Main Street optimism edged higher in August, as the NFIB Small Business Optimism Index rose to 100.8. That reading sits above the long-term average of 98 but missed the consensus estimate of 101. Stronger sales expectations led the improvement, with a net 12% of owners anticipating higher real sales volumes. This represents a six-point jump from July. The Uncertainty Index also declined by four points, showing less concern around financing and capital expenditures.

Business health improved as 68% of owners rated conditions “good” or “excellent.” Profit trends notched their best level since March 2023, while fewer firms raised prices, and financing costs eased. The average short-term loan rate fell to 8.1%, the lowest since May 2023, providing some relief for Main Street borrowers.

Still, Main Street challenges remain. Owners have consistently cited labor quality as the top issue, with 32% of Main Street reporting unfilled job openings. While this marks the lowest share since 2020, it still reflects persistent hiring difficulties, especially in construction and manufacturing.

The bottom line: For investors, the survey results are a welcome contrast to broader signs of economic cooling. Main Street is becoming more optimistic again, but the miss relative to expectations and ongoing labor shortages temper the headline.

What To Watch Today

Earnings

- No notable earnings releases today

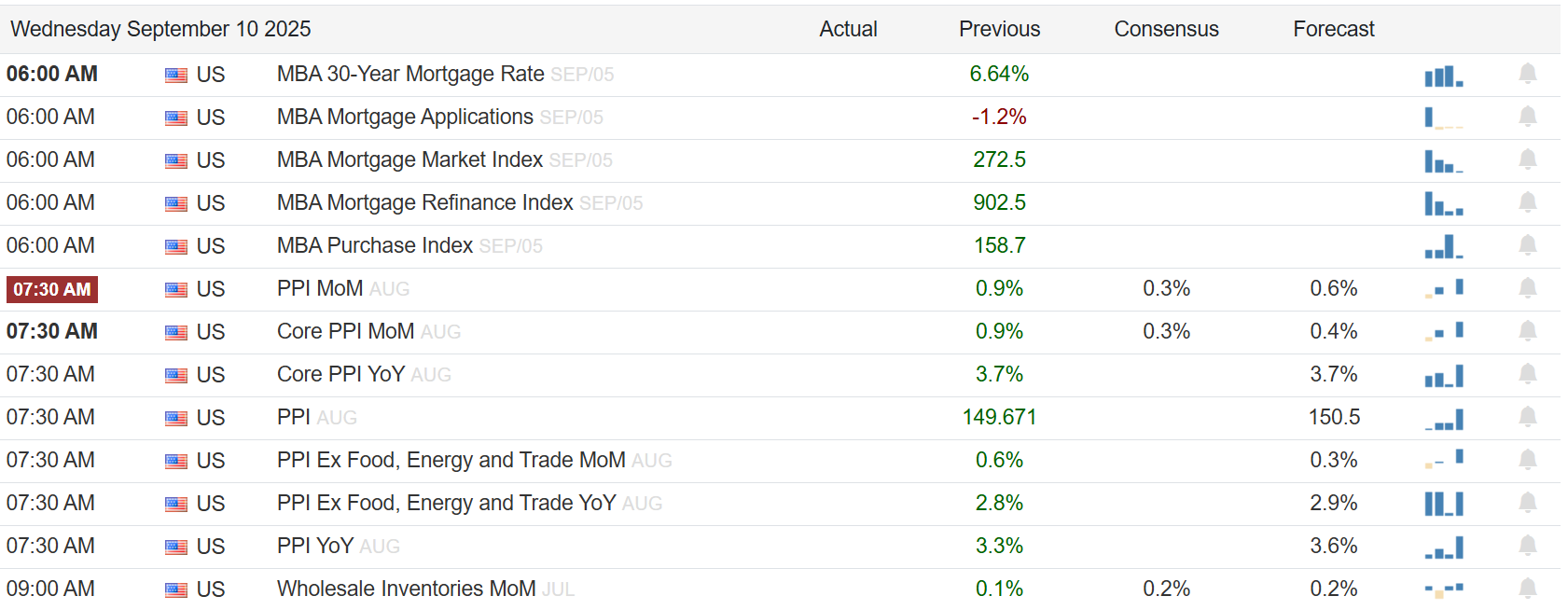

Economy

(Click on image to enlarge)

Market Trading Update

In yesterday’s daily market commentary, we discussed the recent rally in bonds which are now outperforming cash. The latest employment revisions of a loss of 911,000 jobs certainly adds to the backdrop of a weakening economy and bolsters the odds of a Fed rate cut next week. Today’s CPI and PPI data will be closely watched for any sign of inflation, but an inline or weak print will cement rate cuts next week.

Yesterday morning, I noted the divergence between homebuilders and lumber prices. It is unusual that homebuilders are performing so well given the current housing market dynamics. More notably, if homebuilders were doing as well as stock prices suggests, lumber should be performing better. While previous divergences such as it is currently have existed previously, the magnitude of the divergence is notable. Either the “housing market experts” that are predicting a real estate crash are dead wrong or lumber prices are suggesting that a crash is coming.

(Click on image to enlarge)

Interestingly, we see the same divergence in oil prices from oil stocks. Currently, energy stocks are priced well above the fundamentals of oil or we are about to see an economic resurgence that will push oil prices higher.

(Click on image to enlarge)

The real answer is that the flood of money into ETF’s, and subsequently the underlying stocks, has created a divergence between the companies and the underlying fundamentals. That flood of money that began in 2021 has pushed all asset classes into extreme long-term overbought conditions. The eventual reversion, when it comes, will not be pleasant and given that so many assets classes are simultaneously extremely overbought, the rout will be broad based.

In other words, while it is okay to own assets from bitcoin, to gold, to stocks, to homebuilders and energy stocks, don’t forget to take profits and rebalance risks accordingly.

Preliminary Payrolls Revision Disappoints

The BLS released its preliminary estimate of the annual payrolls benchmark revision yesterday, showing job growth for the 12 months ending in March was overstated by 911,000. While the figure grabbed headlines, it’s important to remember this is a preliminary estimate. The BLS won’t publish the final revision, which will adjust monthly payroll data from April 2024 to March 2025, until February 2026. Most notably, in recent years, the final revision has come in smaller than the first estimate.

The process is routine. The BLS reconciles its monthly survey with more comprehensive state unemployment tax records each year, providing a “preview” in September and a final adjustment later. As shown in the chart from Bloomberg below, last year’s preliminary revision showed an 818,000 job overstatement. However, the final adjustment in February reduced the overstatement to 598,000.

The key question is whether today’s report changes the Fed’s calculus. The answer is no. Powell flagged at Jackson Hole that such revisions were likely, noting that administrative data already pointed to a material downward revision. Moreover, the adjustment doesn’t alter unemployment rates, given that they are derived from another data set. Finally, the revision says nothing about job creation since March. As such, while the revision bolsters the odds of a Fed rate cut this month, it’s unlikely to shift monetary policy outlook materially.

Meme Stock Trading & Livermore’s Approach To Speculation

So, how do you navigate a “meme stock trading” market and “live to tell about it?”

Jesse Livermore’s approach in 1916 remains relevant in an era defined by meme stock trading, speculative retail trading, and extreme passive index concentration. Livermore understood that the market is rarely rational in the short term. Prices can extend beyond fundamental value when driven by sentiment, liquidity, or herd behavior. His method was not about predicting tops or bottoms but identifying when the market’s internal strength was shifting.

Livermore stayed long when the leaders, the strongest stocks, continued to rise. However, he watched for early cracks, like when those leaders began underperforming the broader market or when volume patterns signaled distribution rather than accumulation. When leadership broke down, he reduced exposure gradually, moving from aggressive long positions to a balanced stance, and only then to outright bearish trades when weakness spread across the board.

Tweet of the Day

More By This Author:

Healthcare Jobs Keep Labor Market Afloat: But For How Long?Why Diversification Is Failing In The Age Of Passive Investing

Earnings Are Becoming Harder To Come By

Comments

Log in or sign up to join the conversation.