Market Briefing For Tuesday, August 18

The 'tone' of this market wasn't changed much by the weekend news. S&P again shrugged off the 'excess liquidity' issue, the uber-optimistic Goldman Sachs (GS) upgrade on-top of a nearly-half-year run-up we've assessed as continuing with only hiccups, and despite some very bearish 'assumptions' about Warren Buffet's 'gold play' which I suspect might have ended before the report of the filing (hence could be selling into a bit of buying created by the after-the-fact report of 2nd Quarter activity).

(Typo: not 'but but'; meant 'but not' broad.)

Executive Summary:

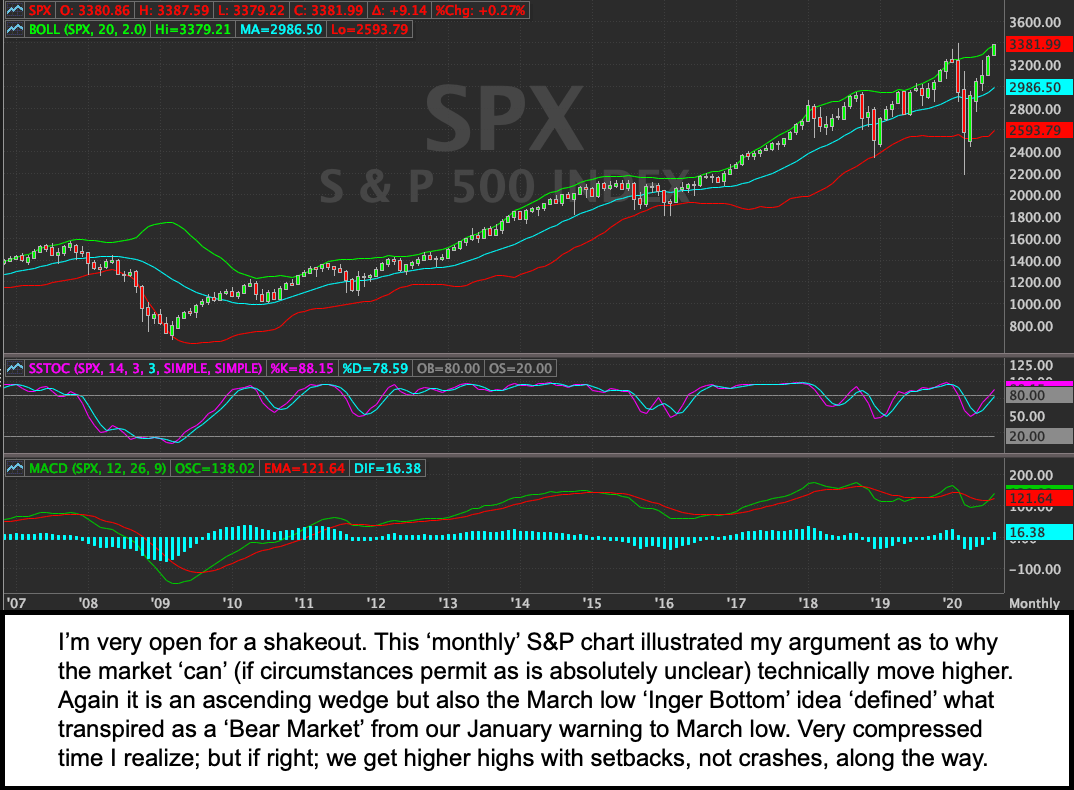

- Ascending wedge patterns, most notable in the NDX, are technically noted in tonight's briefing.

- Behavior of most stocks was favorable and held well despite some effort to retreat from out-of-the-box rallies based on Goldman Sachs upgrade we noted in the weekend report (and belatedly joins our own ascending wedge viewpoint).

- Circumstances go well beyond 'Covid' with respect to the market, assumptions that a Biden/Harris ticket means centrist policies is what the market wants to see for now, whether that's truly their perspective or not;

- The first night of Democratic Convention begins with anti-Trump Republicans.

- College and other school 'live-class' suspensions increase and are highlighted by the Univ. of North Carolina decision today.

- I urged educators to review the Danish approach of small circles and limited total groups (even without masks) as intelligently discussed this weekend.

- Market should close at a new S&P high (NDX leading of course), but caution that some of the super-caps are moving beyond even bubblelicious valuations, that doesn't mean it breaks immediately, but caution should be employed.

The Covid 'crash' was not just a pothole

None of this is to suggest we aren't going to have another shakeout within a trend, a sort of environment where people assume the economy can't catch-up with markets. I have a different view, that while Covid helped complete our early year 'Bear Market' (projected starting in January and elevated to 'crash alert' in early February), this big advance in the S&P (more so than the broad market) is possibly the important first phase not only off the 'Inger Bottom' as I termed it aspirationally on March 23, right as 'max-fear' gripped the Street, but the first leg in what could be a major trend.

Now, for that to occur (major trend), there are political aspects that can't be known as of yet, and we don't at all deny that certain developments could lead to not merely a higher tax environment, but even Depression-like conditions on a broader front than experienced so far.

History shows us that the technical picture we see for the S&P is not necessarily so bearish as simply an extended market, but can be a component of a coordinated or even global) cyclical economic recovery, which would be the precursor to the roaring 20's of this century; not entirely unlike the last century's.

Bears would dismiss all this by suggesting our forecast February-March break wasn't a big deal, but was just a pothole in the old uptrend at least since December of 2018 (another low we nailed going into Christmas Eve that year). Ah ha.. so that is exactly where they miss an alternative prospect, which is that -while compressed into a very short window- the pandemic-panic-fueled March collapse was an actual defined bear market, so you have to dismiss the 'pothole idea' (unless looking for pot) to visualize a technical pattern quite different from the common bearish outlook.

Those bears are not looking at this like the ascending wedge we have identified (very evident particularly in the NDX), which is absolutely liable to experience a shakeout. I have said this for some time because that pattern doesn't require catastrophe. And if you get a sufficient broadening-out of market participation (economic revival), then it becomes less dependent on the heavy-lifting super-cap stocks, and becomes greatly relieving to investors in many sectors. But getting to that nirvana isn't an easy task.

How so? Because of Covid-19. Even now there is reticence at 'funding' industries we will need for recovery to blossom (airlines included and likely to get help if for a poor reason, being that politicians will be at-risk with voters if their districts lose all service) and there is the absence of a true home saliva test combined with an App for phones (Chinese-like) that might provide less 'personally identifiable' information to the CDC or appropriate tracking groups (like John Hopkins who keeps the tallies), but enough to track where outbreaks or contractions is cases, positivity and so on are occurring.

Personally I suspect this is the holdup with something like Sorrento's (SRNE) / Columbia test, as I'm thinking the recent Trademark filing of 'Covi-Mobile' is intended to fill that void. I suspect CDC does not want unknown testing to go on, and 'tracking the testing' is a reason to have an App that the consumer will have some flexibility as to what data is shared by home testers with others (personal physicians, local or state authorities, or just CDC are good examples). I can't verify this officially, but hear that's the holdup, so with Covi-Mobile, perhaps an answer as far as EUA will come sooner than later.

In-sum: The S&P continues to evolve higher, to join the NDX already there. Caution is encouraged especially in those super-caps, one day soon a mini-plug pulling very likely will occur, even if within harmony of overall uptrends.