Image Source: Pexels

Well, it had to happen at some point, so why not yesterday? Nvidia (NVDA) crossed the $4 trillion market cap mark and into valuation history, once again. For anyone wondering what exactly merits this kind of valuation, we suggest you take a few minutes to watch this 2008 video of MythBusters hosts Adam Savage and Jamie Hyneman running a parallel processing demonstration. The basic value-add premise hasn’t changed all that much since then and as long as the company continues to deliver we don’t see how or why Nvidia falls off its current perch. Final note on the company is that even at a $4 trillion market cap and a 32.5 forward P/E, it still sports a fairly reasonable PEG (P/E to Growth) ratio of 1.3 per data from Factset.

Needless to say, MAG 7 and technology names were additive to broad equity indexes as evidenced by the Dow gaining 0.49%, the S&P 500 adding 0.61%, and the Nasdaq Composite rising 0.94%. Small caps led the way higher with the Russell 2000 closing up 1.07%. Sector were mostly higher with Real Estate (-0.05%) essentially flat, and Energy and Consumer Staples falling 0.51% and 0.65%, respectively. Staples saw producers like Coca-Cola (KO), Hershey (HSY), Monster Beverage (MNST), Mondelez (MDLZ) and Altria Group (MO) contribute to just over 70% of that sector’s result. The remaining sectors saw returns ranging from 0.26% (Communication Services) to 0.94% (Utilities).

MAG 7 pull was also evident in the top 10 contributors to return for the SPDR S&P 500 Trust ETF (SPY) as all but Tesla (TSLA) combined to account for 70% of the fund’s 0.60% result, 80% if you include Broadcom (AVGO). The relative narrowness of yesterday’s rally also showed up in a 304 to 199 advance/decline line for holdings of SPY.

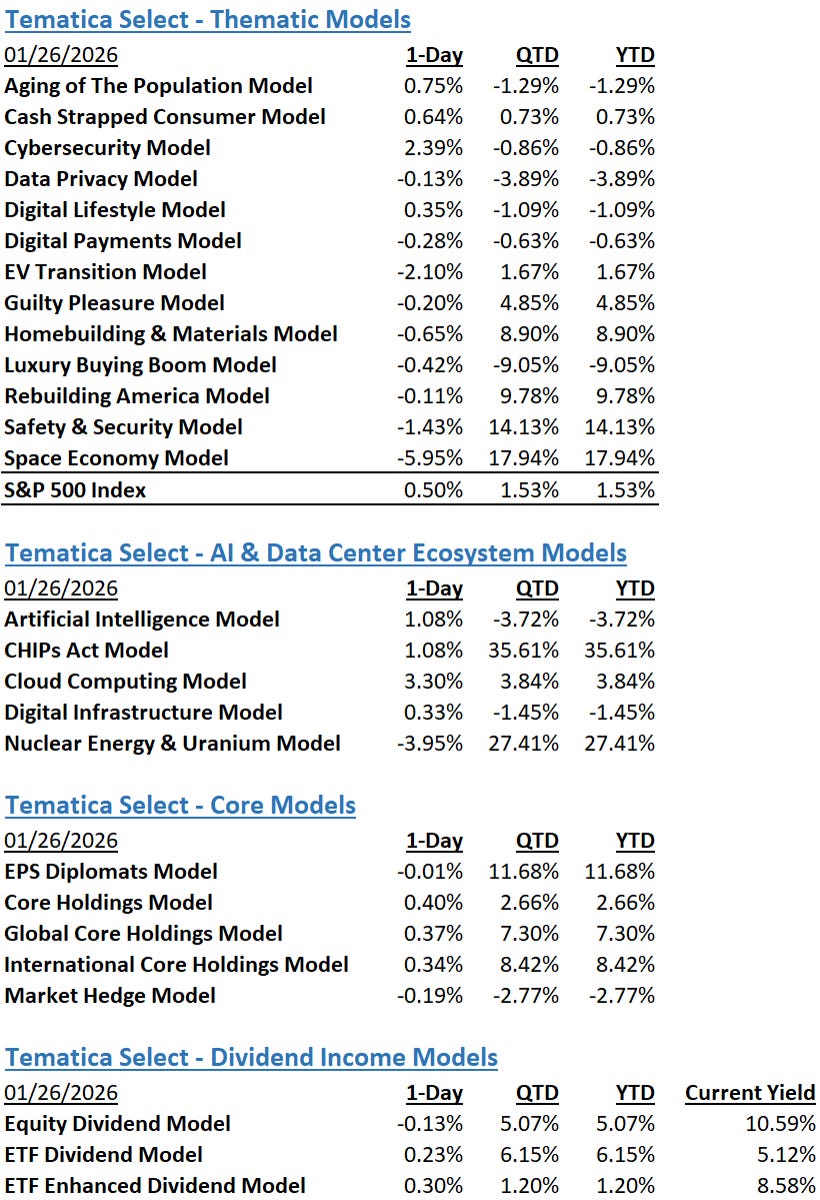

The Tematica Select Model Suite saw positive results across the board except for CHIPs Act (CHIPS) and Market Hedge (HEDGE), of course. Leadership came from Homebuilding & Materials (HOMES) while Space Economy(SPACE), EV Transition (EVTRANS) and EPS Diplomats (DIPLOMATS) also notched relatively strong results. Relative laggards included Core Holdings (CORE) and Guilty Pleasures (GUILT).

TSM 2Q 2025 Revenue Stuns, Costco Delivers, Delta Raises the Bar

Equity futures are off their lows following strong June revenue results from Taiwan Semiconductor (TSM) that cap a robust Q2 2025 with revenue up 39% year over year and low double digits sequentially. The company will report its quarter next week, and its outlook for 2H 2025 by end market and capital spending will be top of mind.

Also helping this morning’s futures rebound is Delta’s (DAL) summer travel outlook, which topped expectations due to continued strength in high-end demand. Delta also reinstated full-year guidance at $5.25-$6.25, down from its January forecast of $7.35, after pulling its guidance in April due to global trade concerns. In our view, that raises the bar for airline earnings, especially those that may have been contemplating holding off issuing guidance amid renewed trade and tariff uncertainty.

We see those data points supporting our Artificial Intelligence, Digital Infrastructure, and Luxury Buying Boom models, while Costco’s June revenue reported last night does the same for our Cash-Strapped Consumer one. The membership-only retail chain saw an 8% rise in monthly net sales to $26.44 billion, with total comp sales excluding gasoline prices and forex impact up 6.2% for June. Adjusted US comp sales grew 5.5% year over year.

As we move into the second half of Amazon’s (AMZN) Prime Day event that runs through Friday, July 11, Adobe Analytics (ADBE) estimates the company raked in $7.9 billion in US sales on Tuesday. That makes it the "single biggest e-commerce day so far this year" per Adobe, and for those keeping score, it also eclipsed total online spending during Thanksgiving last year, when sales on the holiday reached $6.1 billion. Our view is that the event will be a showcase for the intersection of our Cash-Strapped Consumer and Digital Lifestyle models, as will competing efforts from Walmart (WMT), Target (TGT), and other retailers.

But make no mistake, it’s not easy out there. Claire's Stores Inc. is considering a potential bankruptcy for its US operations due to weak demand and higher import costs. Helen of Troy (HELE) missed June quarter expectations with the management team sharing that tariff-related impacts made up “approximately 8 percentage points of the 10.8% consolidated revenue decline.”

We’ll be interested in the comments from ConAgra (CAG) this morning and this afternoon from Levi Strauss (LEVI)about consumer spending. Recent data points to consumers slowing their restaurant spend, while Kroger (KR)upped its comp sales guidance for the balance of the year. Should ConAgra’s outlook confirm that outlook, it would be a positive for several holdings in our Cash-Strapped Consumer model.

As we watch these developments and get ready for Big Bank earnings, the S&P 500 is back in overbought territory given its relative strength index (RSI) level, and the Nasdaq Composite is knocking on that door. Meanwhile, the Volatility Index below 16 indicates a market filled with complacency, and the Fear & Greed Index is flashing “Extreme Greed”. When we’ve seen this combination before, it’s been a good time to tread carefully, and for more risk-tolerant folks, it may be time to revisit our Market Hedge model.

More By This Author:

Will Q3 2025 Guidance Feel The Brunt Of Trump’s Attempt To Regain The Trade Narrative?Trade Deal Realities Bring Potential Market Headwinds

TSM May Revenue Soars, Multiple Models Leading The Market QTD

Comments

Log in or sign up to join the conversation.