Starting with a special video on Monday morning and our Daily Market Commentaries throughout the week, we continually updated readers on the excessive volatility in the markets. We wanted to stress that the volatility was primarily a function of the yen carry trade and much less other daunting issues such as the recent unemployment report, Israel vs. Iran, the coming elections, and the Fed. Our advice was simple yet very difficult for many to follow: have patience. Regarding patience, in the video, we urged readers to “sit on your hands” and resist the temptation to let their emotions get the best of them. Moreover, assessing your portfolio when calmer seas prevail will likely prove beneficial. Midweek, after better understanding the situation, we advised: “Be patient for now, and use the current rally to reduce risk and rebalance portfolios as needed.”

There were many clues that volatility was due to the unwinding of yen carry trades. While it made us anxious, we anticipated it would have a limited life. For instance, Wednesday’s Commentary said: “For now, the carry trade victims appear limited. We presume the Bank of Japan and the Fed have been on the phone constantly and will intervene in the currency markets before the problem spreads to a broader array of assets.“

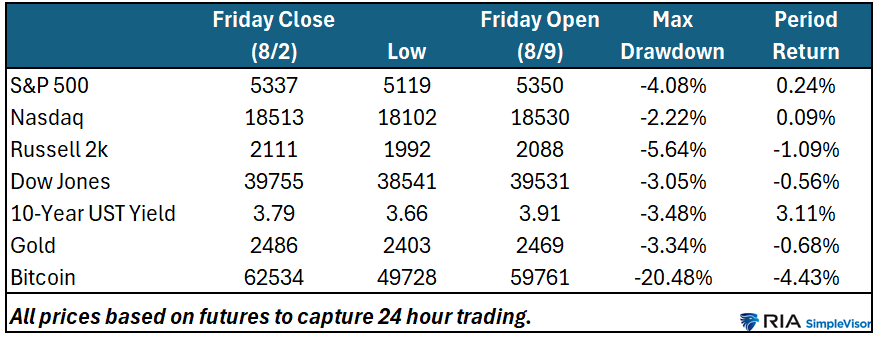

So, with the storm showing signs of abating, at least for now, was patience a virtue? The following table says patience paid off. Most markets are nearly flat since last Friday’s close. Now, with a better handle on the situation and your emotions in check, we advise adjusting your portfolio as desired.

What To Watch Today

Earnings

Economy

- No economic reports of note

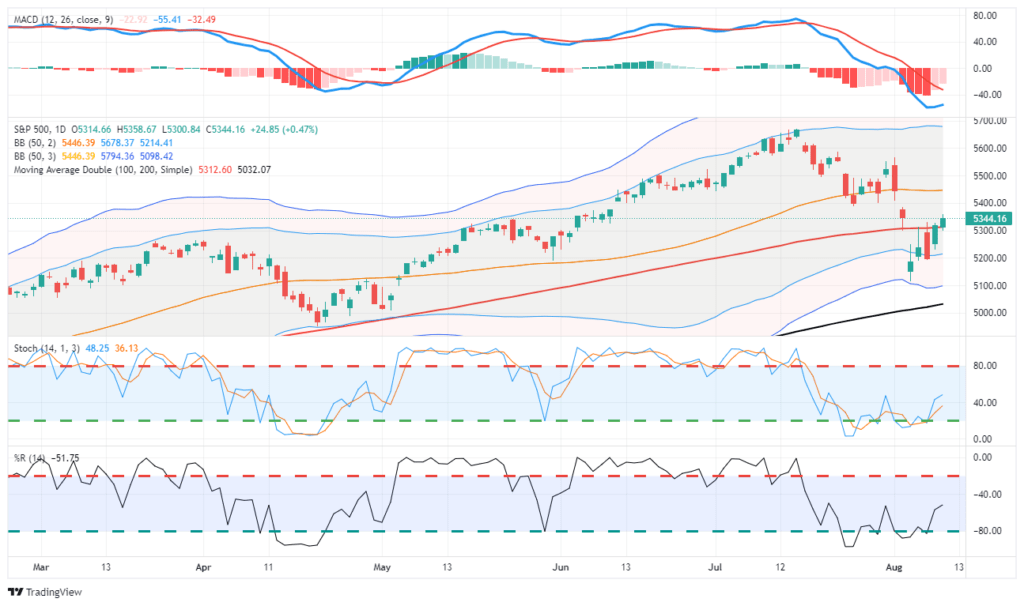

Market Trading Update

Last week, the market declined due to a sharp spike in volatility caused by the ” blowup” of the “Yen carry trade.” As discussed on Friday, the reflexive rally was unsurprising after the recent decline, and the 100-DMA posed an initial challenge. With the markets decently oversold, which exhausted sellers short-term, continuing the rally this week would be unsurprising. However, as shown, significant resistance levels are ahead, which keeps us somewhat cautious. The 20- and 50-DMA crossover and the previous gap will challenge the bulls in the short term.

As such, use the current rally to rebalance risk and reduce exposure as needed in portfolios. This initial rally from Monday’s low will likely fail, and the market will retest the recent low at least once before this correction process is complete.

The Week Ahead

Investors will focus on economic data this week. Presuming CPI, released on Wednesday, and PPI, released on Tuesday, are tame, the Fed will likely proceed with a rate cut at their next meeting. CPI is forecasted to rise 0.2% after falling by 0.1% last month. The year-over-year core CPI is expected to be unchanged at 3.3%.

Retail sales data on Thursday is expected to show slight growth. While the number is important, it will not show how recent market volatility affects consumer sentiment. Friday’s University of Michigan consumer survey will likely be the first data point on consumer confidence after last week’s market action.

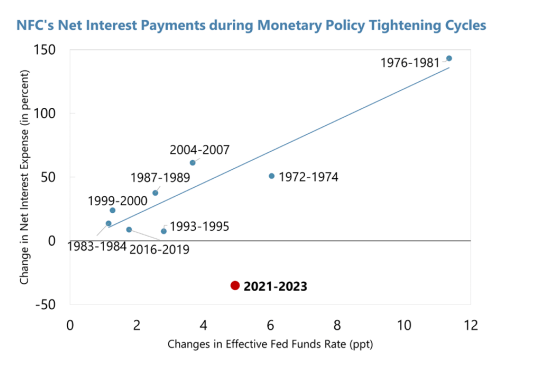

Why High Fed Funds Have Not Been As Damaging As Normal

The IMF graph below shows that corporate interest payments typically rise when the Fed raises the Fed Funds rate. That should not be surprising. The Fed’s goal in raising rates is to slow economic growth and increase corporate expenses, leading to other cost-cutting measures that help constrain economic growth.

This time, however, it didn’t work, as shown by the red dot in the IMF graph. When rates were historically low in 2020 and 2021, corporations pre-funded their debt needs. They created excess cash on their balance sheet by getting ahead of their needs. Having borrowed at low rates, they could then invest the cash at high rates after the Fed raised rates. In many situations, this windfall helped lower net interest payments. While this was a tailwind for growth, it will soon end as rates come down. Furthermore, some of the debt issued at low rates will mature and need to be refunded at higher rates.

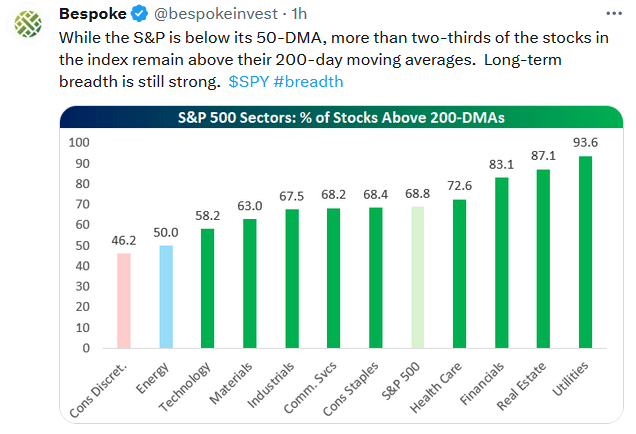

Tweet of the Day

More By This Author:

The Market Crash Heard Around The WorldLabor Hoarding: The Labor Market Lynchpin

The Bank Of Japan Calms Markets

Comments

Log in or sign up to join the conversation.