Market Briefing For Tuesday, April 14

-

The economic re-opening process will be this week's key

-

Mostly 'sector panels' will be announced; timeline vague

-

States defiant as Trump claims decision-process 'primacy'

-

The OPEC+ Oil production cut is unimpressive and insufficient

-

Saudi Arabia contends it is stronger; such as 20 million bbls/d

-

Trump says 20 million bbls/daily reduced; no evidence as yet

-

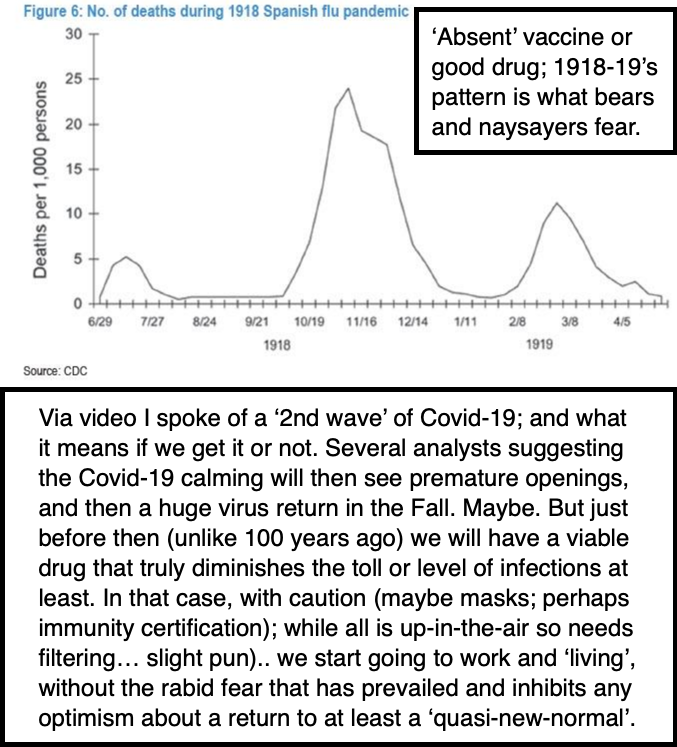

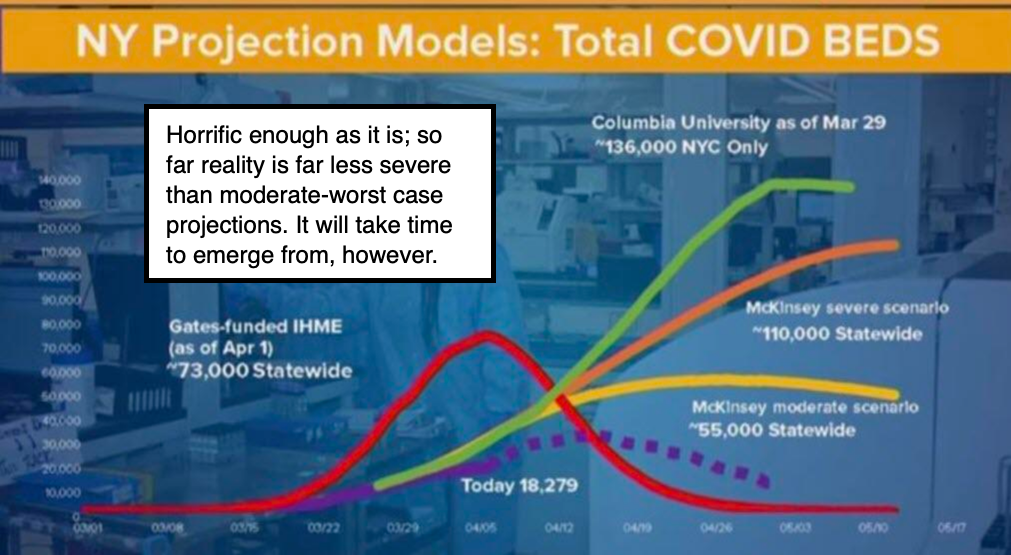

Covid-19-peaking is more a 'plateau' than a 'curve' for now

-

New antiviral drugs that effectively stop Covid-19 are key

-

Horrible Earnings aren't terribly relevant; but outlooks matter

-

Many (including banks) are impaired by 'who' they lent to

-

Whether Oil or mortgage bonds, risk is 'not' off the table

-

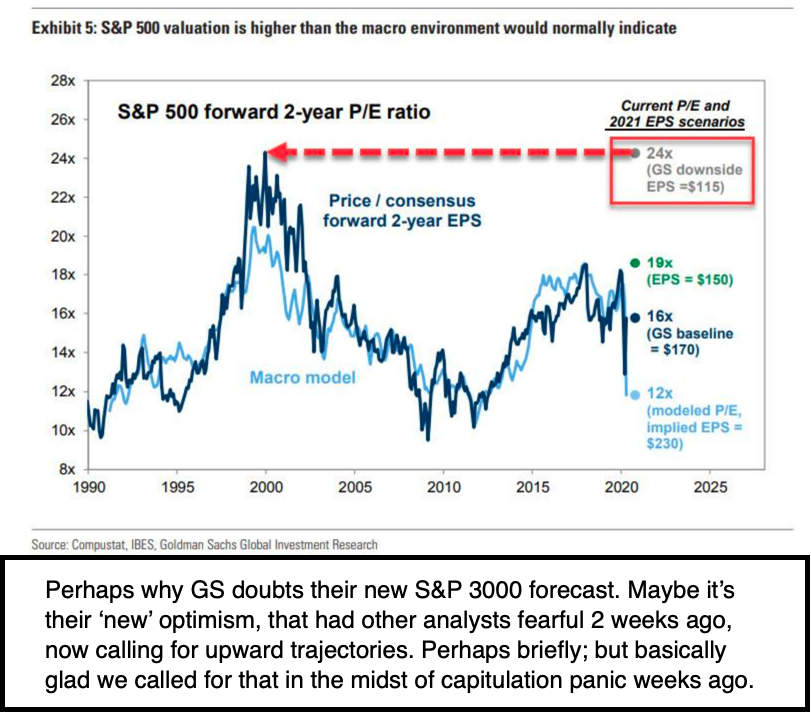

S&P to rebound intraweek 'if' we get a decent reopen plan

-

However the S&P is already in the targeted resistance area

-

Reopen trading prospect 'may' be faded later in the week

Strategists got off-sides - so to speak; hence you have several analysts upgrading market prospects suddenly; much as we've suggested caution, even though I have every optimistic desire to see 'The Inger Bottom' as potentially able to hold. In fact history suggests that rebounds of similar magnitudes retrace, but not catastrophically.

Of course that requires that we do have a medical solution (or treatment with efficacy), in-line with my oft-stated 'take death of the table' and we're good-to-go contentions. In the meantime, that doesn't mean we don't get into a 'range' or for that matter retrace somewhat, without a disastrous new decline thereafter. But for the moment we should regain stability.

The Fed of course sort of socialized a lot of debt, but the market point is a recognition of 'don't fight the Fed' even in this environment, as pointed to in contending that a washout low was made weeks ago, irrespective of gloom and doom, that still prevail (sadly) for so many Americans.

And while this is not going to revert to what was 'normal' on a dime, better things should unfold over time. So let's not focus too much on the obvious glaring negative fundamentals or earnings, because that's hindsight that of course the market discounted by virtue of the projected February-March 'crash', and that's part of why at least superficially they're minimized a bit for now. It is also helped a more 'activist' Fed and Congress, which had been barely functional. At the same time I believe many stocks are getting ahead of themselves as you have these reconstructed bulls now chasing.

In this regard, risk assets, including buys we advocated on the capitulation almost a month ago, don't necessarily have clear sailing ahead, hence the upgrades for stocks don't make a lot of sense 'now', although on pullbacks yes (depending on sector), and once the economy actually picks-up anew which will also be sector-dependent, regionally-varied, and tentative with regard to many ways life itself will change.

That's part of why technology, in my view, was the one sector investors did 'not' want to evacuate from (or in-fact utilize the washout into our indicated max-fear low, for buying, not selling). But again more 'then than now'. Just the fact these are the stocks that benefit from 'work-from-home' or also the 'entertain-at-home' trends, plus the push on cellular networks, much of this won't be as temporary as some think, but we won't likely fully revert to the older era's pattern of work and living. Again that will vary with industries.

Much of this will also depend (as the 'timeline' to rollout a return to 'normal' or what passes as a reasonable-facsimile thereof) how realistic reopening is and whether or not that results in a 2nd wave of Covid-19 in the Fall. I'll share charts that suggest how that could happen, and they make sense of course, but with one big caveat from me (even though I can't yet specify it, nor can anyone else): and that's the timing of a viable drug or vaccine.

The move in OIL on Monday was minimal, as $25/bbl oil isn't impressive at all, and it's conceivable that the Saudi's (perhaps the Russians) and even the Chinese, want to see the U.S. energy industry crippled. Bankruptcies, in many shale-dominant and over-leveraged oil companies are likely and it will require serious moves starting with the Texas Railway Commission on Tuesday to attempt stabilizing 'price' by mandated production cuts here in the US (which presumably Louisiana, Oklahoma and Kansas would join).

In-sum: the progress on a) drugs, b) business reopening schedule (even if tentative), and c) the Texas decision on oil production are the likely keys to this week's intraday and intraweek rebounds.