Well, Russia just told Poland to settle up on their fuel bills in rubles or the plug will be pulled. I suspect this gets nasty (with the effect on forex markets being substantial) and also provides an excuse for invasion, like the U.S. used to do in Latin America in the days of so-called "gunboat diplomacy."

“B-b-b-but Russia can't invade Poland,” say the people who denied Russia would ever invade Ukraine, citing the fact that Poland is a NATO member. I am not terribly reassured by that cavalier expression of confidence. What bothers me about the Ukraine situation is how little history seems to be on the side of either the United States or the willingness of people to learn from history. In many ways what the United States is getting is a taste of its own medicine. 1962 was a pivotal year in JFK finding himself in the kind of public-opinion and other troubled waters that Biden finds himself in today. It was the United States that decided to put in place a series of cloak and dagger initiatives via the CIA to rid the world of Fidel Castro, and not just the kind of covert coup/assassination schemes as it was doing all around Latin America and as far away as Southeast Asia, but we went the full tilt level of landed invasion with Bay of Pigs. Nikita Khrushchev, seeing that disaster, sized Kennedy up as an inexperienced rich guy’s brat and put nuclear missiles in Cuba. By the time the worst of the crisis had passed, half the world had chewed its collective nails down to the elbow and the result was a very impactful trade embargo that altered the course of Latin American affairs and some say even started the American obesity problem with the end of Cuban cane sugar imports. Foggy Bottom orthodoxy invoked the Monroe Doctrine.

Once upon a time as undisputed ruler of the seas, the U.S. under presidents such as McKinley, Teddy Roosevelt and others had no problem at all being the collection agency for Robber Baron era industrialists and financiers who were being stiffed by sovereign clients south of the Tropic of Cancer. U.S. Naval forces simply sailed in and announced “pay up or else.” Yet we don’t see the similarities with Putin and Poland? We don’t see the similarities in the buildup of the EU and NATO filling into the slipstream of the ghosts of the old Warsaw Pact? We can’t see the similarities to how the Monroe Doctrine asserted that nobody but nobody had carte blanche in the Western hemisphere unless the U.S. president said so? Maybe one could say, “but that was more than a century ago.” Ask Mrs. Kirchner about that regarding seizure of Argentine naval vessels as investor restitution for violation of single class bond settlement covenants in New York statute, according to Judge Thomas P. Griesa.

So I am not surprised at all that Russia as I write this is stating that NATO supply lines are an issue and that Russia may strike them. News media handmaidens for NATO are dutifully bleating that this would result in immediate nuclear war. Funny thing…I don’t hear Mr. Putin disagreeing with that analysis.

There is much more I could say about the U.S. and Europe being in no position to preach to Russia about who is an aggressor and who is an innocent victim of aggression, and I would also add that the lack of transparency on what are both the American and Russian true motives in Ukraine is a very serious matter. Ukraine—all of the Baltic nations—are not known for being savory places when it comes to business dealings. We still do not know why Mr. Zelenskyy is worth the better part of a billion dollars owing to allegedly great success as an actor and a comedian, and nobody seems very curious about this. it is most illustrative in my view that there is voluble discussion over a billion-dollar weapons giveaway to Ukraine while the matter of having left $100 billion of the most cutting-edge weaponry available was left on the ground in Afghanistan not even a year ago and there is not a peep about where it went or any concern about retrieving it into what could be deemed trustworthy hands. The U.S. seems to have paid off the puppet ex-president of Afghanistan to the tune of billions to disappear and apparently he did and his unperturbed invisibility has been maintained. And Ukraine related policy initiatives are gaining speed like the proverbial rolling snowball with the current matter on the table being a demand for $2 billion a month in cash, weapons, supplies, etc. But seizing evil oligarchs’ yachts gets the attention?

Convergences and Divergences

Technical analysts like to underline the importance of divergences and convergences. In my somewhat radicalized approach to this philosophy, the reason for my screed above is that bad stuff like we see in the capital markets currently often goes hand in hand with bad stuff in the rest of life, such as contemporary events in Eastern Europe. And the Cuba comparison applies there too. Take a look at what happened to the stock market in 1962 that upended giddy times for the nifty fifty and go-go stocks. It was quite a mess, a mess that a glance at the Netflix chart reminds me of. And it eventually extended to a big hit on commercial real estate, thus revealing that some large institutions, including banks, brokerages and mutual funds, had a much bigger finger in the pie than had been presumed. As Netflix reminds me of the nifty fifty, so too, current inflation and interest rate dilemmas remind me of real estate “hot potatoes” of the past.

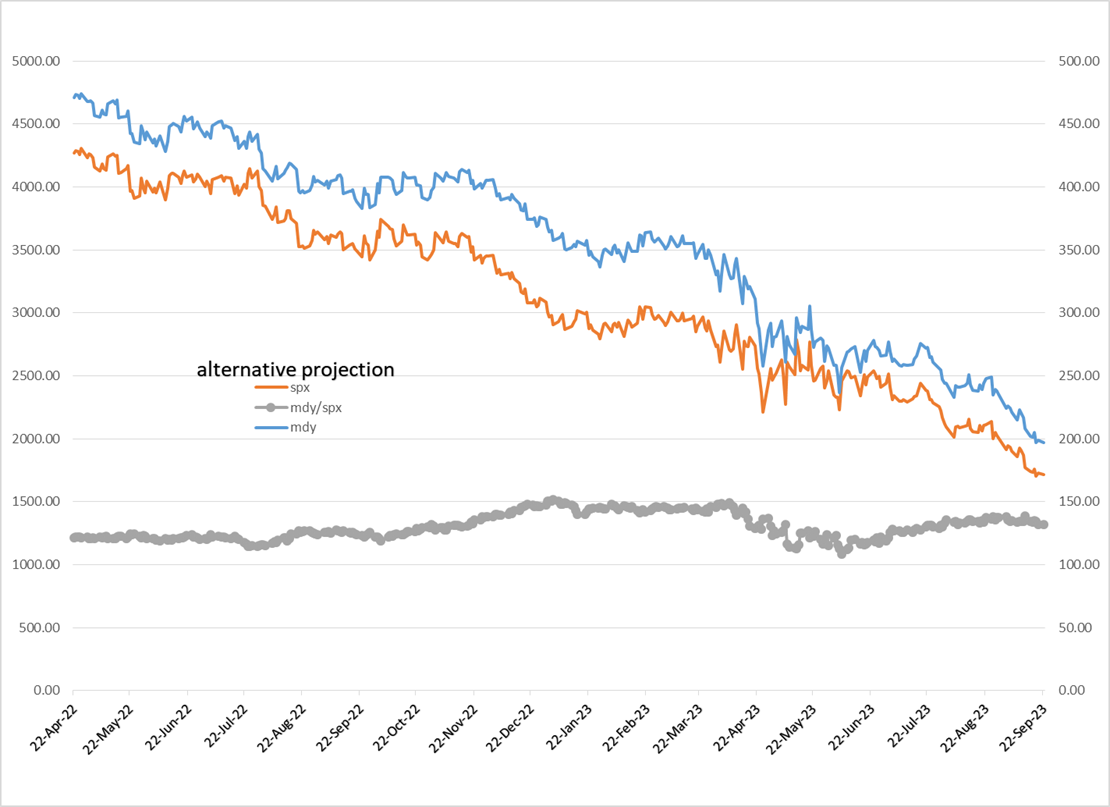

But my radicalized view of technical analysis doesn’t obviate my interest in more conventional views of convergences and divergences of various financial assets and instruments. One I find particularly intriguing—and I have felt this way for some time—is the correlation between the S&P 500 Index and its close relative, the MDY, which tracks the S&P 400 midcap class.

In the above chart, as the legend indicates, the midcaps are the blue line on the bottom and the S&P 500 is the orange line on the top. The grey line in the middle is another derivative of the RLH Volatility Model which is always based on long-term smoothed averages of volume-weighted daily fluctuations in price. What concerns me now about this relationship is that it has been deteriorating for more than a decade, and has been diminishing since mid-2016. This concerns me because it was only a minor attenuation in this model-measured relationship that led up to wholesale slaughter ahead of the dot com and mortgage derivative crashes of 2001 and 2008 respectively.

Extending the historical implications observed by the model to the current scenario, I have imputed two scenarios for where we will be heading through this year and well into 2023 as follows:

These are not savory projections. The main reason I used two differing methods of imputing the future with my model’s volatility criteria was to see whether results varied in either extent or duration. Considering the low probability of the very IDEA of this kind of imputed projection, the fact that the results for both approaches don’t differ a lot translates to “dealer’s choice” as I see it.

Further Aspects in the Comparison between the Current Times and the 1960s – 1970s

The main things I focus on as fundamental rather than technical elements in comparing 2022 with the 1960s and 1970s are financial market behavior, geopolitical issues (Cuba/Vietnam vs. Ukraine/NATO), inflation and real estate. As for thematic comparisons of these time-frames, the one that sticks out the most for me is complacency about one of these elements—complacency to the point of snide dismissal—and then not too long thereafter, expressions of “shock and awe” when the complacency and snideness is upended by reality.

During 1964 – 1965 John Chancellor was NBC’s “nightly news” face in counterpoint to CBS’s “grandfather of the news” Walter Cronkite. Chancellor had filled in the wake left by Chet Huntley and David Brinkley. Cronkite could never be topped ratings-wise but all his competitors did their best by trying to look as somber and serious as they could. One night Chancellor came on the air and with the gloomiest of faces ever seen in a newsroom announced that there was murmuring among economists that inflation was becoming a more worrisome factor than had been the case since the Korean War commodity inflation of the early 1950s, and the horrifying prospect was…wait for it!...the possibility of 4% compound annualized! I remember this broadcast and thinking, having just been introduced to the phrase, “no wonder they call economics the ‘dismal science.’ ” Nobody was going to knock Cronkite off his pedestal with this kind of report! But before long, inflation was in fact a big story, and as the war in Vietnam raged on, the “ABJ” movement took hold (“Anybody but [Lyndon] Johnson”), and in fact Johnson did announce he would not seek the Democrat renomination and Hubert Humphrey was put up in his place. Humphrey squared off against “comeback kid” Richard Nixon and Nixon, who ran as the “Peace with Honor” candidate bearing “a secret plan to end the war” very narrowly defeated Humphrey, whose main problem was being stuck with LBJ’s inflation and war baggage, including half a million troops in faraway rice paddies, soaring prices and widespread criticism of Johnson's arrogance for daring to execute a “guns and butter” policy. The auto industry was producing record vehicle unit output. The skies over the Ohio Valley from Cleveland to Pittsburgh to Buffalo to Detroit were red like the sunset three shifts a day with best ever steel production and employment numbers in skilled union jobs were high and producing impressive personal income stats. A Big Steel union job working in the vicinity of a blast furnace in those days got you better than $22 an hour with the right talents and sufficient seniority, and nice multiples of the hourly over 40 weekly hours, and double-time for some on holidays. Big Labor lived large then in cities now known for the absence of heavy industry. And in that section of the country at that time, thirty or forty grand could get you a nice sized three or four bedroom suburban house in a respectable subdivision with good schools backed by a 30-year mortgage in the range of 4.25% and a 20% downpayment. That was a monthly payment ranging from $200 - $400, and interest on the loan and the local property tax were both deductible against taxable earned income.

Mortgage Financing was a Very Different Kind of Beast in the 1960s and 1970s

Here is a pithy summary of the lay of the land for sources of funding for residential mortgage loans during the 1960s and 1970s, happily ripped off from a U.S. Treasury document titled, “The Federal Thrift Charter Is Created,” thus saving me the trouble of concocting this verbiage myself and also giving me the backstop of blaming a major U.S. government department in case any of it is erroneous. Thanks U.S. Treasury!

One aspect of reviewing financing legislation such as this is that money and lending has always involved government meddling by definition. And there is always a similar tone of “big bankers screwed us again so we had to pass laws cordoning off their territory.” What the above says about national banks being kept out of home lending sounds a lot like how Glass-Steagall kept the same people from being in investment banking and this and other legislation even required breaking up organizations involved in conflicting segments (e.g., the “trust busting” of the Teddy Roosevelt era that among other things peeled Morgan Stanley off of J.P. Morgan; ensuing similar developments for decades after that included similar disaggregation and reconstitution of the oil and the telecommunications industries).

The main reason I’m pointing this out now is to highlight the “who gets stuck holding the bag” aspect of real estate loans when inflation forces central bankers to take action by restricting availability and costs of funds. It is one of history’s most fascinating examples of Samuel Clemens’s adage that history may not repeat itself but it certainly rhymes. The reason this is true in real estate lending is a direct function of the law keeping big banks out and, because of that, who steps in to service the mortgage market. Then, after that segment builds up a massive portfolio of outstanding loans, what happens to those lenders when “guns and butter” incites inflation, central banks step in to raise rates, and loan portfolios decline in market value in order to make their issued rates competitive on a market yield basis in sync with credit markets in general.

The far-worse-than-Cliff Notes summary of what happened in the 1970s and 1980s consists of a few important moving parts. The thrift industry as the main lender for residential mortgages was issuing mortgages with depositors’ money (savings banks, savings and loans, etc.). The bond market was a pretty dull place before inflation became a noticeable menace, then things changed. The goal of central bank policy in those days was to tame inflation by disintermediating depositor funds from lenders and back to Treasurys. Policymakers assumed raising rates would accomplish this but thrifts struck back by creating money market instruments to compete with the government. Rates rose and rose and rose and disintermediation was not elicited. Real estate market values climbed with inflation and cost of financing did not overtake availability of financing, especially in markets like New York where insider discounts in the hot cooperative apartment market kept borrowing hot because buyers had dollar signs in their eyes and were willing to make higher monthly payments based on appreciation speculation. Multifamily speculators even accepted the idea of negative cash flow. But all wild parties eventually culminate in an empty punch bowl and when the prime rate finally hit 20.5%, inflation hit 10% and a proposal from Jimmy Carter to raise the capital gains tax to 50% hit the floor of the congress, the hats and hooters were gone, and lenders were sitting on loans with a market value pushed down by soaring rates and inflation they had built up for years with loans issued at less than half prevailing lending rates. This was a huge balance sheet hit that threatened the entire industry some of the failures were quite impactful and noteworthy such as Franklin National. The Franklin debacle, the Nixon resignation and a 50% meltdown from 1973 stock market peaks all occurred in 1974. A year later New York City went bankrupt. In 1976 Jimmy Carter defeated Nixon’s successor Gerry Ford. Ronald Reagan defeated Carter in 1980 who assumed office in 1981. By August of 1982 the stock market was more or less at the same peak levels it had attained in 1973. The picture was not rosy.

New Bagholders

By 1984 Alan Greenspan was well on the way to all new (actually resuscitation of the old pre-Paul Volcker) policy of targeting fed funds rather than money supply which was what “bad guy punchbowl remover" Paul Volcker had to do in order to tame inflation. Greenspan bet on the idea that the emerging technology industry would allow him to flood the system with money following Volcker’s money supply tightening regime by contributing massive productivity gains that would stave off inflation, further insured by lingering recessionary drags. This held true right through to the end of the millennium, albeit with some significant hiccups in the “Asian Contagion” and the failure of Long Term Capital Management (a hedge fund up to its ears in arcane hedges feature gold against rubles), and it all ended with massive speculation in the dot come sector as Prince partied like it was 1999, speculation ran rampant and earnings from companies such as AOL, Netscape and others fell way short or never materialized despite large expectations for same as well as enormous acquisition activity. As all this was going on, a large transition was underway in sources of funds for real estate financing.

By the time of the 2008 mortgage meltdown the role of the thrift industry, already post-massive consolidation, was but a shell of its former self, as was the entire idea of depositor-based lending. Not only were the new lenders typified by what we know as Rocket Mortgage and their ilk today getting their funds from relatives of what earlier legislation had tried to keep out of the picture, but Glass-Steagall had also been eliminated, and that was the basis for the construction of derivatives in the bond market, including bundled mortgage packages constructed to get around rating-agency particulars regarding risk. Accumulation of massive U.S. federal debt due to 9-11, the wars in Iraq and Afghanistan, security initiatives such as Homeland Security and increases in government intervention into healthcare exacerbated matters.

So now we are at an important crossroads where history is rhyming but not repeating, and “guns and butter” are rearing their ugly heads once more. Inflation is the culprit again, and there is far more pernicious aspects to the discussion than ever previously, essentially trying to blame exogenous difficulties for what are in truth domestic policy flaws both fiscally and monetarily.

But the really big new factor is size of debt in U.S. on-the-books obligations at $30 trillion and prevailing rates determining interest obligations’ being only a third or a quarter of the annual inflation rate that is merely the initial dimension of what is taking shape as the enemy rate to overcome. Discussion of this so-called “neutral” rate is as wicked as the blame game for how this inflation came about but the Fed is being forced to play chicken with prices and in my estimation there is no possibility of the U.S. government spending debt-service outlay, which is already comparable to defense outlays, being three or four times the present level. Also, back when the housing industry was targeted by central bank policy to bring inflation under control, the thinking was that you could “draft inflation fighters working construction” by putting them out of work, and that their high incomes and spending would be missed by the butchers, bakers and candlestick makers, reduce spending and bring down prices.

I don’t think that works now because of what it would do to federal interest outlays. What does that leave? Either getting used to the idea of a stock market crash as inevitable, or expressly creating one. In my view that’s the obvious choice because, as the once notorious Willie Sutton responded when asked why he was knocking over all the banks he could, “that’s where the money is.” So a crash is, by this analysis, either the only inevitability, or the express choice. How will we know what’s coming? I would be on the lookout for clues like Biden doing what LBJ did (not seeking renomination) and greater emphasis on initiatives like student loan forgiveness and other handouts especially as times get tougher, in effect finessing a political scheme that would “reimage” Biden as the new Herbert Hoover and position his anointed successor as the new FDR, even though both would be democrats, all engineered by a party trying to get ahead of a game they can’t change. Just a theory, of course.

Whatever happens should be quite engaging, and anything but boring.

Comments

Log in or sign up to join the conversation.