Image source: Pixabay

The Federal Reserve’s aggressive fight against inflation has savaged financial markets. Along the way, I have taken note of bouts of navel-gazing over inflation indicators. Many of us have little operating experience navigating inflation, so perhaps it is natural to get sidetracked staring at an indicator or two that confirms a desire to see an end to inflation or that confirms the persistence of inflation. Since the U.S. last had an inflation problem over 40 years ago, the data samples are quite small for making conclusions about today’s unique mix of ingredients. Yet, since the Fed has expressed fears about entrenched inflationary psychology, consumer expectations for inflation have entered the basket of metrics used for assessing the Fed’s every move.

For example, back in April 2022, Richard Corbin, a research professor at the University of Michigan who has directed consumer sentiment surveys since 1976, issued this ominous warning in describing “inflationary psychology”:

“There is a high probability that a self-perpetuating wage-price spiral will develop in the next few years. Households have already become less resistant to paying higher prices and firms have become less resistant to offering higher wages. Prices and wages will continue to spiral upward until the cumulative erosion in inflation-adjusted incomes causes the economy to collapse in recession……Although consumers have increasingly expected higher inflation, they have also expected a strong job market and rising wages, especially among consumers under age 45. In the year ahead, wage gains will continue to reduce resistance to rising prices among consumers, and the ability of firms to easily raise their selling prices will continue to reduce their resistance to increasing wages. Thus, the essential ingredients of a self-perpetuating wage-price spiral are now in place: rising inflation accompanied by rising wages.”

“Inflationary Psychology Has Set In. Dislodging It Won’t Be Easy” – Richard Corbin

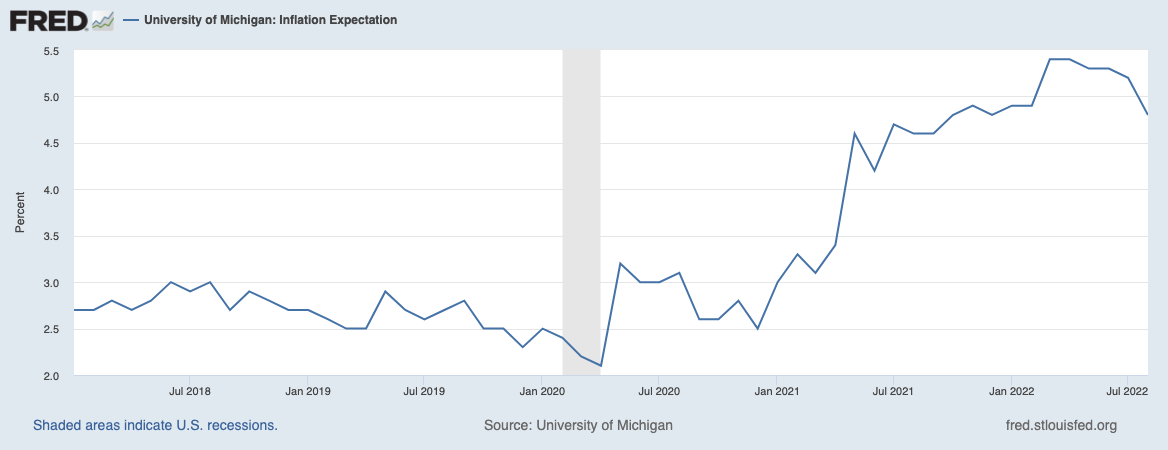

Note well that the University of Michigan’s U.S. consumer sentiment survey showed that 1-year inflation expectations last peaked in March at 5.4%. There have been encouraging signs from the subsequent drift downward. However, hopes were dashed that these numbers could convince the Fed to pause after October’s 1-year expectation of 5.1% delivered a significant jump from September’s 4.7%. In other words, at best, expectations may be stabilizing at high levels, especially with core CPI surprising to the upside in September. Note, Corbin warned about over-extrapolating trends from wiggles in inflation numbers:

“Another critical characteristic of the earlier inflation era was frequent temporary reversals in inflation, only to be followed by new peaks. That same pattern should be expected in the months ahead.”

Surveys of Consumers, University of Michigan, University of Michigan: Inflation Expectation© [MICH], retrieved from FRED, Federal Reserve Bank of St. Louis, (Accessed on 10/16/2022, note the data are updated only through August per agreement)

For reference, the 5-year inflation expectations remain just above 2% which indicates consumers are still clinging to the confidence that over the “long-term” inflation will return to the “before times”.

Federal Reserve Bank of St. Louis, 5-Year, 5-Year Forward Inflation Expectation Rate [T5YIFR], retrieved from FRED, Federal Reserve Bank of St. Louis, October 16, 2022.

Corbin wrote on the heels of the Fed’s first rate hike which was a mere 25 basis points. Corbin reacted with dismay and presciently argued:

“What was perhaps more surprising was that the quarter-point hike the Fed adopted in March was simply too small to signal an aggressive defense against rising inflation. Instead, it signaled the continuation of a strong labor market along with an inflation rate that would continue to rise.

Much more aggressive policy moves against inflation may arouse some controversy. Nonetheless, they are needed.”

Apparently, the Fed got the message and has been aggressively hiking starting with May’s rate hike!

If inflation expectations remain stubbornly elevated, then the time when the Fed is finally forced to take a pause could present a critical juncture of economic tension. In this scenario, I expect those who applaud the Fed’s pause will dismiss ongoing high inflation expectations as transitory or even uninformed. Watch out if those expectations achieve new highs in the wake of a Fed pause.

The current controversy about aggressive policy demonstrates an instructive contrast with the last tightening cycle. What a different pace can make! The S&P 500 (SPY) (red line with the scale on the right) had little problem drifting higher while the Fed tightened with baby steps from 2016 to 2018. A sharp correction in late 2018 helped to convince the Fed to pause and then bring rates down. Market participants are still waiting for the Fed to care about the current market sell-off in the wake of higher rates.

Board of Governors of the Federal Reserve System (US), Federal Funds Effective Rate [FEDFUNDS], retrieved from FRED, Federal Reserve Bank of St. Louis; S&P Dow Jones Indices LLC, S&P 500 [SP500], retrieved from FRED, Federal Reserve Bank of St. Louis, October 17, 2022 (data available through September 1, 2022)

Be careful out there!

More By This Author:

Why The Fed Won’t Read Cathie Wood’s Open Letter

Fed's Daly: The Market Is Wrong About A Hump In 2023 Fed Rates

Softening Inflation Expectations Are The Beginning Not The End Of The Fed’s Hawkish Posturing

Comments

Log in or sign up to join the conversation.