Image: Shutterstock

The need for social distancing has become less of a driver for the e-commerce segment, which includes pure-plays as well as traditional retailers with e-commerce capabilities. That’s because, as estimates from the Commerce Department indicate, some of the traffic that moved online during the initial months of the pandemic is moving back to stores.

Accordingly, e-commerce sales in the last quarter were 39.1% above 1Q20 (up 7.7% sequentially), with total retail sales increasing 16.8% (up 7.8% sequentially). Ecommerce accounted for around 13.6% of total U.S. retail sales, which is about level with the preceding two quarters, lower than the 15.7% share in the June 2020 quarter and higher than the 11.4% share in the year-ago quarter.

Therefore, as the above stats also show, e-commerce continues to grow strongly off an admittedly smaller base to take a bigger share of the total retail pie. And this is helped by the race to digitization, consumer habits altering for good, and supply chains adjusting to help the two sides meet.

Also, while there may be some moderation in absolute growth numbers this year, it is because of difficult comps, and it’s clear that e-commerce continues to grow its share of total retail. So, growth is less of a negative for this group as is valuation, which remains rich despite the sell-off in the last few months. Certain names worth considering now are Overstock.com, Alibaba, and ASOS plc.

About The Industry

Electronic commerce, the buying/selling of goods and services via a software platform, continues to evolve as the technologies driving it advance.

On the one side are user devices (including voice-controlled ones), which are getting bigger, brighter, and more capable. On the other are software platforms facilitating transactions, which are getting AI-enabled, sometimes including AR/VR and getting generally more sophisticated, and thereby, more capable of delivering user satisfaction. Social commerce and chatbots are facilitating the back-end.

Differentiation comes from better technology for improved showcasing, easier navigation and payment, speedier delivery and returns, brand building, comparison shopping, loyalty, etc. which generally tip the scale in favor of larger players. Particularly

Factors Shaping the Future of the Internet-Commerce industry:

- The pandemic has proved extremely beneficial for e-commerce players, and not just because of the government-mandated stay-home orders that led to soaring business volumes. Markets have been open across the country for a couple of quarters now, but purchasing trends haven’t gone back to where they were before. Just like many companies temporarily adopting work-from-home practices are expected to make it a broader trend, many shoppers that preferred going to stores earlier have now had a taste of the convenience of online shopping. One thing this trend should boost (if technology companies are up to it) is the adoption of AR/VR technology because of its potential to greatly enhance showcasing. The technology is already being leveraged very effectively in the housing market. Also, the ability to fit things like furniture or other items where people want it in their homes is better even than physical retail. More stores will likely be converted into delivery hubs to facilitate this trend.

- As American companies like Amazon and Walmart continue their march to conquer the world, it’s relevant for this outlook to include data that goes beyond the borders. So, according to eMarketer’s projections, global retail e-commerce is expected to decelerate from 27.6% growth in 2020 to 14.3% growth in 2021 even as total retail sales go from down 3.0% to up 5.1%. eMarketer has updated its U.S. market expectations for 2021. Earlier, it was expecting U.S. e-commerce sales to decelerate from 32.4% growth last year to 6.1% this year. It is now forecasting 17.9% growth this year with e-commerce contributing 15.3% of total retail sales. Total retail was earlier expected to improve from a decline of 3.2% in 2020 to an increase of 1.6% in 2021. It is now expected to grow 7.9% this year. The categories expected to see the strongest eCommerce growth this year include apparel and accessories (to grow 18.9%, there is pent up demand and a third of the shopping has moved online), food/beverage (to grow 18.1%, driven by digital groceries, a spillover effect of at-home cooking), health/personal care/beauty (16.1%), auto and parts (13.5%), toys and hobbies (13.1%) and furniture and home furnishings (12.3%). The categories generating a majority of their sales online are books/music/video (69.1%) and computer/consumer electronics (53.2%, after a stellar 2020). These two will grow 12.5% and 9.1%, respectively. Amazon accounts for 83.2% of all e-commerce sales in the books/music/video category and 50.2% of all online computer/consumer electronics sales. It accounts for more than a quarter of U.S. e-commerce sales in every category other than auto/parts. This year, traditional retailers will double down on digital initiatives including click and collect, cashier-less checkout, contactless payment, and digital signage while online retailers focus on social commerce, grocery sales, and the buy-now-pay-later option.

- Both e-commerce pure-plays and traditional retailers branching into e-commerce are seeing a surge in e-commerce sales. However, physical presence remains important because it is only proximity to a consumer that can facilitate quick delivery. So the trend moving retailers toward a hybrid/omnichannel model that customers can get quick delivery from, or from where they can pick up the items ordered online (BOPIS, curbside pickup), at their convenience, and through apps arranging personal shoppers, is likely to remain. Self-driven delivery vehicles and drones are already on the horizon to deal with logistics problems and make deliveries smoother and cheaper.

- Also, data mining has never been easier. Because of the many details involved in satisfying a customer, data mining has grown in importance over the years, with the party controlling the customer’s data being best positioned to identify and service demand while also delivering the desired experience. Most of the big e-commerce players are also into payments processing, which gives them further insight into a customer’s tastes, preferences, and buying habits. As machines read and process this data, they can create programs and processes to maximize customer satisfaction and drive sales. Artificial intelligence such as that used by companies like Amazon already decides how competitive a player is. But as time goes by, more and more retailers are jumping on board and harnessing big data that has become imperative for survival.

All said revenue growth rates may be expected to remain very strong as a result of more companies moving online and existing players utilizing more advanced tools and analytics to increase their return on investment. But profitability could come in for some pressure (for some) as companies invest heavily in building out infrastructure.

Zacks Industry Rank Reflects Uncertain Prospects

The Zacks Electronic - Commerce Industry is a rather large group within the broader Zacks Retail And Wholesale Sector. It carries a Zacks Industry Rank of #228, which places it in the bottom 9% of more than 250 Zacks industries.

Our research shows that the top 50% of the Zacks-ranked industries outperform the bottom 50% by a factor of more than 2 to 1. So the group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates strong near-term prospects.

The industry’s positioning in the bottom 50% of the Zacks-ranked industries is a result of its relative performance versus others. As far as aggregate estimate revisions are concerned, it appears that analysts expect earnings to decline this year and the next on revenue that will also decline, although at a lower rate.

The net decline in the 2021 and 2022 earnings estimates are 16.1% and 37.5%. The net decline in the revenue estimate for 2021 is 9.5% and for 2022 is 4.9%. The delta is mostly because of difficult comps, coming off the extremely strong 2020 results, on top of the increased cost of operation and amortization and other charges related to infrastructure buildup.

Before we present a few stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

Industry Lags On Shareholder Returns

The Zacks Electronic - Commerce Industry is trading at a discount to both the broader Zacks Retail and Wholesale Sector as well as the S&P 500 index over the past year. This is because of the changing sentiment, as physical stores open up, taking back some of the sales that moved online during the pandemic.

So we see that the stocks in this industry have collectively lost 5.9% of their value over the past year, compared to the broader Zacks Retail and Wholesale Sector’s 18.6% gain and the Zacks S&P 500 Composite’s 38.0% gain.

One-Year Price Performance

Image Source: Zacks Investment Research

Industry's Current Valuation

On the price-to-forward 12 months’ earnings (P/E) basis, the industry still looks grossly overvalued (41.20X) with respect to both the S&P 500 (21.85X) and the broader retail sector (28.00X).

On the basis of forward 12 months’ sales (P/S) however, the industry’s multiple of 3.92X trails the S&P 500’s 4.81X although it remains understandably higher than the sector’s 1.38X. Over the past year, the industry has traded as high as 5.66X, as low as 3.91X, and at the median of 4.77X, as the chart below shows.

Forward 12 Month Price-to-Sales (P/S) Ratio

Image Source: Zacks Investment Research

3 Stocks Standing Out

Overstock.com, Inc. (OSTK Quick Quote OSTK - Free Report): Overstock.com is primarily an e-commerce service provider focused on home furnishing. The company sells its broad range of price-competitive products, including furniture, home decor, bedding and bath, and houseware through its www.overstock.com, www.o.co, and www.o.biz websites. This business contributes 90% of its revenue. The rest of the business deals in blockchain and financial technology.

Overstock’s focus on the home furnishings segment, which is in turn benefiting from the housing shortage and increased digitization of home furnishings sales, makes it an attractive play. The pandemic also drove the company to improve its tech platform, through ML/AI and facilitating easier navigation, refined searches, and better content. It has also improved efficiencies on the logistics side, thereby saving costs.

The Zacks Rank #1 company has seen a 79.9% increase in its 2021 earnings estimate and a 53.0% increase in its 2022 estimate in the last 60 days.

The shares are up 299.3% over the past year.

Price Performance: OSTK

Image Source: Zacks Investment Research

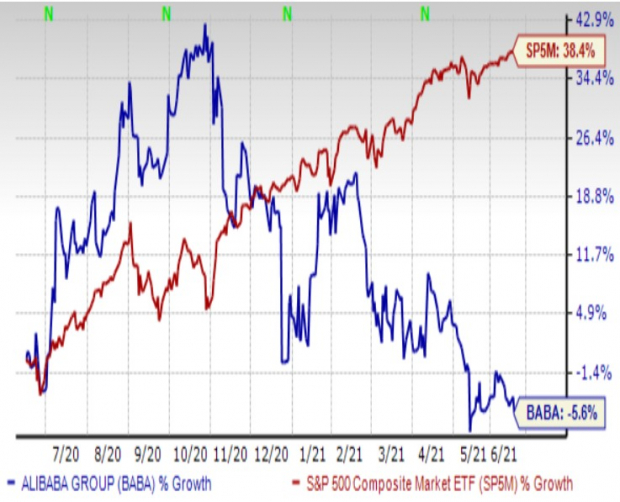

Alibaba Group Holding Limited (BABA Quick Quote BABA - Free Report): Alibaba Group Holding is one of the leading e-commerce giants in China. Alibaba.com, Taobao, and Tmall, its three main online platforms generate huge volumes and account for more than half of all online retail sales in China, where online sales just surpassed in-store sales in the last quarter. Over the last few years, the company has transformed itself from being a traditional e-commerce company to a conglomerate that has businesses ranging from logistics and food delivery to cloud computing.

The company’s leadership in the fragmented and fast-growing Chinese e-commerce market, the breadth of its products, continued innovation, and ability to cater to strong demand following the pandemic are expected to generate very strong results in the foreseeable future.

The Zacks Consensus Estimate for the current-year EPS is up 6.2% in the last 60 days while the estimate for the following year is up 12.6%.

The Zacks Rank #3 (Hold) stock is down 3.2% over the past year, as investors appear to be discounting the stock because of issues the company seems to be having with the Chinese government. As a result, the shares are going really cheap. It’s worth keeping in mind however that Alibaba is too important to China’s overall growth strategy, so any issues with the government are likely to be temporary.

Price Performance: BABA

Image Source: Zacks Investment Research

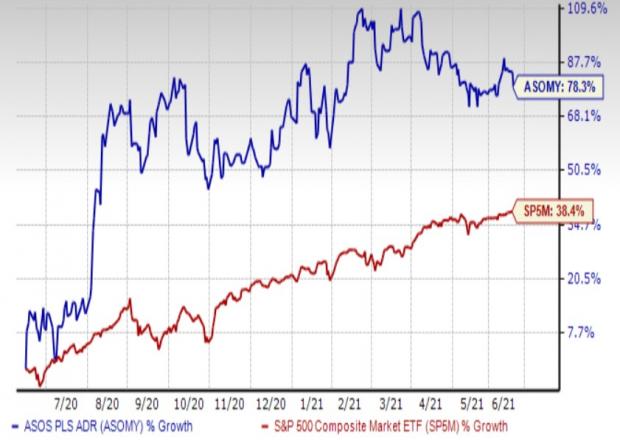

ASOS plc (ASOMY Quick Quote ASOMY - Free Report): This is a British provider of fashion goods including womenswear and menswear, footwear, accessories, jewelry, and beauty and grooming products that are sold through its website, asos.com. It operates in the UK, France, Germany, Italy, Spain, Australia, the U.S., Russia, and China.

The company has recently picked up the famous Topshop, Topman, and Miss Selfridge brands from Arcadia, which went out of business. ASOS has also seen the same pandemic-driven surge in its results that other e-commerce players in the U.S. have seen. With the reopening of the economy and release of pent-up demand for apparel and accessories, it should continue to do well this year.

This Zacks Rank #3 stock’s current year and next year EPS estimates are both up 4 cents in the last 60 days.

Its shares are up 78.3% over the past year.

Price and Performance: ASOMY

Image Source: Zacks Investment Research

Comments

Log in or sign up to join the conversation.