Market Briefing For Friday, April 17

Executive summary for April 17:

- President Trump announces 'states may make own decisions' and begin allowing public activities before this month ends

- We're not out-of-the-woods, but making process to reopening, while there's no assurance announced schedules are reliable

- Meanwhile parts of the U.S. economy remain in free-fall, albeit at a slower pace, given collapsed sectors simply stagnating

- Stocks in tourism/travel, down say 50% +/- easing lower, most damage already done, for those that will be ultimate survivors

- More depends on medical progress than political calculations, and today's news on Remdesivir shows how crucial this is (as especially we had heard a Chinese Trial was unimpressed, and this post-Close story was not released by a hospital trial leader or the Company, but is an anecdotal report), we hope it's valid but call this to your attention as actually there's no real news on it);

- Gilead's Remdesivir Trial seeing 'rapid recovery' in early data, is a report conflicting reviews heard in earlier anecdotal reviews, so it's welcomed (I repeat) but not with the focus media gave it (GILD)

- So (like with Hydroxychloroquine) hope springs eternal for now, don't forget (unless morphed into an oral formula), Remdesivir is an IV normally administered 'in-hospital', not earlier symptoms,

- Boeing to resume commercial 787 production next week, and it may resume 777x builds as well,

- Duration of social-restrictions a key variable for S&P prospects, and these already vary in our states and in several countries, the President's task force plans are fine; but can consume months

- Pressure to reopen must be balanced due to financial overload despair, which itself has health risks if not properly addressed, and basically tonight threw decision-making to the states

- Reopening scale to impact consumer confidence and markets, optimism may easily get-ahead of practicable reality for now, at the same time some states (Ohio will be one of the 29 noted as fairly well positioned) will reopen soon

- Risks of 'carnage' are not merely behind, but variable, clearly discrepancies exist even as we all share a common goal, and you could see short-term peaks from excessive near-term optimism

- We don't expect 'full' recovery in '20-'21, but 'waves', these will provide numerous trading swings amidst 'macro indecision', a lot of Wall Street forecasts will have to be adjusted to this reality

- Record-high big-caps (online economy) aren't broad reflections but have dominated the S&P's recovery as outlined

- 'Wave' phases will continue providing trading swings, the next one may well be up-to-down; although a process as well

- The post-Covid new-normal will vary depending on 'science', not political pronouncements; which must vary as conditions shift

- As optimistic -but realistic- patriots, we favor progress, both as relate to economic revival and medical progress easing turmoil

'New Normal (Travel +) Speculation'

Meanwhile . . many mandated travel policy measures aren't enforceable, that's why people have to do the right thing, but commercial carriers at this point can't really depend on travelers, so you get imposed airline controls, like Emirates, the first airline (today) to impose a blood test (fast version) on every passenger that wanted to board one of their few operating flights.

You certainly can't do that on the NYC Subway system or PATH trains, but you can compel wearing masks, or ultimately some less-intrusive version of what China does, with QR codes on your cellphone that indicates what your health status is believed to be. None of this is foolproof, nor will it be.

Against this backdrop; one can envision a 'slow reopening, slow recovery and no 'V- turnaround by the economy, though it may initially see a 'relief romping' by people as they are seemingly-released from cabin fever for at least awhile (with the risk of a fairly swift 2nd wave should many exercise what are their 'Constitutional' rights, pushing the envelope to prove points, that may be correct, like the crowd in Michigan agitated, but risks health of their compatriots and then anyone they come in-contact with for days).

Risk-appetite for stocks, and careful culling of sectors that may be harmed or benefit, remains essential. Just for-instance, everyone wants a return to their formerly-normal lives. Those businesses that can efficiently operate from home (most banking and financial fields are included) may see cost savings if they reduce need for office-space and travel expenses ahead.

It of course means that -especially if a covid-19 vaccine really is a year or more off- a return to anything like the levels of 'business flying and hotel utilization' is a pipe-dream. Leisure travel will try opening but sketchy as to what will be doable. Look at Disney World Shanghai for clues, limited entry with compulsory masks and health certification (those QR codes).

Cruises shot themselves in the foot, by not properly caring for their crews, and thus contributing to passenger viral spreading (now there is the start of the series of lawsuits against Carnival, beyond a claim), as it's fairly obvious a known concern about coronavirus did not prevent Carnival from 'boarding' passengers on later cruises, as a retired Dallas firefighter and his wife, detail in an Action). Media claims about 'high forward bookings' was not correct as suspected, with the source admitting massaged data.

Reopening won't be helpful in the health sector (aside breakthrough drugs of course) to some degree, as 'normal' patients without virus will hesitate, or at least continue to defer, almost any elective (or borderline essential) trips to doctors, hospitals, laboratories, or anything related, for some time. (I'm an example, twice postponing routine lipid blood tests simply because I'd rather not be in-proximity to strangers in a medical environment for now and especially as my sense is that there's no change; hence just delay.) It is reported that medical practices are struggling with no procedures to do, so they will be eager for elective outpatient surgery to resume.

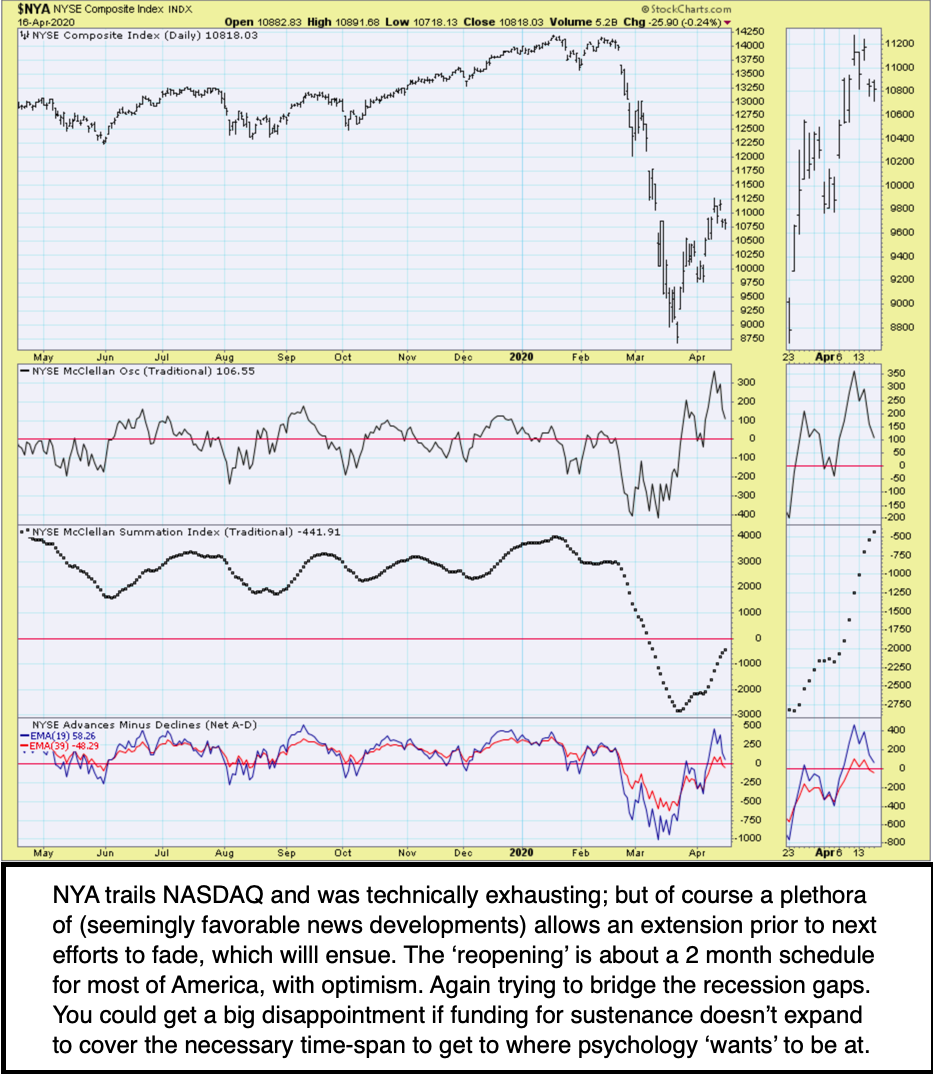

Technically. . the market got ahead of itself with the enthusiasm for the reopening, and we were absolute cheerleaders for the turnaround from the very day of 'max-fear' amidst the panic just over a month ago. Now we're likely to see a short-term blow-off spike of sorts.

That's vastly different than those who only got comfortable buying earlier in this week, after the S&P (SPY) retraced essentially half of the prior projected 'market crash' in February and March. Our point was to 'fade' unjustified euphoria in late-January / early-February, and buy extreme despair as that arrived in March along with a few hedge fund or other forced liquidations.

Just because we very closely got the top and trading bottoms right, surely doesn't mean we'd have any reason to chase the Averages higher recently with the crowd. Just the opposite possibly, as the permabulls parroting the old adage about no market recovering 50% fails to continue on up, misses the point, and as technicians tend to do, views charts in a vacuum. (By the way that often works in a trading-range market with no seminal changes in the basic underpinnings by which a macro picture is built. This isn't that.)

So, while the President will proclaim that everything will surge back to the old economic levels (stocks too), that's hardly sensible, though we know it could occur only 'if' OIL demand and price were to soar and game-changer antiviral drug emerge 'affirmed by science not aspiration' very quickly. So I will say that is possible, but again: 'that's not technicals in a vacuum'.

Longer-term, there is a new Harvard study suggesting this virus is every bit as tricky as we all realize, and that it may mutate significantly in months just ahead, which would reduce prospects that early vaccine(s) efficacy is going to be 'as protective' as would be not just desirable, but essential, as permanent organ damage can occur from Covid-19 if allowed to simmer a long time, 'even if' the patient doesn't find themselves ever in an ICU.

Not a pleasant thought, but it might become the reality they fear. If (and it's too soon to assess of course beyond the Harvard study) that's the case, of course Wall Street will have to further extend the timeline for GDP and big cap earnings recoveries; aside those companies (already expensive) that benefit from families compelled to virtually live-life from their 'cocoons'. It's hoped we all emerge from that restricted lifestyle in the months ahead.

Telecommunications stocks, especially those that pay good dividends and can be reasonably assured of being able to continue doing so, should hold or even advance during such a time. Video-conferencing stocks are either already overpriced, or may periodically be acquired by larger carriers (that creates network symbiosis, a trend in the business world already).

That actually means that the online-lifestyle that evolved for years (and for sure that's something to be thankful for, lest we be even-less-prepared for what just happened and being stuck at home so persistently) perseveres, even if the economy is largely able to be reopened. At worst they and tech (largely) have less problems going-forward than most companies that are struggling to figure-out how to attract business, not just ramp-up internally.

Conclusion: for now the drama of 'The Inger Top' over two months ago, and 'The Inger Bottom' (over one month ago) are evolving into a volatile trading range, but that range has been meandering at the higher levels for now; which it entered some days ago.

The reality is we caught this, but the numbers that are coming will be both worse-than and less-severe (depending on reports) than any consensus. I see this as a debate about the next phase, recognize the depth of severe recession not just here, but forthcoming; while focused on the 'duration' as may relate to medical progress, which will either expedite getting past this or compel further downgrades of expectations for an extra year or two (as would drive the Indexes, not necessarily all sectors, to lower lows).

In a sense that's an argument for concentrating in fairly steady stocks that have done well through the up-and-down phases, preferably with reliable (sustainable) returns, and occasional speculative picks during washouts; a good example being our advocacy of buys virtually at the March lows.

For now there's little reason to chase, which is what some managers (who as thought likely, deployed leverage to bail-themselves-out weeks ago) did and why they (or banks with questionable loans and loan reserves) remain more nervous than zero-margin holders of assets, that will be periodically volatile but are survivors.