Photo by Colin Watts on Unsplash

Let’s start with the bad news: UK headline inflation is back at 3%, up from 2.5%, after briefly dipping below the Bank of England’s 2% target last Autumn. That’s a tad higher than expected, though almost entirely because of a near-1% month-on-month increase in food prices, which is hard to explain. Even so, headline CPI is poised to remain in the 3% region for much of this year and we expect a peak of 3.5% later this year. Much of this can be traced back to household energy bills, which are set to increase again in April due to rising wholesale natural gas prices.

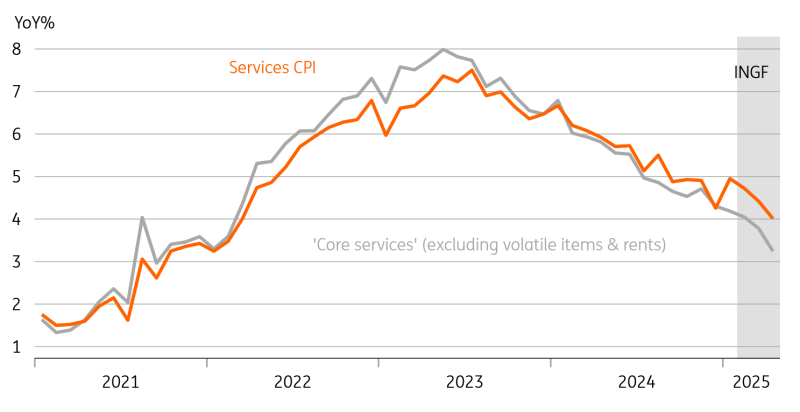

But energy and food are of little relevance to the BoE’s decision-making. What really matters is service sector inflation, and here the news is getting better. Admittedly services CPI did rebound up to 5%, though that was lower than expected and followed an artificially low reading in December. Airfares didn’t properly account for the usual surge in prices around Christmas.

Again though, airfares don’t matter for monetary policy. And once you strip out the volatile items as well as rents, ‘core services’ inflation is falling. There isn't a single official measure of this, but when we calculate it, we tend to strip out things like airfares, package holidays, and also rents. Rental growth has been relentless, but the Bank of England doesn't seem to put much weight on it.

By our calculations, that measure of ‘core services’ inflation now sits at 4.2%, down from 4.7% two months ago.

UK services inflation measures

Core services excludes items like air fares, package holidays, education and rents

Source: Macrobond, ING calculations

We expect this trend to continue. We think the measure of ‘core services’ can dip below 4% within the next couple of months, while overall services inflation could be there by the summer. Crucially, that’s a faster fall the Bank of England is currently forecasting. Huge chunks of the services basket are subject to annual price hikes in April, which owing to lower headline inflation, should be less aggressive than they were in April 2024.

If we’re right, that wouldn’t necessarily speed up the pace of rate cuts, but it would help cement a total of four cuts this year. We also expect rates to fall to 3.25% in 2026, which is a fair bit lower than markets are currently pricing.

More By This Author:

The Commodities Feed: Supply Risks Vs. Peace Talks

FX Daily: Euro Paying EU’s Isolation

Japan’s Export Jump May Be Calm Before Trumpian Storm

Comments

Log in or sign up to join the conversation.