Image Source: Unsplash

Market Recap

Markets held strong through the day up until the Fed rate inaction announcement and subsequent press conference. Broad equity indexes did bounce back slightly but ended the day mixed. Mag 7 exposure in Communication Services (0.31%) and Technology (0.22%) sectors helped lift the Nasdaq Composite 0.15% while the S&P 500 fell 0.12%, the Dow dropped 0.38% and the Russell 2000 closed 0.47% lower. Sectors were lower except for the two mentioned earlier and Utilities (0.74%). The remaining sectors saw results ranging from -0.18% (Healthcare) to -2.02% (Materials).

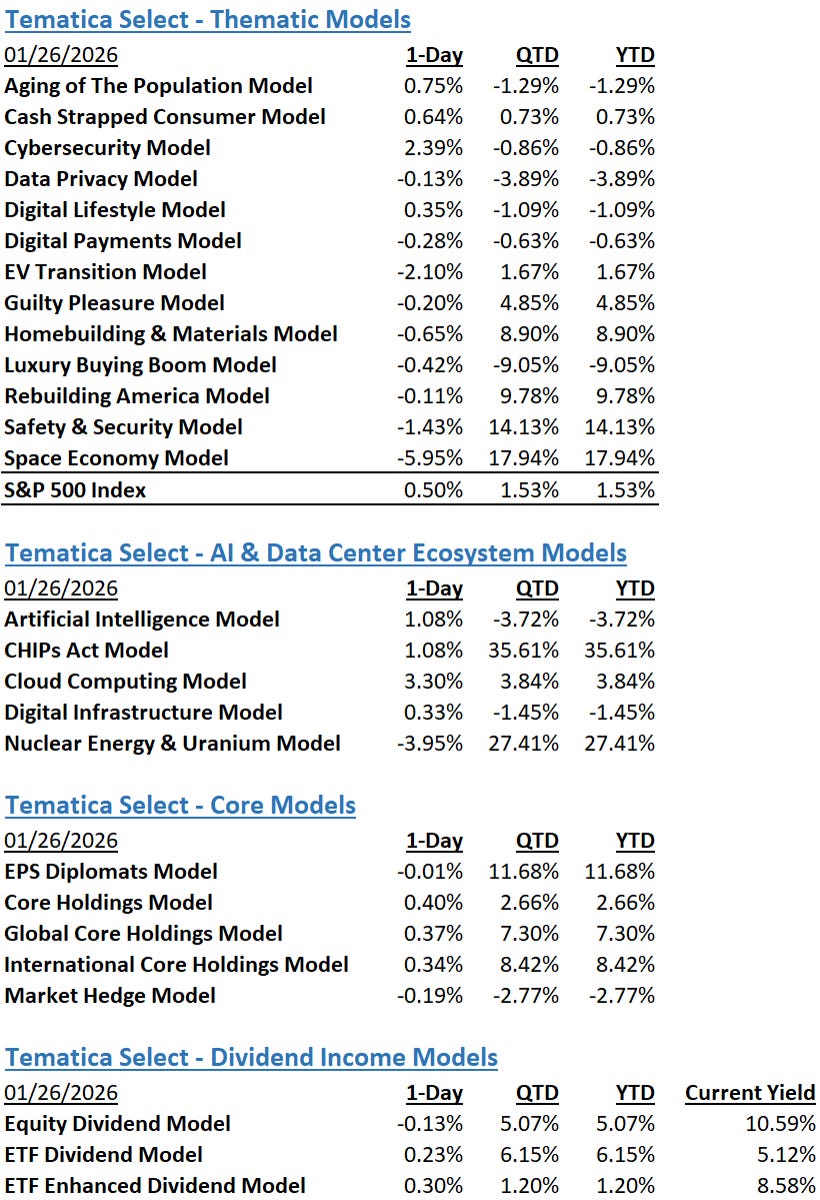

The Tematica Select Model Suite saw mixed results today. Leadership came from Guilty Pleasure (GUILT), buoyed by a strong earnings surprise from Wingstop (WING). Despite seeing its first same-store sales decline in three years, the company exceeded analysts’ expectations and posted beats in revenue and EPS, pushing the name 26.85% higher. EPS Diplomats (DIPLOMATS) and Digital Lifestyle (DLIFE) also topped the leaderboard. Laggards included Luxury Buying Boom (LUXE), Cybersecurity (CYBR), and Homebuilding & Materials (HOMES), as that strategy was weighed down by an unmoving Fed.

AI and Data Center Spending Confirms the AI Trade is Very Much Alive and Well

Fueled by the beat and raise quarters posted by Microsoft (MSFT) and Meta Platforms (META) last night, equity futures are shaking off Fed Chair Powell’s sobering comments about rate cut prospects, pointing to a strong market open later this morning. Microsoft guided Azure growth to 37% year over year in the current quarter and hiked its capital spending for the period to $30 billion, confirming AI demand remains robust and the data center infrastructure shortage continues.

During the June quarter, Meta doubled its capital spending levels year over year to $17 billion, bringing that spending to just over $29 billion for 1H 2025. While Meta narrowed its 2025 capital spending forecast to $66-$72 billion, up from $39.2 billion in 2024, that implies larger spending in 2H 2025. Meta management also shared it sees “another year of similarly significant Capex dollar growth in 2026.” Those collected comments are lifting shares of chip companies Nvidia (NVDA), Marvell (MRVL), and Broadcom (AVGO), and bode very well for our Digital Infrastructure (DIGI) model.

Microsoft, Meta, and Nvidia shares alone account for just over 18% of the S&P 500’s weighting, which helps explain the level of strength we’re seeing in equity futures. Comments and guidance from Microsoft, Meta, and Alphabet (GOOGL) last week set the table for Amazon’s (AMZN) June quarter results and updated capital spending outlook. While it may be a bit premature to say, it sure looks to us like the AI and data center arms race isn’t slowing down. Based on comments already received, we know 2H 2025 capital spending levels will be higher, comments from Amazon will help us better determine how high that spending may be.

While we enjoy the follow-through from last night’s developments, let’s not make a rookie mistake and get so caught up in it that we forget to pay attention to other things going on today and tomorrow. We have the June Personal Income & Spending data out at 8:30 AM ET, which brings with it the latest Personal Consumption Expenditure (PCE) Price Index figures. Expectations for the headline and core PCE do not call for any meaningful improvement.

While we will review the findings, given the inflation comments in the July Flash PMI report, we’re going to focus more on what is found on that front in tomorrow’s July Manufacturing PMI reports and next week’s July Service PMI ones. To be blunt, we do not expect to see any meaningful improvement in their Price data. That collective PMI data will also give us another vantage point on the overall economy and its prospects as we move deeper into the current quarter.

In addition to Amazon’s quarterly results, Apple (AAPL) will also be reporting its June quarter performance, as will a sea of other companies. We expect the usual picking over of Apple’s performance for what is the seasonally weakest for its iPhone business. We expect management to focus on strides in other businesses, but we will be focusing on the mix shift toward the company’s high-margin, recurring revenue Service business.

Our take is that while the market continues to focus on Apple’s hardware business, it is missing the growing influence of the Services vertical, which is helping smooth the company’s earnings profile and delivering cash flow. We suspect Apple will remain somewhat tight-lipped about its upcoming device launches, but we also expect management will need to explain a bit more on its AI strategy, which by all accounts has been rather underwhelming thus far. With that in mind, we are curious to see if management shares any AI usage metrics, especially after the ones Qualcomm (QCOM) discussed last night on its earnings call regarding Samsung:

AI usage in smartphones is increasing. For example, Samsung noted that 70% of Galaxy S25 users are utilizing Galaxy AI, and usage of Google Gemini AI has nearly tripled among S25 users compared to the S24. ~ Qualcomm’s CEO, Cristiano Renno Amon

From our perspective, that comment from Qualcomm reinforces our view that AI adoption in the enterprise, consumer, and government verticals will translate to tight network capacity levels, driving the need for higher enterprise networking and carrier infrastructure spending. Another reason why we are long-term bullish on our Digital Infrastructure (DIGI) model.

More By This Author:

Earnings Continue, Flash July PMI Ahead, Trump To Visit Powell

TSM 2Q 2025 Revenue Stuns, Costco Delivers, Delta Raises The Bar

Will Q3 2025 Guidance Feel The Brunt Of Trump’s Attempt To Regain The Trade Narrative?

Comments

Log in or sign up to join the conversation.