Image source: Pexels, Photo by Monstera

In its latest 13F filing (as of June 30, 2025), Berkshire Hathaway, under Warren Buffett, boosted its position in Pool Corporation (POOL) and Domino’s Pizza (DPZ), with the latter being one of my favorite companies in the world, although I don’t eat their food.

Pool Corp. is fascinating, too. It’s a niche yet dominant distributor in the pool maintenance space. It fits the sort of capital-efficient, high-moat business within Buffett's playbook. He wants strong recurring demand, pricing power, and durable cash flows.

This move reminds us that Berkshire Hathaway wasn't just built on stock-picking genius. Berkshire Hathaway has always been a structural masterpiece. Buffett created the ultimate permanent capital vehicle. It’s funded by low-cost insurance float and leveraged at roughly 1.6x, according to AQR research. Then his entire machine was turbocharged by tax deferral, a topic he’d regularly discuss in his shareholder letters and showcase in the financials.

Buffett hasn’t needed to chase alpha. Instead, he controlled time, liquidity, and compounding mechanics. Every dollar would be recycled into long-duration, high-cash-flow assets.

The goal was never to maximize growth, but to maximize efficiency, control, and durability.

New Players, Same Game

Today, a lateral version of Buffett's original model is emerging. The thing is, it's not happening in Omaha. It's unfolding in Riyadh, Abu Dhabi, Singapore, and Oslo.

Sovereign wealth funds have adopted a different version of Buffett's playbook. They utilize permanent capital with little redemption risk and focus on long duration.

But they're applying this capital to different kinds of assets. They’re buying up the physical and digital infrastructure of the modern economy.

While Berkshire reinvests in railroads and pipelines, sovereign funds are acquiring and building server racks, AI data centers, LNG terminals, grid access, power rights, and toll infrastructure. They're not betting on capital appreciation. They're buying rent.

They're acquiring long-duration, cash-flow-producing assets with contractual income, leasing the future through multi-decade agreements -- all with higher yields and stronger alignment between capital and time.

Saudi Arabia's PIF is investing billions into U.S. data centers through DataVolt. Aramco is building stakes in U.S. LNG infrastructure. Capital from Singapore's GIC, Norway's sovereign fund, and Qatar's QIA is diving into fiber, digital storage, and power grids.

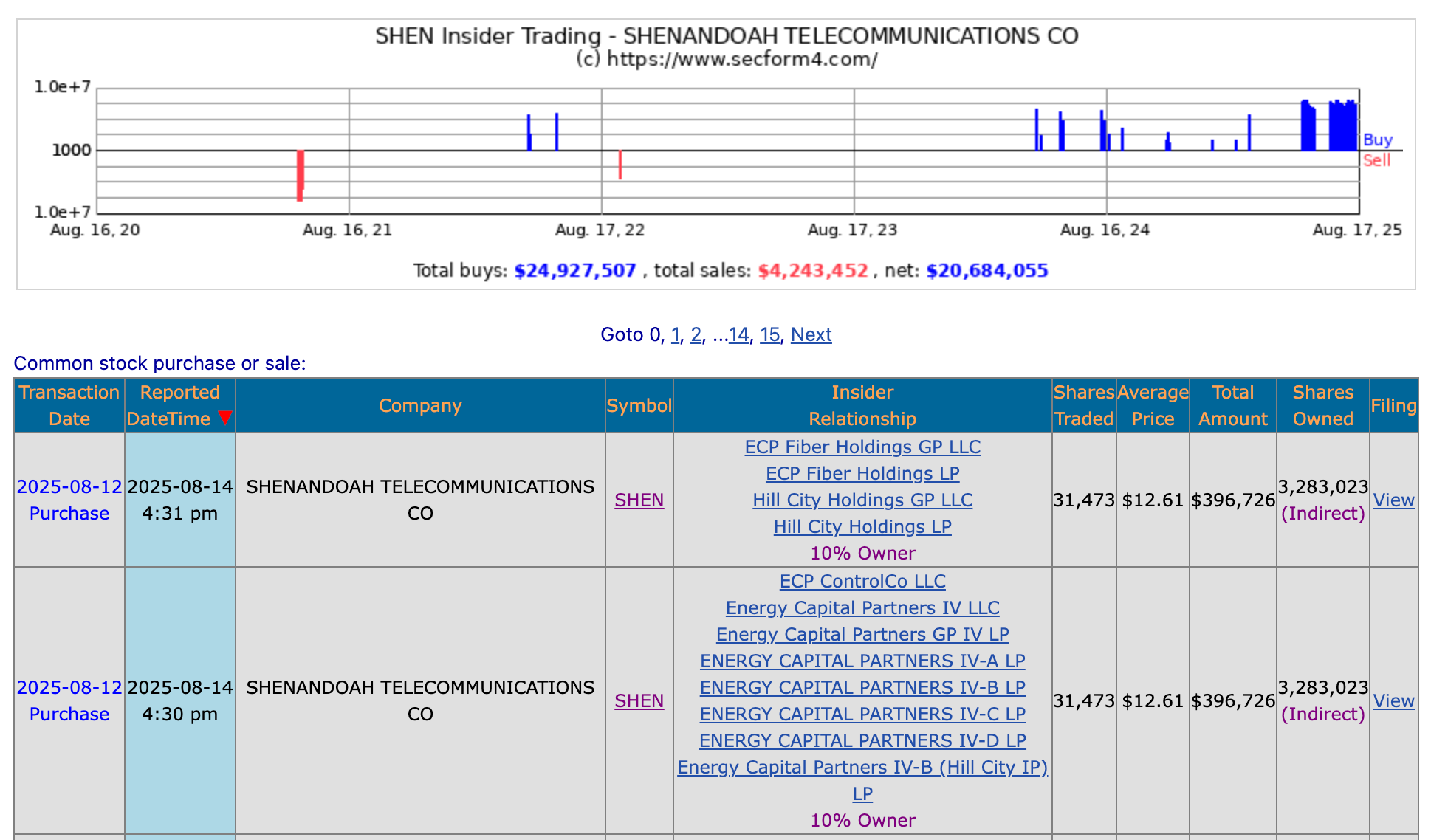

Also, if you’re looking for a stealth play on the fiber, see Shenadoah (SHEN) as an insider darling. It’s not big. It only boasts $686 million in market capitalization, but insider money is seemingly flooding into it through the back door. Kudos to Scott Dunn, who works with me, for picking up on this.

(Click on image to enlarge)

I’m just saying, this is the type of thing that I’m often looking for; dollar-denominated, capital-efficient, tax-advantaged, and increasingly vital to the functioning of the American economy. Let’s find more of them.

The Infrastructure of Compounding

The evolution beyond Berkshire isn't just about owning great companies. It's about owning capital-efficient assets with permanent capital, structured to generate income with minimal reinvestment, long-term contractual durability, and insulation from equity market cycles.

This last point matters a lot. Even the best companies get crushed during liquidity events -- years like 2008, 2011, 2015, 2018, 2022, and 2025. The boom-and-bust cycles driven by global liquidity flows, credit creation, and liquidity crises hammer even the best businesses.

But infrastructure assets with contractual cash flows can provide a different kind of durability.

The New Permanent Portfolio

Buffett never lost his touch as a stock picker. The problem -- and why Buffett likely struggled against the market in recent years -- is that he moved away from what made it great in the first place (and the fact that we keep dropping money from the sky while he’s still focused on fundamentals).

They stopped deploying float into world-class names like Amex, Coke, and Apple. Instead, they had redirected capital into capital-intensive, wholly owned businesses like BHE, Kraft Heinz, and Precision Castparts.

This, initially, made sense from a tax efficiency standpoint. But it’s weighed down their capital allocation and overall return profile. This recent 13F went back to basics with Domino’s, Pool, etc. But I think long-term investors have to worry less about Buffett’s 13Fs, and should instead turn their attention to a sovereign-style allocation.

The focus should be on assets that share key characteristics. They need to be capital-light post build-out, generate contractual dollar-denominated cash flows, resist or even benefit from inflation, and be backed by sovereign or institutional demand.

Let's look at some places to start your research.

Digital Infrastructure & Storage

Consider names like Digital Realty (DLR), Iron Mountain (IRM), and American Tower (AMT). They all represent the "rack-rent" infrastructure of the digital economy, with built-in inflation protection and growing interest from sovereign funds.

Energy Royalties & Pipelines

Then, turn your attention to Viper Energy (VNOM) and Williams Companies (WMB).

These names offer yield with minimal reinvestment -- cash flow per barrel, cubic foot, or export volume. These do require maintenance, but I trust the business model.

Streaming & Royalty Models

Next, look to Franco-Nevada (FNV), Wheaton Precious Metals (WPM), and Black Stone Minerals (BSM). These are structured to buy cash flow, not operate assets. They’re, in my opinion, the purest expression of the Buffett-adjacent model applied to commodities.

Infrastructure REITs & Yield Platforms

Next, look at Brookfield Infrastructure Partners (BIPC) and Clearway Energy (CWEN). They offer core infrastructure exposure with varying degrees of capital intensity.

Logistics & Storage Assets

And, of course, names like Prologis (PLD), Safehold (SAFE), and Americold (COLD). These control essential nodes in the physical economy.

Private Credit & Specialty Finance

Finally, I like the private credit side as always, with a focus on KKR Real Estate Finance (KREF) and Ares Capital (ARCC), which the Federal Reserve will always back in our financialized economy. These are the real buy-the-dip names when the money printer runs.

Sovereign Wealth, Sovereign Man

This approach isn't about beating the market every year. And, it’s not “original.”

Companies like Brookfield deploy a similar strategy. This is just more of a hybrid. But the entire concept is about owning durable, yield-rich assets that compound over decades, largely independent of sentiment. These assets help avoid the worst parts of liquidity cycles while owning critical infrastructure that will always have the backing of the Fed and the dollar.

The continued financialization of the economy will lead to further compounding. And any serious problem in these sovereign-side assets will trigger bailouts -- that's baked into the system.

This is the reimagined next-generation float machine. Not a hedge fund, not a venture book, but a pure institutional-grade yield engine engineered for compounding. A synthetic sovereign wealth allocation for the individual investor.

The next edge isn't in chasing the next great company. It's in owning the infrastructure of compounding itself. While Buffett built his empire on insurance float and American businesses, the new permanent capital is being deployed into the rails and rent of the digital age -- and that matters because individual investors can participate in this transformation.

In the wake of Berkshire's latest moves, perhaps the question isn't what Buffett is buying, but what the next generation of permanent capital allocators is building.

I think that answer is the blueprint for the next fifty years of wealth creation and the return of the 'Political Economy' and 18th-century thinking on the role of a nation in building and sustaining wealth. So, please do me a favor: go get the bag, investors.

More By This Author:

The Insiders Aren't BuyingRough Seas

Central Banks Just Showed Their Hand

Comments

Log in or sign up to join the conversation.