Image Source: Pexels

One area of controversy that showed up after 2020 was about the role of “price gouging” in the overall rise in inflation. (This idea was satirically referred to as “greedflation.”) This has been an area of theoretical dispute between post-Keynesians and mainstream economists (as post-Keynesians argued in favour of a conflict theory of inflation), although it was not that a well-known dispute until after the pandemic. The obvious reason is that most people are not going to loudly argue about the sources of inflation when it was stuck near 2%.

Since I do not want this text to stray too far into theoretical disputes, I will just outline the ideas behind this debate.

Weber and Wasner Article

Isabella M. Weber and Evan Wasner published the article “Sellers’ Inflation, Profits and Conflict: Why can Large Firms Hike Prices in an Emergency?” in 2023. The authors argue that the conventional story that inflation is always macroeconomic is incorrect, rather it can have microeconomic origins.

The abstract of the paper summarises how they saw the inflation process developing in this instance.

We review the longstanding literature on price-setting in concentrated markets and survey earnings calls and compile firm-level data to derive a three-stage heuristic of the inflationary process: (1) Rising prices in systemically significant upstream sectors due to commodity market dynamics or bottlenecks create windfall profits and provide an impulse for further price hikes. (2) To protect profit margins from rising costs, downstream sectors propagate, or in cases of temporary monopolies due to bottlenecks, amplify price pressures. (3) Labor responds by trying to fend off real wage declines in the conflict stage.

This fits within the wider literature of “conflict inflation” that characterizes the post-Keynesian literature. The authors contrast this from a “macroeconomic” viewpoint, where inflation is the result of something like GDP growing above “potential GDP,” the unemployment rate being below the “The Non-Accelerating Inflation Rate of Unemployment” (NAIRU), or rapid “money” growth.

This does not correspond to “the inflation after the pandemic was the result of firms getting greedier than they were in 2019” (as some critics attempted to downplay the idea), rather it is a process that required concentration in “systemically significant upstream sectors.” There are always some firms raising prices to see whether they can pad profits, the issue is that there needs to be a mechanism for price hikes to propagate.

This idea fits in to the existing literature on “conflict inflation.” Conflict inflation is the standard post-Keynesian explanation for the inflation process. The mainstream view on conflict inflation is mixed. American neoclassical economists tend to reject the idea out of hand, while European mainstream economists were more sympathetic to the idea. The American stance tends to have a higher profile, presumably because they have stronger views on the topic.

Inflation Control Implications?

For reasons that I will discuss below, it is going to be hard to come up with conclusive analytical evidence either way on this topic if we look at outcomes under the current economic structures. The differences between the views show up more in terms of offering different policy options to combat inflation.

Given that I am not in the policy advocacy business, nor do I want to discuss unresolvable theoretical disputes in this text, I will not pursue this angle. However, the policy implications of the concept are why it matters. If one is only interested in forecasting inflation in the current policy environment, it is somewhat hard to distinguish between this concept and others.

Why I Like the Concept

I believe that the mechanism described in the Weber and Wasner article was a factor behind the inflation spike (although I will note theoretical concerns later). The authors give examples of firms taking advantage of the situation to push through price hikes, and how they fit in with the story.

The advantages of this story versus conventional theories is that we had an inflation spike at the right time.

- If one wants to blame “money printing” for inflation, why was there no inflation in Japan when they pioneered “Quantitative Easing,” or most of the major economies after 2008?

- If one wants to blame “fiscal deficits,” we then can make pretty much the same response as in the previous point.

- Trying to use the unemployment rate to explain inflation (e.g., the so-called “Non-accelerating inflation rate of unemployment (NAIRU)”) fails horribly. Inflation spiked when the unemployment rate was still quite high yet started to moderate even though the unemployment rate eventually hit low levels.

In summary, the supply chain disruptions were what distinguished the post-pandemic period from the rest of the post-1990 period, and that was the only period where inflation broke out. The supply chain disruptions were what gave “upstream firms” to ram through price hikes under this story.

Theoretical Concerns

At the time of writing, this line of argument is currently being debated, and I think the discussion will continue to shift. I have not seen an analysis that is truly conclusive one way or another.

The main difficulty is always going to be determining how much of the rise in inflation is due to rising profits. One method would be to try to estimate the effect company by company. The problem is that the ability to undertake such a survey is limited, and we need to question the reliability of things like statements on corporate earnings calls. Given that collusion to fix prices is illegal in some jurisdictions, corporate executives might shy away from stating that they did that publicly. Unless some form of survey was legally mandated to be submitted to national statistical agencies, it is going to be hard to connect anecdotal reports to the overall price index in a systematic fashion.

An alternative is that we could look at aggregate profits in the economy and attempt to assign contributions to overall price changes to the change in profits.

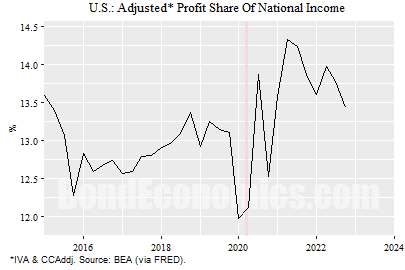

The previous figure shows “Corporate Profits with Inventory Valuation Adjustment (IVA) and Capital Consumption Adjustment (CCAdj)” as a percentage of national income from 2015-2022. There was an increase in the profit share after the disruptions in 2020, so one might try to argue that reflects companies padding profit margins.

The problem with this aggregate profit accounting story is the Kalecki/Levy Profit Equation. I discuss this equation in Section 4.2 of my book Recessions: Volume I. If we use a simplified version of the national accounts, the equation is:

Profits = (Net Investment) – (Household Savings) + (Dividend Payments) + (Government Fiscal Deficit) – (Net Imports).

(In the real world, the national accounts are more complicated, and there are more entries to the equation.) Importantly, this is not an opinion or theoretical model – it is an accounting identity. (An accounting identity is an equation that is true by definition – it just tells us how accounting entries add up when there are no errors in measuring the accounting entries.)

Although we could attempt to pin down the initial terms of the equation (net investment, housing savings, and dividends) by tying them to corporate pricing strategy within a model, the fiscal deficit and the trade deficit are determined by government policy and the state of the macroeconomy. Even if every firm in the economy wanted to raise its forecast profit margins, there is no guarantee that aggregate profits would rise.

An alternative way of viewing this concern is that one could create an economic model where prices and wages are constant. (For example, this describes many of the models I developed in my earlier book, An Introduction to SFC Models Using Python.) Even though profit margins on production are constant, profits in the model will still rise and fall due to other variables changing in the simulation.

Although the decomposition approach looks like the natural approach to test the theory, this is not necessarily the case. If the price hikes are being rammed through by “upstream” industries with pricing power, this results in downward pressure on the profits the “downstream” industries. Meanwhile, wages are also expected to rise.

If we move away from a “decomposition approach,” we face an additional concern: how much predictive value the concept has? It is one thing to have an explanation based on price hikes that have already happened and discussed in corporate earnings calls, it is another to have a forward-looking explanation that can be used to predict inflation. Why did we have no profit-driven inflation spikes from 1995-2020? Will we always need a disruption as large as the pandemic shutdown to have a repeat?

“Excuseflation”

We can then run into variant idea, which was dubbed “excuseflation,” which was discussed in a Bloomberg Odd Lots episode by Tracy Alloway and Joe Weisenthal ( URL in references.). Excuseflation is the observation that it is a lot easier for a firm to find an excuse to raise prices when other prices are rising. If a lot of other prices are rising markedly, it is a lot easier to sneak in price hikes that raise profit margins.

Although I think that is a good description of the psychology, we run into a theoretical problem. Saying that people are observing other prices shoot up is very hard to distinguish from those people forecasting higher inflation. This means that this is very hard to distinguish from the mainstream concept of “inflation expectations” – at least if we take a broad definition of “inflation expectations.”

Concluding Remarks

There was certainly a greater interest in the idea that price increases were the result of corporations trying to raise their profit margins after the pandemic disruptions. At the time of writing, it is still unclear whether it will shift how “mainstream” entities like central banks view inflation. My view is that it will be hard to find any data that can convincingly demonstrate an aggregate effect, although we certainly can find individual firms jacking up their prices and increasing their profitability.

The debate about the role of profit padding in inflation might result in a different perspective on how to control inflation, but that is outside the scope of this text.

References

-

Weber, Isabella M., and Evan Wasner. “Sellers’ inflation, profits and conflict: why can large firms hike prices in an emergency?.” Review of Keynesian Economics 11.2 (2023): 183-213. Working paper URL: https://scholarworks.umass.edu/econ_workingpaper/343/

-

“How ‘Excuseflation’ Is Keeping Prices – and Corporate Profits – High,” Bloomberg Odd Lots, Tracy Alloway and Joe Weisenthal. URL:https://www.bloomberg.com/news/articles/2023-03-09/how-excuseflation-is-keeping-prices-and-corporate-profits-high

-

The most introductory text discussing conflict inflation that I own is Macroeconomics by William Mitchell, L. Randall Wray, and Martin Watts.

More By This Author:

U.S. Breakeven Inflation Comments

Degrowth Versus Sustainability

Will The Fed Keep Reacting With A Lag To Lagging Data?

Comments

Log in or sign up to join the conversation.