Japan’s trade deficit widened in July as imports surged due to high commodity prices while forward looking core machinery orders rebounded in June. Today's data supports our view that GDP will likely continue to rise in the current quarter led by investment, but at a slower pace than the previous quarter.

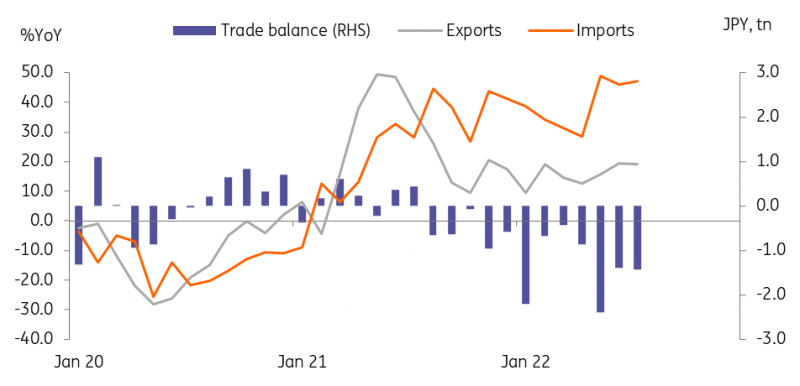

Imports grew faster than exports, deepening the trade deficit in July

Exports rose 19.0% year-on-year in July (vs 19.4% in June), a bit higher than the market consensus of 17.6%. Auto exports to the US and semiconductor exports to China were particularly strong. Meanwhile, imports jumped 47.2% in July (vs 46.1% in June), also above the consensus forecast of 45.5%, mainly led by the high cost of commodities.

Still, as global oil prices have dropped since June, we expect the trade deficit to narrow, with import growth decelerating. Also, auto exports are expected to improve as the production of other major automakers continues to increase. Thus, the contribution of net exports to GDP will likely record a small gain in 3Q (vs 0.0% in 2Q).

Trade deficit widened in July

Source: CEIC

Core machinery orders rebounded slightly in June

A leading indicator of capital spending, core machinery orders rose 0.9% month-on-month seasonally-adjusted in June (vs -5.6% in May), slightly missing the market consensus of 1.0%. In the second quarter, core machinery orders rebounded firmly by 8.1% quarter-on-quarter (vs -3.6% in the first). Thus, we expect Capex investment to improve in the rest of this year, with growth momentum slowing gradually. Auto and electrical machinery orders increased as global supply bottlenecks and China lockdowns eased while semiconductor manufacturing equipment orders fell for the first time in three months.

More By This Author:

US Strength In 3Q To Give Way To Renewed 4Q WeaknessCzech Republic: Lower Financing Needs Than MinFin Expects, But Still A Lot To Cover

China’s Economic Weakness Goes Beyond Real Estate

Comments

Log in or sign up to join the conversation.