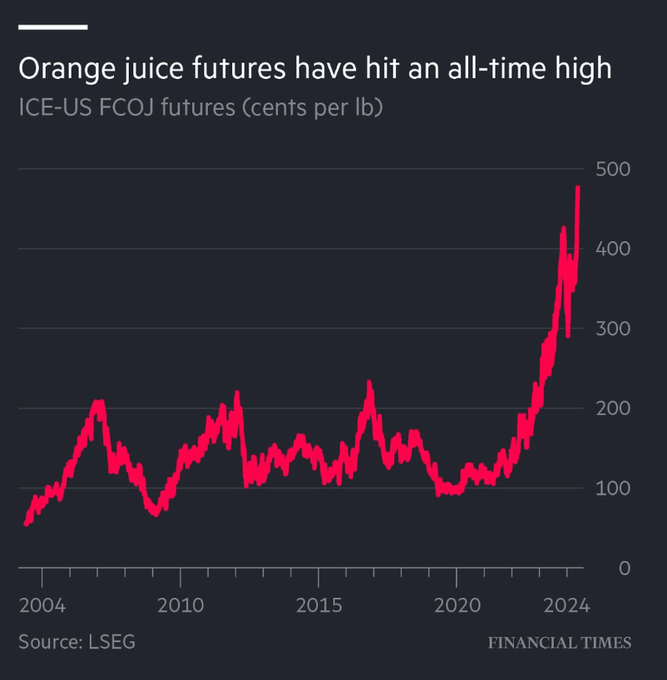

In mid-March, we presented daily Commentary readers with a section entitled, Add Cocoa To The List Of “Mooning” Assets. When we wrote the article, the price of cocoa was up by 70% for the year, in line with year-to-date gains in Bitcoin and Nvidia. Since then, cocoa prices have fallen by over 40% but have started rising again. Some of the price volatility is undoubtedly due to weather conditions and its impact on the cocoa harvest. But as we wrote, speculative fever also plays a role. Orange juice futures appear to be following a similar path.

The graph below shows that orange juice futures prices are “mooning.” Citrus greening, a disease affecting Brazil’s trees, is impacting the price of orange juice. Furthermore, draught and above-average temperatures in Brazil also weigh on crop yields. As a result, Brazil’s crop is expected to be 25% less than in average years. Further impacting the supply of orange juice, Florida’s recent hurricanes have damaged orange trees. The outlook for a busy hurricane season is also to blame.

However, similar to our thoughts on cocoa in March, it seems that orange juice prices are also swayed by the more mainstream speculative flows impacting the commodity markets. Commodities have always been a speculative arena, but with more traditional investors trading orange juice and other commodities, the correlation between crypto and hot stocks is rising as well.

What To Watch Today

Earnings

- No notable earnings releases.

Economy

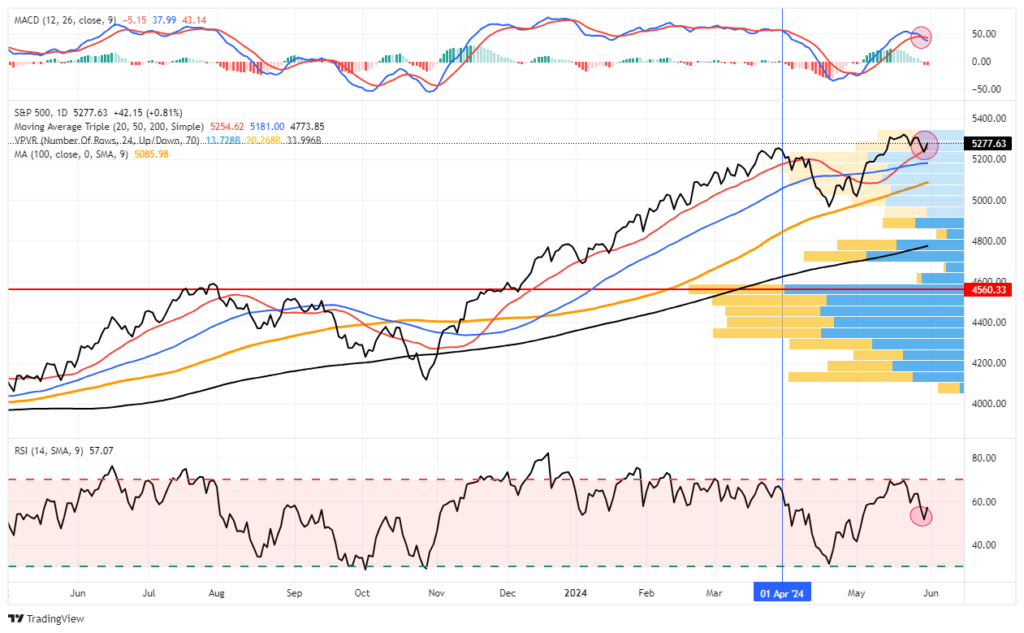

Market Trading Update

Last week, we discussed that consumer data suggested the economy was weakening. That was confirmed this past week with downward revisions to Q1 GDP and weak personal consumption expenditures (PCE) reports.

The U.S. economy’s growth in the first quarter was revised to an annualized rate of 1.3% from the previously estimated 1.6%, reflecting weaker consumer spending and equipment investment. This slowdown contrasts sharply with the 3.4% growth rate in the final quarter 2023. Inflation for the first quarter was also slightly revised down to 3.3%.

On Friday, PCE, which is roughly 70% of GDP growth, also came in under expectations, adding more concerns to a growing list of economic data that has recently weakened.

In an interesting turn of events, “bad news” seemed to matter to the markets this week. Of course, the reality was that the market was overbought and needed a correction. Wall Street just needed a reason to liquidate some positions.

As noted last week, the 20-DMA crossed above the 50-DMA. On Friday, that support level held, with the market bouncing off of it, keeping the current consolidation in process. If the 20-DMA fails, the 50-DMA is the next logical support level. Below that will be the 100-DMA held during the April sell-off.

Crucially, the market has now registered a “sell signal,” which will limit any rallies in the near term. Therefore, use bounces to reduce exposure and rebalance portfolios as needed. The upside to the market is likely constrained to recent highs.

The Week Ahead

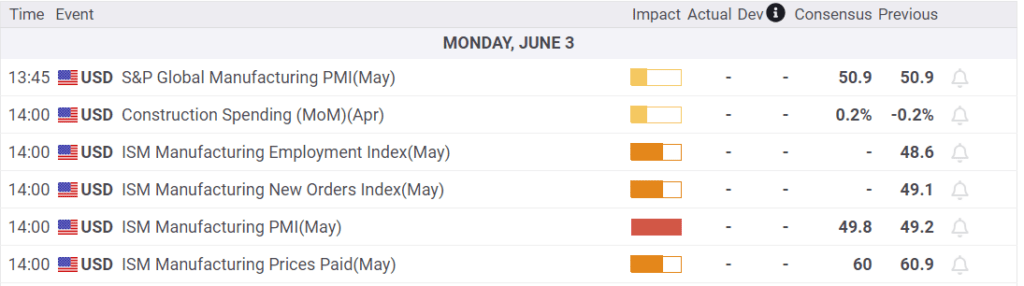

A new monthly cycle of economic data starts this week with the latest jobs data. JOLTs on Tuesday, ADP on Wednesday, and the BLS report on Friday will provide a new round of employment data. The market expects another relatively weak job number, with payrolls rising by 177k. The prior reading was 175k. We say “relatively” because payroll growth averaged approximately 250k a month. Also on the calendar are the ISM manufacturing and service sector reports on Monday and Wednesday, respectively. The jobs and prices sub-components will likely garner the headlines.

We get a reprieve from Fed speakers as they enter the media blackout period before the FOMC meeting on June 12th.

Electricity Demands And Debt

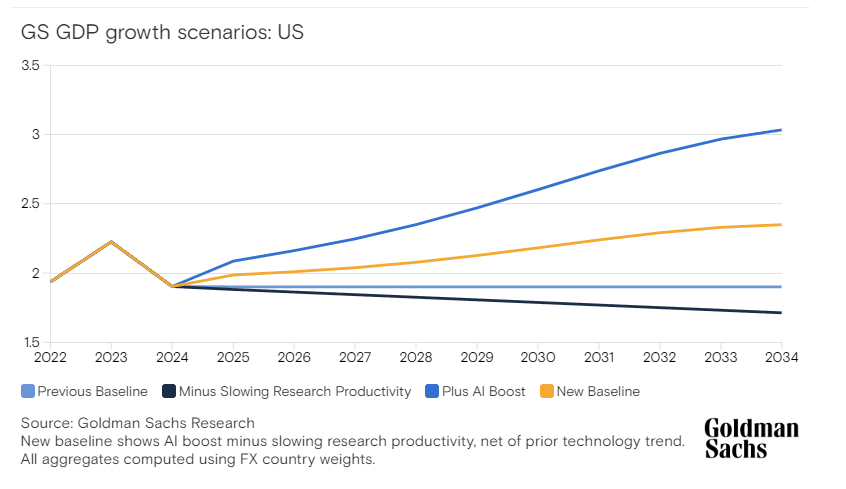

Traditionally, government debt has a negative multiplier. In other words, each dollar of debt ultimately reduces economic growth. While we have little doubt that will change going forward, there is one significant investment the government will be making that has the potential to create lasting economic growth. Following up on our soon-to-be three-part article (Link 1, Link 2) on investing in the coming power grid expansion, we present an article on how the massive upgrade and expansion of the power grid will affect the economy. The following comes from Electricity Demand Cures Debt Concerns.

However, building infrastructure is very labor-intensive, and CapEx is labor—and investment-intensive. Those dynamics change the economic growth dynamic. While corporations increase capital investment to build the power supply, the Government will likely enter the fray with further infrastructure-focused spending bills. This is because AI is a critical component of ensuring the defense and national security of the United States. However, instead of issuing debt to spend on domestic welfare programs, the debt used in infrastructure will create economic growth through labor creation.

Government spending on infrastructure differs from most other government spending because it can create both near-term economic growth in the grid’s buildout and, more importantly, lasting economic growth.

The article shares that Goldman Sachs thinks the infrastructure expansion could add 0.4% to GDP, as shown below.

Increases in productivity, productive capital investment, and increased labor demand for the infrastructure buildout (which will also result in higher wages) should provide the economic boost needed.

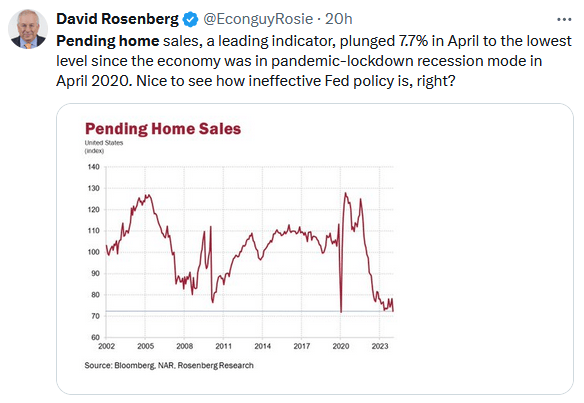

Tweet of the Day

More By This Author:

The MoMo Chase RemainsLets Knock On Wood

Electricity Demand May Cure Debt Concerns

Comments

Log in or sign up to join the conversation.