Image Source: Pixabay

Warren Buffett is the Chairman and CEO of Berkshire Hathaway (BRK-A)(BRK-B). As of its most recent quarterly filing, Berkshire Hathaway has an equity investment portfolio worth approximately $258 billion.

Berkshire Hathaway’s portfolio is filled with quality stocks, many of which pay dividends to shareholders. Some have even paid rising dividends each year, for decades on end.

Income investors can find many quality dividend stocks among Berkshire’s portfolio.

This article analyzes Warren Buffett’s top 10 highest-yielding stocks based on information disclosed in the Q2 2025 13F filing.

Warren Buffett & Dividend Stocks

Buffett has grown his wealth by investing in and acquiring businesses with strong competitive advantages trading at fair or better prices.

Most investors know Warren Buffett looks for quality, but few know the degree to which he invests in dividend stocks:

- All of Warren Buffett’s top 10 stocks pay dividends

- His top 5 holdings have an average dividend yield of ~2.2% (and make up 70% of his portfolio)

- Many of his dividend stocks have paid rising dividends over decades

Keep reading this article to see Warren Buffett’s 10 highest yielding stock selections analyzed.

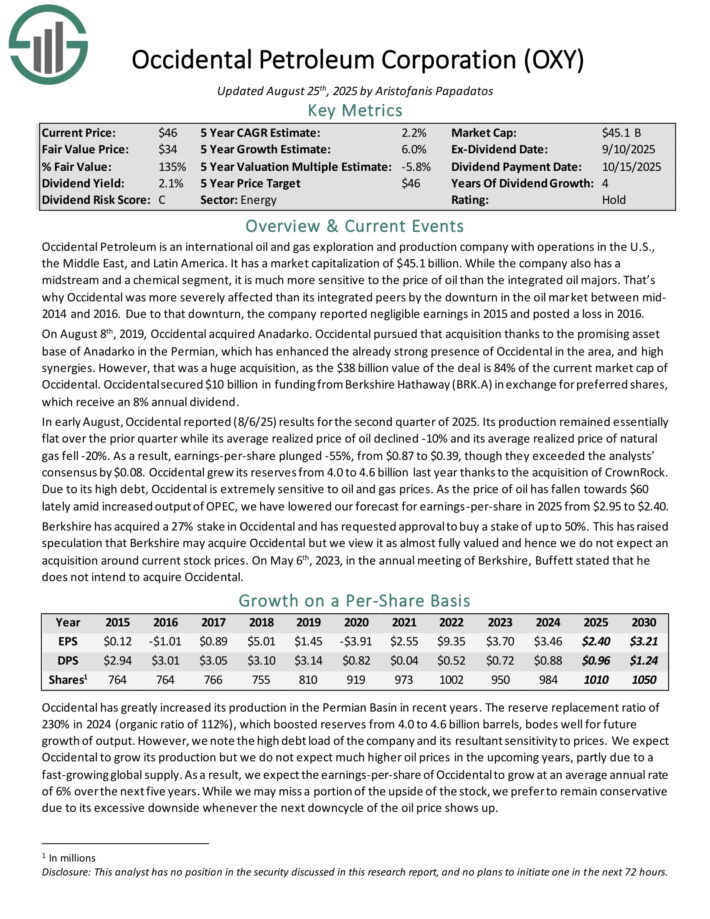

#10: Occidental Petroleum (OXY)

Dividend Yield: 2.0%

Occidental Petroleum is an international oil and gas exploration and production company with operations in the U.S., the Middle East, and Latin America. While the company also has a midstream and a chemical segment, it is much more sensitive to the price of oil than the integrated oil majors.

In early August, Occidental reported (8/6/25) results for the second quarter of 2025. Its production remained essentially flat over the prior quarter while its average realized price of oil declined -10% and its average realized price of natural gas fell -20%.

As a result, earnings-per-share plunged -55%, from $0.87 to $0.39, though they exceeded the analysts’ consensus by $0.08. Occidental grew its reserves from 4.0 to 4.6 billion last year thanks to the acquisition of CrownRock.

Due to its high debt, Occidental is extremely sensitive to oil and gas prices. As the price of oil has fallen towards $60 lately amid increased output of OPEC, we have lowered our forecast for earnings-per-share in 2025 from $2.95 to $2.40.

Click here to download our most recent Sure Analysis report on OXY (preview of page 1 of 3 shown below):

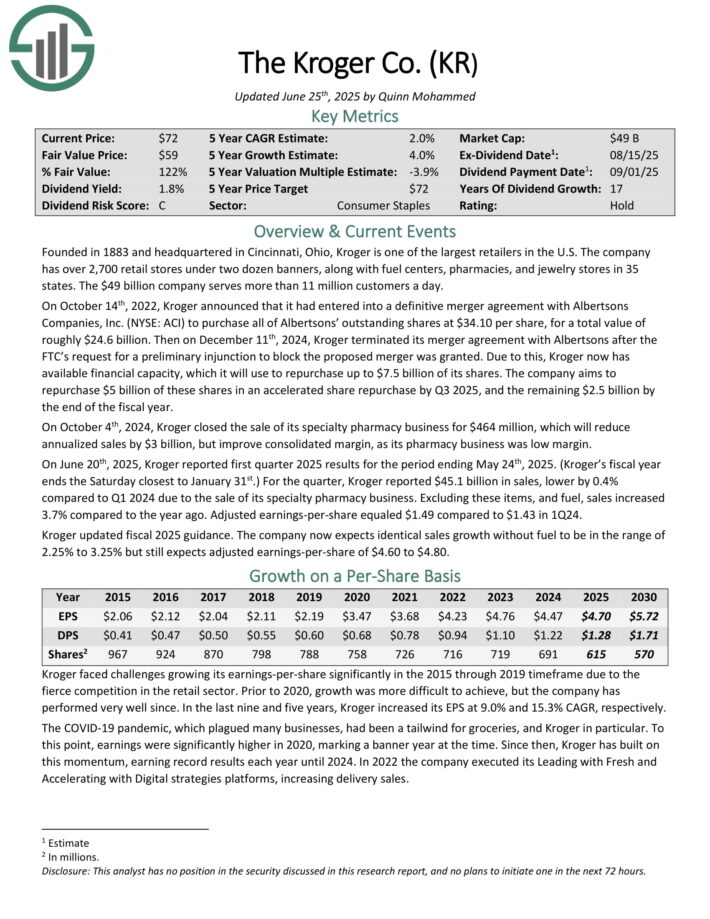

#9: The Kroger Co. (KR)

Dividend Yield: 2.1%

Founded in 1883 and headquartered in Cincinnati, Ohio, Kroger is one of the largest retailers in the U.S. The company has nearly 2,800 retail stores under two dozen banners, along with fuel centers, pharmacies and jewelry stores in 35 states.

On June 20th, 2025, Kroger reported first quarter 2025 results for the period ending May 24th, 2025. (Kroger’s fiscal year ends the Saturday closest to January 31st.) For the quarter, Kroger reported $45.1 billion in sales, lower by 0.4% compared to Q1 2024 due to the sale of its specialty pharmacy business.

Excluding these items, and fuel, sales increased 3.7% compared to the year ago. Adjusted earnings-per-share equaled $1.49 compared to $1.43 in 1Q24.

Kroger updated fiscal 2025 guidance. The company now expects identical sales growth without fuel to be in the range of 2.25% to 3.25% but still expects adjusted earnings-per-share of $4.60 to $4.80.

Click here to download our most recent Sure Analysis report on Kroger (preview of page 1 of 3 shown below):

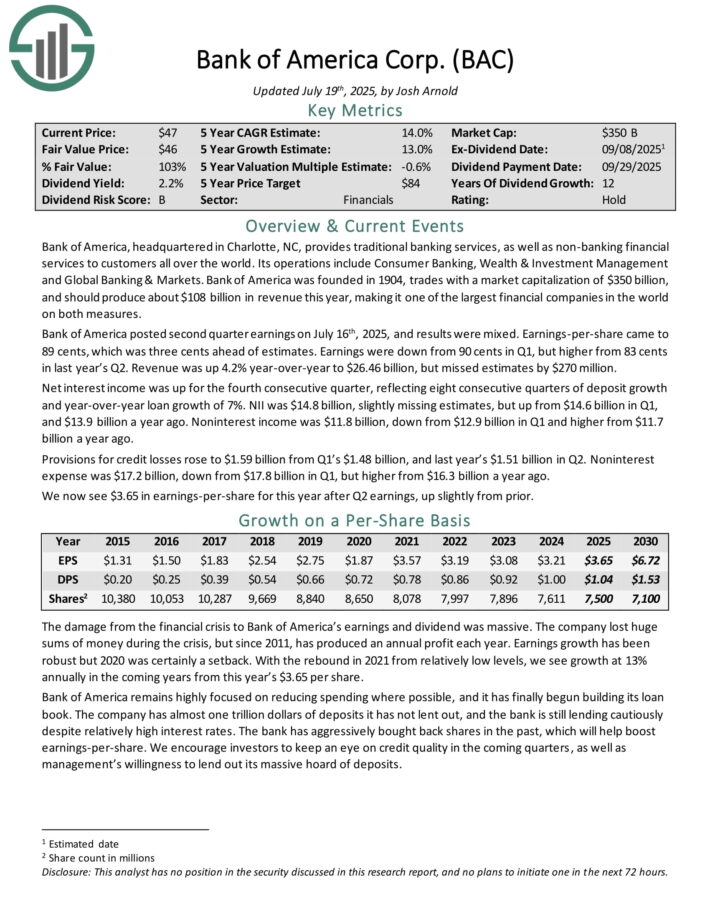

#8: Bank of America Corporation (BAC)

Dividend Yield: 2.2%

Bank of America, headquartered in Charlotte, NC, provides traditional banking services, as well as non–banking financial services to customers all over the world. Its operations include Consumer Banking, Wealth & Investment Management and Global Banking & Markets.

Bank of America posted second quarter earnings on July 16th, 2025, and results were mixed. Earnings-per-share came to 89 cents, which was three cents ahead of estimates. Earnings were down from 90 cents in Q1, but higher from 83 cents in last year’s Q2. Revenue was up 4.2% year-over-year to $26.46 billion, but missed estimates by $270 million.

Net interest income was up for the fourth consecutive quarter, reflecting eight consecutive quarters of deposit growth and year-over-year loan growth of 7%. NII was $14.8 billion, slightly missing estimates, but up from $14.6 billion in Q1, and $13.9 billion a year ago. Noninterest income was $11.8 billion, down from $12.9 billion in Q1 and higher from $11.7 billion a year ago.

Click here to download our most recent Sure Analysis report on Bank of America (preview of page 1 of 3 shown below):

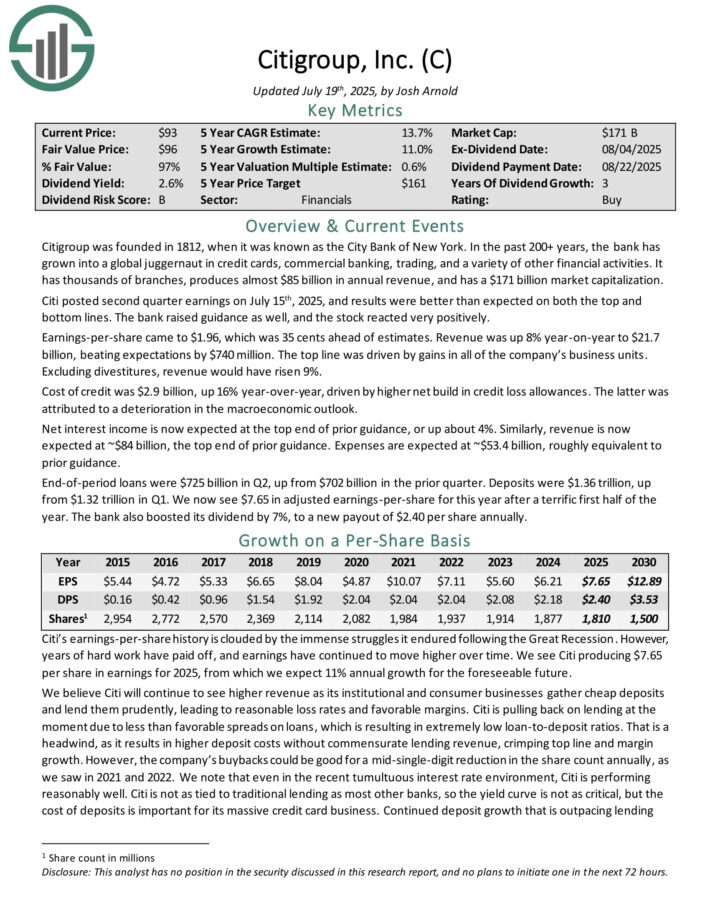

#7: Citigroup Inc. (C)

Dividend Yield: 2.5%

Citigroup was founded in 1812, when it was known as the City Bank of New York. In the past 200+ years, the bank has

grown into a global juggernaut in credit cards, commercial banking, trading, and a variety of other financial activities.

Citi posted second quarter earnings on July 15th, 2025, and results were better than expected on both the top and bottom lines. The bank raised guidance as well, and the stock reacted very positively.

Earnings-per-share came to $1.96, which was 35 cents ahead of estimates. Revenue was up 8% year-on-year to $21.7 billion, beating expectations by $740 million. The top line was driven by gains in all of the company’s business units. Excluding divestitures, revenue would have risen 9%.

Cost of credit was $2.9 billion, up 16% year-over-year, driven by higher net build in credit loss allowances. The latter was attributed to a deterioration in the macroeconomic outlook.

Net interest income is now expected at the top end of prior guidance, or up about 4%. Similarly, revenue is now expected at ~$84 billion, the top end of prior guidance. Expenses are expected at ~$53.4 billion, roughly equivalent to prior guidance.

End-of-period loans were $725 billion in Q2, up from $702 billion in the prior quarter. Deposits were $1.36 trillion, up from $1.32 trillion in Q1.

Click here to download our most recent Sure Analysis report on Citigroup (preview of page 1 of 3 shown below):

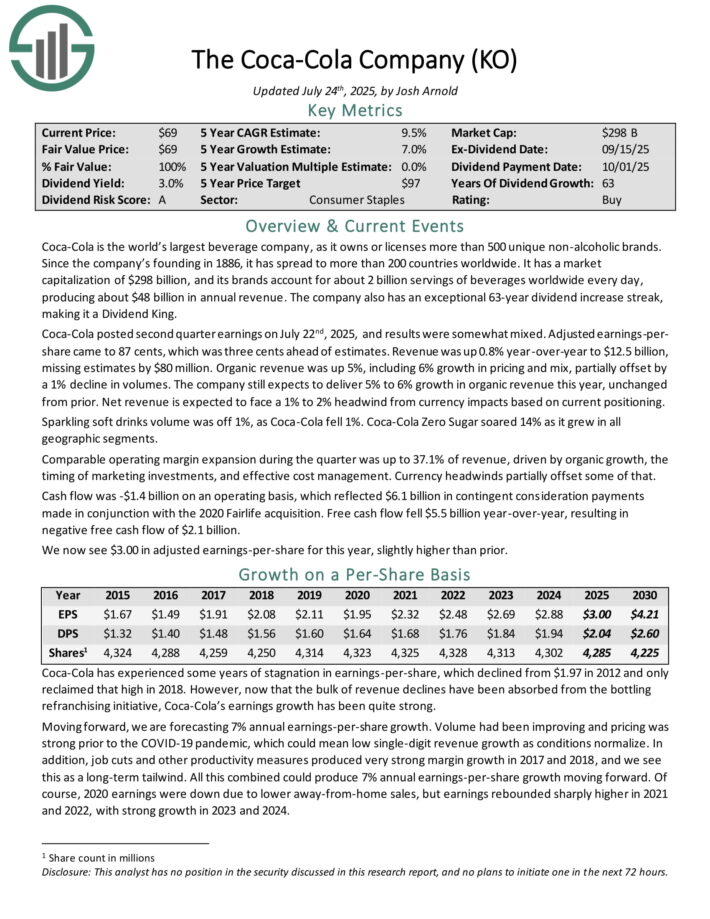

#6: The Coca-Cola Company (KO)

Dividend Yield: 3.0%

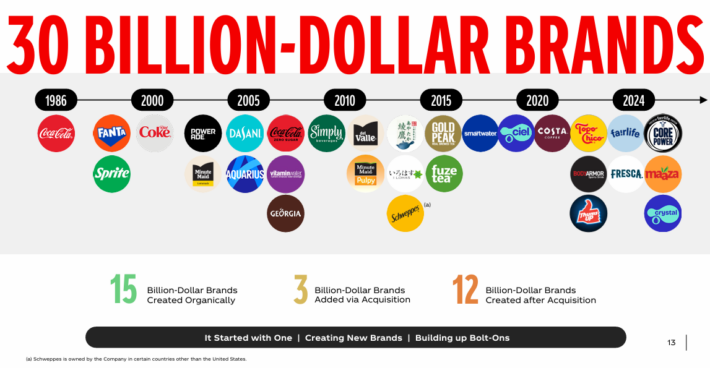

Coca-Cola is the world’s largest beverage company, as it owns or licenses more than 500 unique non–alcoholic brands. Since the company’s founding in 1886, it has spread to more than 200 countries worldwide.

Coca-Cola now has 30 billion-dollar brands in its portfolio, which each generate at least $1 billion in annual sales.

Source: Investor Presentation

Coca-Cola posted second quarter earnings on July 22nd, 2025, and results were somewhat mixed. Adjusted earnings-per-share came to 87 cents, which was three cents ahead of estimates. Revenue was up 0.8% year-over-year to $12.5 billion, missing estimates by $80 million.

Organic revenue was up 5%, including 6% growth in pricing and mix, partially offset by a 1% decline in volumes. The company still expects to deliver 5% to 6% growth in organic revenue this year, unchanged from prior. Net revenue is expected to face a 1% to 2% headwind from currency impacts based on current positioning.

Sparkling soft drinks volume was off 1%, as Coca-Cola fell 1%. Coca-Cola Zero Sugar soared 14% as it grew in all geographic segments. Comparable operating margin expansion during the quarter was up to 37.1% of revenue, driven by organic growth, the timing of marketing investments, and effective cost management. Currency headwinds partially offset some of that..

Click here to download our most recent Sure Analysis report on KO (preview of page 1 of 3 shown below):

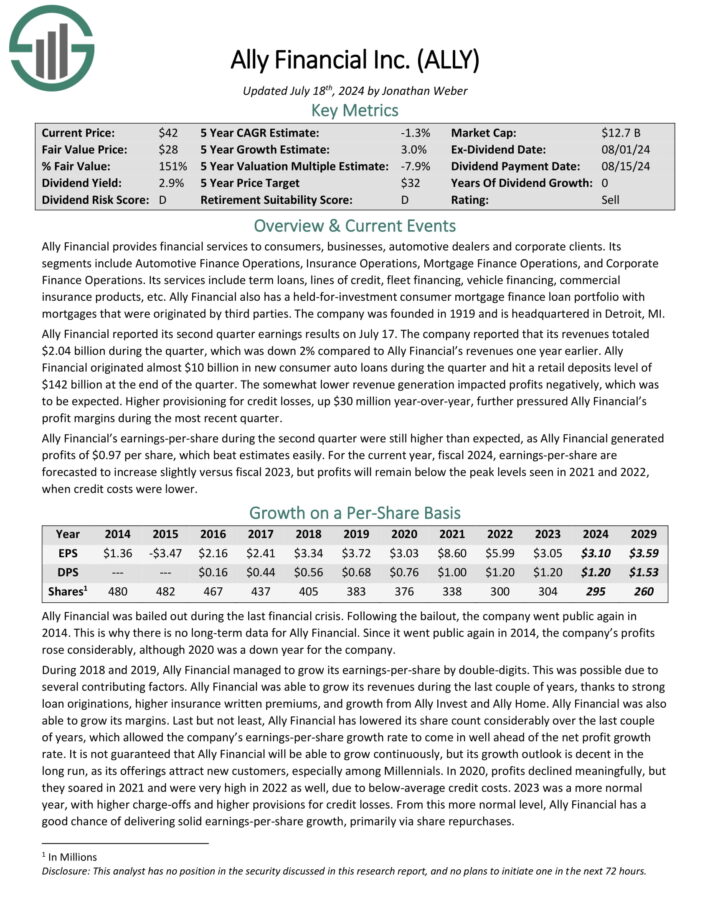

#5: Ally Financial (ALLY)

Dividend Yield: 3.0%

Ally Financial provides financial services to consumers, businesses, automotive dealers and corporate clients. Its segments include Automotive Finance Operations, Insurance Operations, Mortgage Finance Operations, and Corporate Finance Operations.

Its services include term loans, lines of credit, fleet financing, vehicle financing, commercial insurance products, etc. Ally Financial also has a held-for-investment consumer mortgage finance loan portfolio with mortgages that were originated by third parties. The company was founded in 1919 and is headquartered in Detroit, MI.

Ally Financial reported its second quarter earnings results on July 17. The company reported that its revenues totaled $2.04 billion during the quarter, which was down 2% compared to Ally Financial’s revenues one year earlier.

Ally Financial originated almost $10 billion in new consumer auto loans during the quarter and hit a retail deposits level of $142 billion at the end of the quarter. The somewhat lower revenue generation impacted profits negatively, which was to be expected. Higher provisioning for credit losses, up $30 million year-over-year, further pressured Ally Financial’s profit margins during the most recent quarter.

Ally Financial’s earnings-per-share during the second quarter were still higher than expected, as Ally Financial generated profits of $0.97 per share, which beat estimates easily. For the current year, fiscal 2024, earnings-per-share are forecasted to increase slightly versus fiscal 2023.

Click here to download our most recent Sure Analysis report on ALLY (preview of page 1 of 3 shown below):

#4: Diageo plc (DEO)

Dividend Yield: 3.8%

Diageo is a large alcoholic beverages company. It manufacturers popular spirits and beer brands, such as Johnnie Walker, Smirnoff, Captain Morgan, Baileys, Tanqueray, Guinness, Crown Royal, Ketel One, and many more. Diageo has 20 of the world’s top 100 spirits brands.

On August 5th, 2025, Diageo announced earnings results for fiscal year 2025 for the period ending June 30th, 2025. For the period, the company’s adjusted earnings-per-share totaled $4.23. Results were impacted by unfavorable currency exchange and restructuring costs.

Net sales decreased 0.1% to $20.2 billion, though organic sale growth was 1.7% as volume and pricing were both favorable for the fiscal year. Total market share grew or held steady in 65% of the portfolio, but this was down from 70% figure in fiscal year 2024.

The company had pulled its medium-term guidance due to the potential for tariffs to be placed on products, but Diageo expects organic sales growth to be in-line with FY 2025.

Organic operating profit growth is projected to be in the mid-single-digit range. The company is also expected to cut costs by $625 million over the next three years.

Click here to download our most recent Sure Analysis report on DEO (preview of page 1 of 3 shown below):

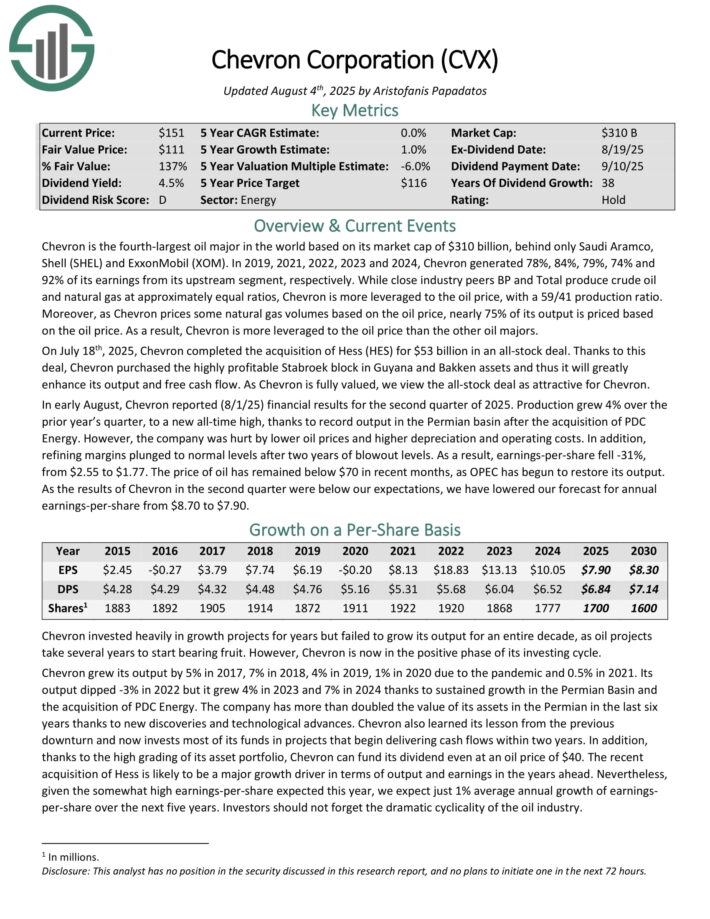

#3: Chevron Corporation (CVX)

Dividend Yield: 4.3%

Chevron is the fourth-largest oil major in the world based on market cap. Chevron prices some natural gas volumes based on the oil price, meaning nearly 75% of its output is priced based on the oil price. As a result, Chevron is more leveraged to the oil price than the other oil majors.

Chevron has increased its dividend for 38 consecutive years, placing it on the Dividend Aristocrats list.

In early August, Chevron reported (8/1/25) financial results for the second quarter of 2025. Production grew 4% over the prior year’s quarter, to a new all-time high, thanks to record output in the Permian basin after the acquisition of PDC Energy. However, the company was hurt by lower oil prices and higher depreciation and operating costs.

In addition, refining margins plunged to normal levels after two years of blowout levels. As a result, earnings-per-share fell -31%, from $2.55 to $1.77.

The price of oil has remained below $70 in recent months, as OPEC has begun to restore its output.

Chevron’s output dipped -3% in 2022 but it grew 4% in 2023 and 7% in 2024 thanks to sustained growth in the Permian Basin and the acquisition of PDC Energy. The company has more than doubled the value of its assets in the Permian in the last six years thanks to new discoveries and technological advances.

Click here to download our most recent Sure Analysis report on Chevron Corporation (CVX) (preview of page 1 of 3 shown below):

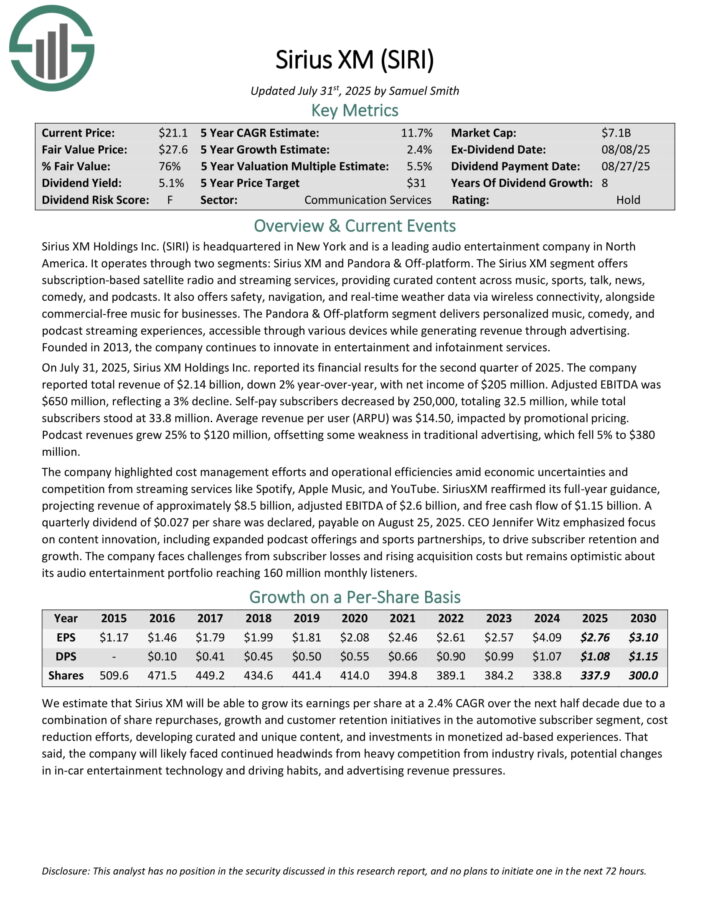

#2: Sirius XH Holdings (SIRI)

Dividend Yield: 4.7%

Sirius XM Holdings is a leading audio entertainment company in North America. It operates through two segments: Sirius XM and Pandora & Off-platform.

The Sirius XM segment offers subscription-based satellite radio and streaming services, providing curated content across music, sports, talk, news, comedy, and podcasts. It also offers safety, navigation, and real-time weather data via wireless connectivity, alongside commercial-free music for businesses.

The Pandora & Off-platform segment delivers personalized music, comedy, and podcast streaming experiences, accessible through various devices while generating revenue through advertising.

On July 31, 2025, Sirius XM Holdings Inc. reported its financial results for the second quarter of 2025. The company reported total revenue of $2.14 billion, down 2% year-over-year, with net income of $205 million. Adjusted EBITDA was $650 million, reflecting a 3% decline. Self-pay subscribers decreased by 250,000, totaling 32.5 million, while total subscribers stood at 33.8 million.

Average revenue per user (ARPU) was $14.50, impacted by promotional pricing. Podcast revenues grew 25% to $120 million, offsetting some weakness in traditional advertising, which fell 5% to $380 million.

SiriusXM reaffirmed its full-year guidance, projecting revenue of approximately $8.5 billion, adjusted EBITDA of $2.6 billion, and free cash flow of $1.15 billion.

Click here to download our most recent Sure Analysis report on SIRI (preview of page 1 of 3 shown below):

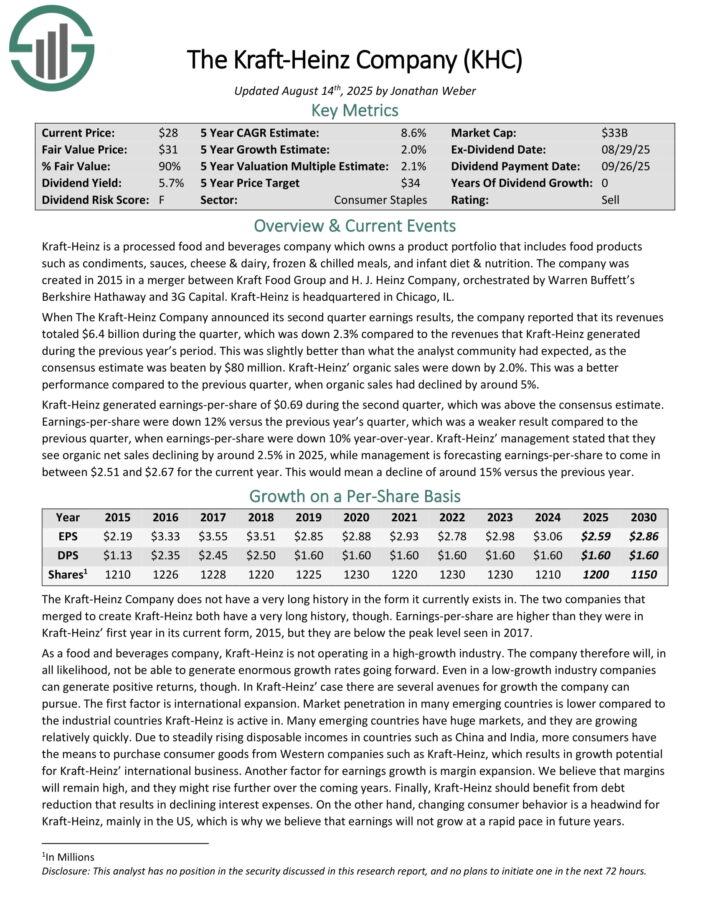

#1: The Kraft-Heinz Company (KHC)

Dividend Yield: 6.1%

Kraft-Heinz is a processed food and beverages company which owns a product portfolio that includes food products such as condiments, sauces, cheese & dairy, frozen & chilled meals, and infant diet & nutrition.

When The Kraft-Heinz Company announced its second quarter earnings results, the company reported that its revenues totaled $6.4 billion during the quarter, which was down 2.3% compared to the revenues that Kraft-Heinz generated during the previous year’s period.

This was slightly better than what the analyst community had expected, as the consensus estimate was beaten by $80 million. Kraft-Heinz’ organic sales were down by 2.0%. This was a better performance compared to the previous quarter, when organic sales had declined by around 5%.

Kraft-Heinz generated earnings-per-share of $0.69 during the second quarter, which was above the consensus estimate. Earnings-per-share were down 12% versus the previous year’s quarter, which was a weaker result compared to the previous quarter, when earnings-per-share were down 10% year-over-year.

Click here to download our most recent Sure Analysis report on KHC (preview of page 1 of 3 shown below):

More By This Author:

3 High Dividend Stocks Making Payouts Each Month

10 Top Retirement Income Stocks Now

Dividend Kings In Focus: MGE Energy

Comments

Log in or sign up to join the conversation.