been 12%.

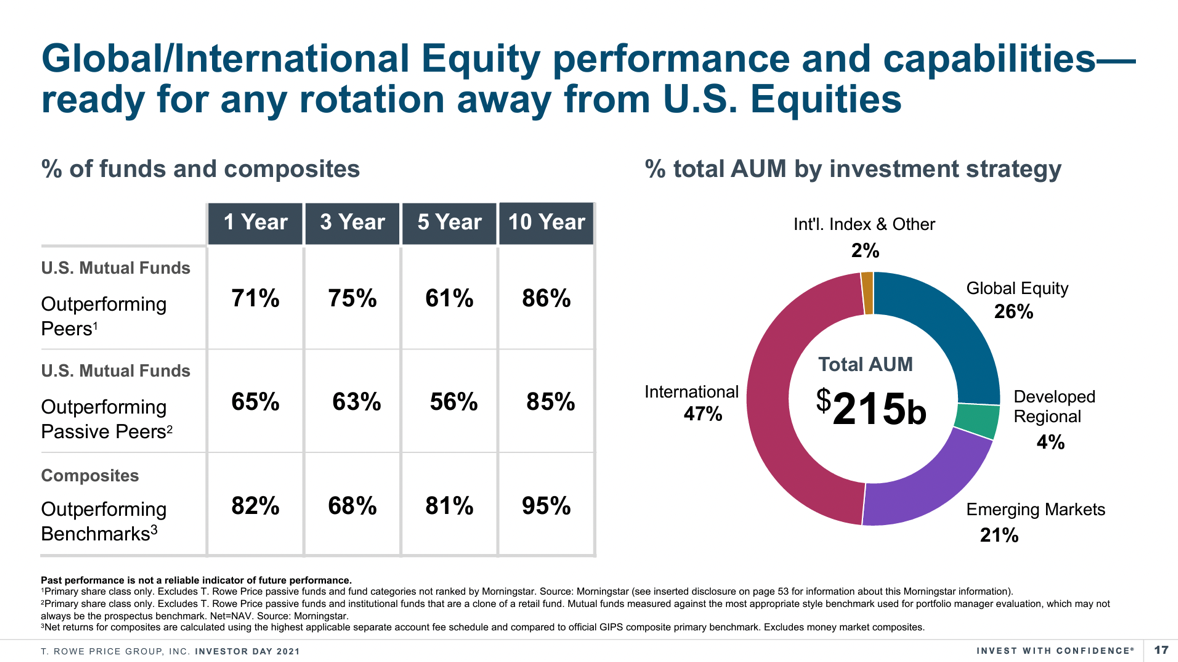

Source: Investor Presentation

The asset manager has outperformed its peers and benchmarks in terms of its Mutual funds’ performance and has also been investing a large proportion of its AUM in international equities to reduce its dependence on the US equities market.

In order to enhance its capacity, the firm has established an additional investment advising subsidiary T. Rowe Price Investment Management, Inc. (TRPIM), with SEC and has announced to transfer sic U.S. Equity and Fixed Income Strategies to TRPIM. Other companies, such as Capital Group, aka American Funds, have adopted this strategy of splitting into more entities to manage capacities. If executed successfully, this will allow the group to manage more investments and implement more strategies with two separate research teams working for each entity.

Although there has been a shift towards passive investing in recent times, the business model and diversity in product offerings make T. Rowe a very strong firm. In addition, the company has been effectively marketing its active strategies and flaunting its results compared to passive competitors. One exhibit of such marketing is this report on how 11 of T. Rowe’s retirement funds have beaten passive competitors over various rolling periods from inception through December 31, 2021, net of fees.

Valuation & Expected Returns

Although headwinds are expected in the short run, a forward PE ratio of 15.63x means that currently, the stock is trading at very attractive multiples. For comparison, BlackRock and Blackstone are currently trading at a forward PE of 20.21x and 19.37x, respectively.

By this year, T Rowe had paid out a regular quarterly dividend of $1.20 per share, a 36th consecutive year of dividend increases since the firm’s IPO in 1986. Last year, the regular quarterly dividend was $1.08 per share, with a special dividend of $3 paid out in the third quarter of 2021.

Shares appear overvalued right now, with a 2022 P/E of 14.9 against our fair value estimate of 14. While we do not expect another special dividend anytime soon, a forward annual dividend yield of 3.6% and a payout ratio of 43.97% make the stock a very attractive investment in times of the bear market.

Final Thoughts

T.Rowe Price stock has had a difficult start to 2022, due to the broader stock market declines. While the stock appears to be overvalued right now, we expect the company to grow its earnings over the next several years. Lastly, the stock has a 3.6% dividend yield, while the company should be able to increase its dividend each year. Total returns are expected at 5.3% at the current share price, making T.Rowe Price stock a hold.

More By This Author:

Blue Chip Stocks in Focus: Black Hills Corporation

Warren Buffett Stocks: RH

Blue Chip Stocks In Focus: Sonoco Products Co.

Comments

Log in or sign up to join the conversation.