Eyewatering increases in household energy bills between now and next April mean inflation is likely to head above 12% from October. But core inflation might have peaked - or is close to peaking - now that goods price pressures are easing. We expect another 50bp rate hike from the Bank of England in September.

UK inflation has gone above 10% for the first time since 1980, and indeed both headline and core CPI measures came in above expectations. A lot of that surprise can be traced back to a huge 2.2% month-on-month increase in food prices (in the case of headline CPI) and a sizable increase in various housing costs (in the case of core).

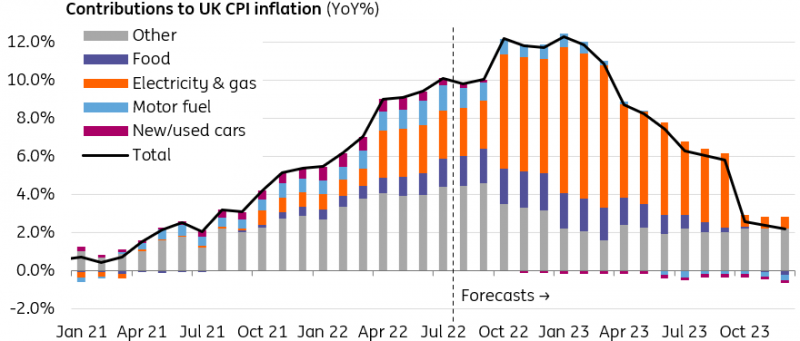

Next month, headline inflation looks set to dip back below 10% on a near-7% fall in average petrol/diesel prices, which came too late to affect the July figures. But as everyone knows, that’s only a temporary reprieve with a 75% increase in the household energy cap on its way in October. While it’s not totally clear yet how the Office for National Statistics will treat the government’s £400 discount for household bills, this increase in electricity/gas costs looks set to take inflation above 12% later this year.

UK inflation set to head above 12%

Source: Macrobond, ING

Plugging the latest wholesale gas and electricity costs into the regulator’s spreadsheet, we estimate that the average household bill will have risen from roughly £2000 currently, to £3500 in October, before heading to roughly £4500 in January and above £5000 in April next year. That latter figure is £1000 higher than it was when we ran these figures at the end of July and reflects a further abrupt rise in gas prices over recent weeks.

Those sequential increases mean that inflation is likely to hover around (or a bit above) 12% from October through to about February. Thereafter the energy impact will gradually dissipate and in fact, by 2024, inflation is likely to be a bit below the Bank of England’s 2% target – assuming that energy prices do indeed begin to gradually edge lower from mid-2023.

What matters more for policymakers are signs of persistence in the inflation numbers. And once food and energy costs are stripped out, core inflation looks like it might have peaked – or is close. Goods price pressures look set to ease over coming months now that commodity costs have fallen and the insatiable demand for ‘stuff’ seen through the pandemic has faded, and retailers are reporting they have more inventory. Used car prices, which were one of the most extreme examples of pandemic-related goods inflation, have fallen 7% since January.

Instead, it is wage pressures that will heavily influence the Bank of England’s decision-making over coming months. As we discussed yesterday, wages (at least in nominal terms) have decent momentum right now, but there’s a lot of uncertainty over how far labor demand is falling, and how much labor supply is improving. In the near term, skill shortages remain a big issue for companies

For now, we expect another 50bp rate hike in September. We wouldn’t rule out another hike in November, though this heavily depends on the fiscal response from the new prime minister in September.

More By This Author:

Japan’s Exports And Core Machinery Orders RecoverUS Strength In 3Q To Give Way To Renewed 4Q Weakness

Czech Republic: Lower Financing Needs Than MinFin Expects, But Still A Lot To Cover

Comments

Log in or sign up to join the conversation.