President Trump fired Fed Governor Lisa Cook for cause. The President claims,

There is sufficient reason to believe you may have made false statements on one or more mortgage agreements.

This is the first time in the 112-year history of the Fed that a President has fired a Fed Governor. Cook is fighting the dismissal, claiming:

President Trump purported to fire me for cause when no cause exists under the law, and he has no authority to do so.” Given her stance, this issue is likely to be fought in the courts, with no quick resolution.

Between the constant barrage on Fed Chairman Powell from the President, the sudden retirement of Fed Governor Adriana Kugler, and the latest firing of Lisa Cook, the Fed is mired in a soap opera of change. Let’s step back from the headlines and appreciate Lisa Cook’s role at the Fed and why her seat is important for Trump. Cook is one of seven Fed Governors. Fed Governors serve 14-year terms and, importantly, are permanent voting members of the FOMC committee, which sets monetary policy. The New York Fed President is also a permanent voting member. The remaining four seats rotate among the other 11 Federal Reserve presidents.

By removing Cook and replacing the seat with someone of his choosing, Trump will indirectly set the tone for monetary policy for years to come. If Cook is replaced and Congress approves Miran to replace Kugler, Trump will have appointed four of the seven permanent voting members. Further, he will replace Chairman Powell in 2026, pushing the number to five and, importantly, accounting for almost half of the 12 FOMC votes.

Simply, those with dovish views are quickly gaining more voting power. Furthermore, Trump’s wishes for a significantly lower Fed Funds rate are coming closer to reality.

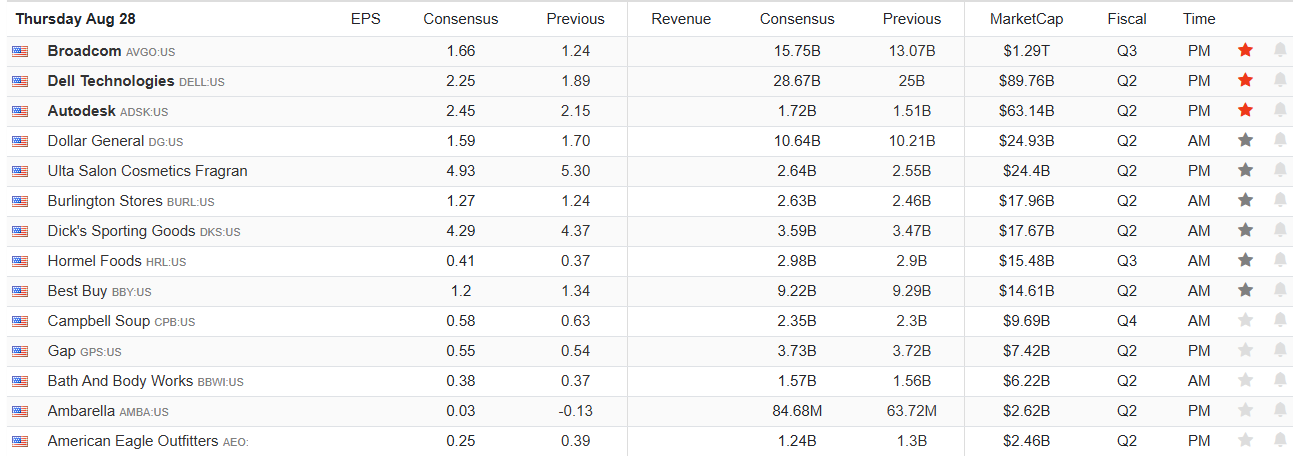

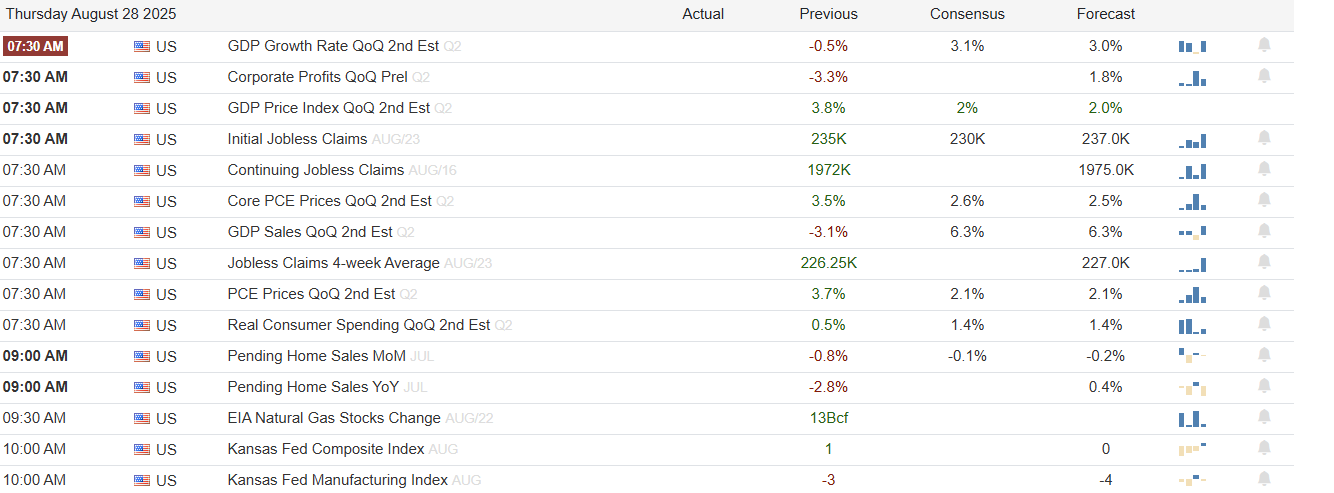

What To Watch Today

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

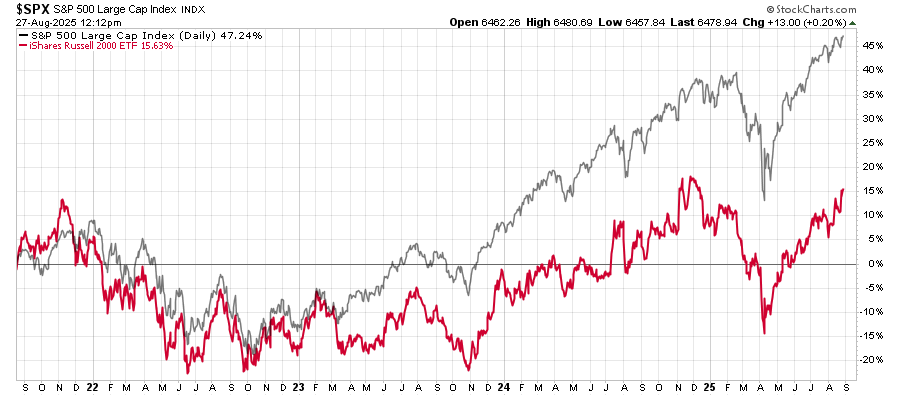

Market Trading Update

Yesterday, we discussed Nvidia’s earnings preview and the potential for its earnings announcement to move the market. The other market area worth paying attention to right now is the Russell 2000 as a proxy for small and mid-capitalization stocks. While the fundamental backdrop of these companies has not changed, roughly 40% are “zombies” and 40% are non-profitable, the recent surge in the index has once again gotten investors overly excited about prospects.

The Russell 2000 is flirting with its previous peaks going back 4 years. A break above those levels would certainly be encouraging, but from an investment perspective, holding IWM has been a losing bet when adjusting for inflation. However, from a trading perspective, it has had terrific runs that excited investors, only to see them repeatedly fail. I suspect, given the sensitivity of small and mid-capitalization companies to economic growth, if the current bout of economic weakness continues, the rally may once again fail.

(Click on image to enlarge)

More notably, as the top chart shows, from an investment perspective, small and mid-caps have underperformed large capitalization stocks over the holding period. That performance gap is shown below. Yes, while the Russell 2000 has certainly rallied significantly from the April lows, the performance gap since October 2022 has been enormous.

(Click on image to enlarge)

While we currently hold mid-capitalization companies in our portfolio, keeping the overall index has been a significant performance drag. Investors need to focus on the underlying fundamentals of small and mid-cap companies and their sensitivity to economic changes, and be selective of their positions. There have been some terrific winners in that basket of stocks, offset by many losers.

Control your risk and trade accordingly. Given their correlation to the broader market, a downturn in large caps could be painful in small and mid-caps.

This Weekend’s Kickoff In The Big Business Of College Football

This weekend, the college football season kicks off in earnest. NCAA football has become a significant business for colleges and some corporations. For instance, total revenues for NCAA Division I Football Bowl Subdivision (FBS) schools are projected to reach nearly $12 billion this year. The dominant conferences, such as the SEC and Big Ten, are each expected to earn almost $2.5 billion each, with some schools earning approximately $100 million in revenue. A good portion of the money comes from media rights deals, sponsorships, ticket sales, and the NCAA playoffs.

It’s not just the colleges benefiting from football. The media, including broadcasters and streamers, have multi-year, multibillion-dollar rights deals. While they pay a substantial fee for the rights to broadcast the games, they also earn significant profits through advertisements, carriage fees, and subscriptions. In addition, the NCAA playoffs are a separate, multibillion-dollar arrangement that boosts profits for many other media interests. Moreover, non-college beneficiaries include apparel brands with outfitting deals, ticket vendors earning fees on secondary sales, data firms licensing statistics, sportsbooks and fantasy platforms buying sponsorships, agencies and NIL collectives brokering endorsements, and bowl organizers/host cities earning from tourism and corporate hospitality.

Momentum Strategies And Physics

In his 1687 book, Philosophiae Naturalis Principia Mathematica, Sir Isaac Newton defined momentum as the product of mass and velocity, or p = m * v. The reason we begin with a physics lesson is that momentum strategies are very popular, and Isaac Newton’s famous formula can teach us a lot about financial asset momentum.

Recently, we have seen rapid shifts in and out of various sectors and stock factors that disrupt momentum strategies. Therefore, understanding how momentum strategies work can help you better identify when they might be effective and when it’s time to switch to a different approach.

(Click on image to enlarge)

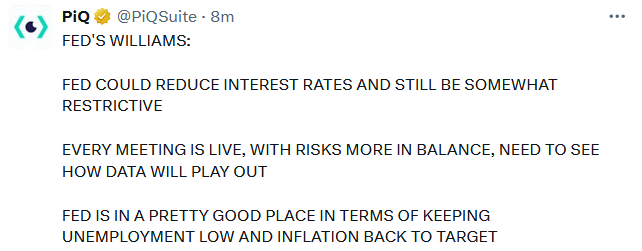

Tweet of the Day

More By This Author:

Smart Money Loves Healthcare: But Are They Now Dumb?Market Internals Weaken

Gold Miners Are Benefitting From The Speculative Boom

Comments

Log in or sign up to join the conversation.