UK GDP Only Fractionally Lower Due To Omicron

Photo by James Giddins on Unsplash

Another surge in health spending helped offset Omicron-related weakness in consumer services, to deliver only a modest hit to December's monthly GDP. The bigger economic challenge is now the cost of living crunch, which looks set to deliver steadier growth readings later this year.

On the face of it, December’s GDP data doesn’t look bad at all given everything going on with Omicron. We saw only a very modest 0.2% fall in activity compared to November, and that means the size of the economy was still roughly at its pre-virus level.

That benign story does, admittedly, mask some pretty big shifts beneath the surface. Activity fell sharply everywhere you’d expect, including a 9% fall in hospitality output and a 4% slide in entertainment & recreation, all presumably down to increased caution before Christmas. But this was offset by another sizable increase in health output, owing to the ramping up of vaccines and testing before the end of the year. And in fact, if health spending had hypothetically remained unchanged through the pandemic, GDP would be some 1.3% lower than it is now.

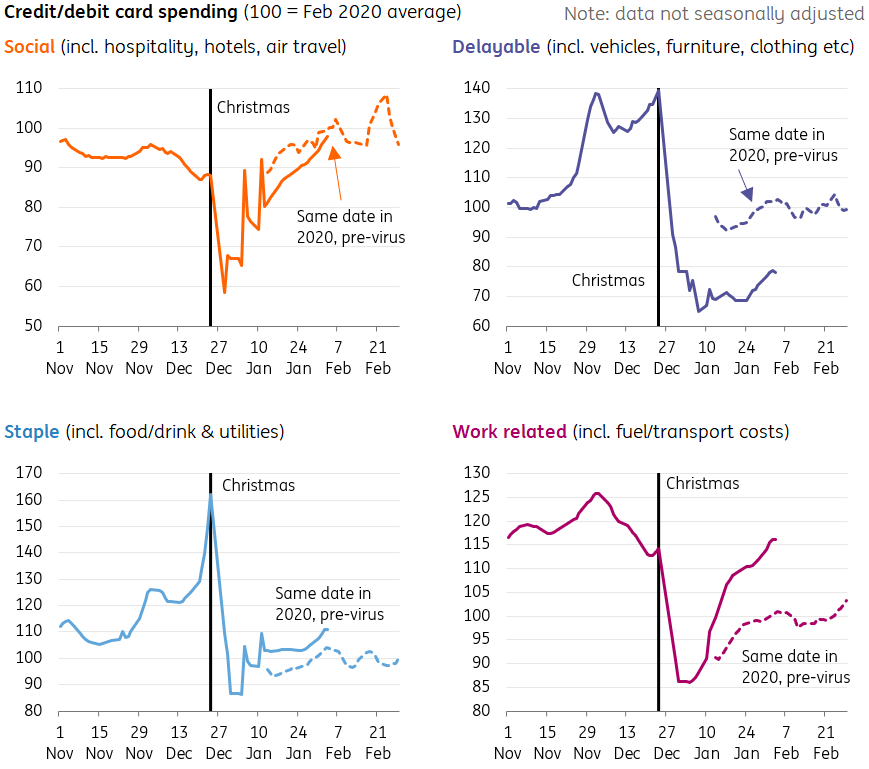

It goes without saying that all of this is pretty ‘old news’ now. Virtually all of the more recent indicators we’ve been watching have staged a turnaround since the start of the year. Social spending has returned to comparable levels to the same time in January 2020. The percentage of people saying they have visited an indoor pub/restaurant recently has returned to levels seen through the autumn. And the latest ONS business survey has shown a marked drop in staff absences due to Omicron. January’s GDP may stage a further modest decline, but any losses are likely to have been mostly returned through February.

UK social spending is close to Jan 2020 levels

(Click on image to enlarge)

Image Source: Macrobond, ING

The bigger challenge now facing the economy is the cost of living crisis. Disposable incomes are set to decline noticeably this year on a combination of tighter fiscal policy and to a greater extent, higher inflation. Consumers have accumulated plenty of 'excess savings' during the pandemic – now totalling roughly 8% of GDP – and that will help to offset some of the income shock. However, it is worth remembering that this savings buffer is more heavily concentrated in higher-income earners, who are less likely to cut back their spending dramatically in response to the rising cost of living. Economic growth rates are likely to slow later this year.

Importantly though the Bank of England has already factored a lot of this into its forecasts. If anything policymakers may need to revise up their near-term growth projections due to the milder Omicron impact. That suggests that the Bank is on track to hike at the next two meetings. But a slower growth outlook is one of the reasons why we suspect policymakers will deliver less tightening than markets currently expect over coming months

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more