Image Source: Pixabay

MARKETS

U.S. stocks finished mostly lower on Friday, dragged down by a technological sector slump. However, major equity indexes still managed to post gains for the week, driven by investor enthusiasm for AI growth, which continues to be more appealing than concerns over prolonged high interest rates.

Expectations for a near-term rate cut were dealt a blow as the U.S. economy showed unexpected strength. According to preliminary PMIs released on Friday, early June, economic activity picked up. S&P Global’s services gauge exceeded estimates, rising from May to reach 55.1, the highest reading in over two years. The composite index also achieved a 26-month high at 54.6. The report highlighted a strong year-to-date service activity recovery driven by robust domestic demand, resulting in the strongest new work inflows in a year.

The manufacturing sector also showed resilience, with the factory gauge increasing to 51.7 in the flash estimate for June. These positive readings contradict the slowdown narrative that had been gaining traction amidst a series of weaker economic reports, pushing Bloomberg’s U.S. economic surprise index to a five-year low. However, Friday’s data suggests that the U.S. economy is expanding at a healthy pace of approximately 2.5%.

BLOOMBERG ECONOMIC SURPRISE INDEX

As we reach mid-year, financial markets are demonstrating robust performance, supported by a resilient economy, decelerating inflation, and the early signs of central bank easing. If these conditions persist, we may be on the cusp of a significant transition in the economic cycle, which could have profound implications for financial markets.

Since the inflation spike in early 2021, we have closely tracked the performance of various asset classes against their historical trends during different phases of the inflation cycle. Despite each cycle’s uniqueness, including the current one, historical patterns have provided reliable insights thus far.

The challenging period of high inflation has transitioned into stronger gains driven by disinflation, particularly for U.S. equities. We define disinflation as periods when U.S. core inflation exceeds 3% year-over-year but is declining, as it is today. Core inflation, which was at 3.4% year-over-year in May, is projected to slow further throughout the year, potentially falling below 3% year-over-year by early 2025. This indicates that we are in the latter stages of a favourable disinflationary environment for the remainder of 2024.

As disinflation progresses, a pivotal development to watch later this year will be the shift towards central bank easing. Historically, this combination has been favourable for asset returns. It is crucial to understand that central bank easing does not always result in strong equity returns, as the reasons for rate cuts—often linked to recessions—are pivotal. However, since the early 1980s, the initial phase of Federal Reserve easing has been one of the most challenging parts of the cycle. Nevertheless, when the Fed eases during a disinflationary period, which typically does not coincide with a recession, returns tend to be stronger for both equities and bonds.

In conclusion, we are in the latter stages of a favourable macroeconomic environment for asset returns. Historical patterns suggest that returns should remain strong, potentially even improving, as the Fed moves into the policy normalization phase.

FOREX MARKETS

The USD has been on a winning streak this past week, gaining ground against other major currencies. Thanks to the political drama in France and the Bank of Japan’s leisurely approach to policy changes, the USD is looking more attractive by the day. This happened even as U.S. yields dipped due to softer inflation data and signs of a cooling labour market. Adding to the USD’s momentum, Chinese policymakers seem quite content to let the CNY drift lower against the USD.

Market watchers are bracing for a weak U.S. PCE deflator report in the upcoming week, which could give the USD an extra push just in time for the French elections. Meanwhile, high-beta G10 commodity currencies hold their own, buoyed by investor optimism for a gentle global economic landing.

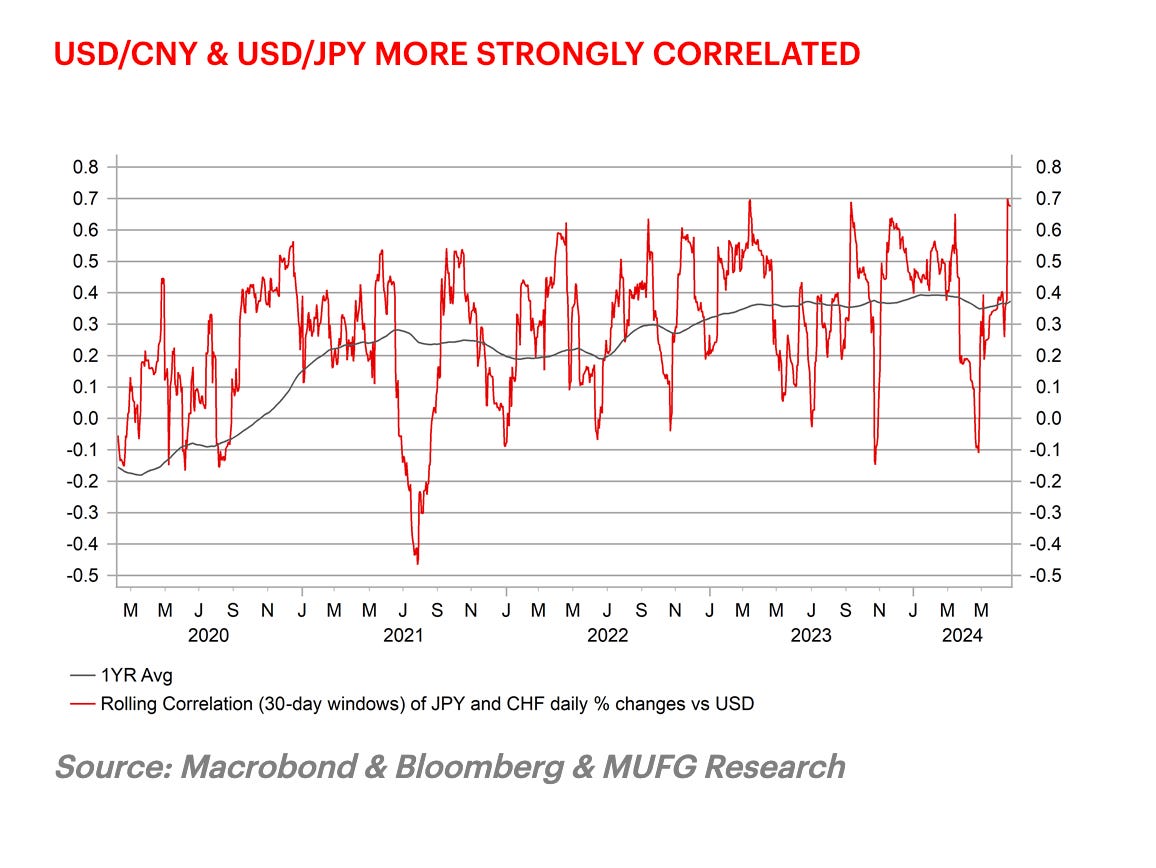

The “follow you follow me dance” between USD/JPY and USD/CNY continues, as USD/CNY reached a new high for the year overnight at 7.2925, inching closer to last year’s peaks between 7.3000 and 7.3500. The People's Bank of China is nudging this along by setting higher daily fixes. This week’s fixings were particularly eye-catching, jumping from 7.1159 to 7.1196 on Friday. This move has the market buzzing with speculation that Chinese policymakers will allow the CNY to weaken further as we head into the U.S. election season, where trade tensions are expected to heat up again.

In short, it looks like the USD is set to stay strong, while Asian currencies might have a bit of a tough time keeping up. So, as the world turns and the currency markets churn, the USD stands poised to keep its edge, much to the relief of American tourists everywhere.

RMB DEVALUATION

Speculation is swirling that Beijing might consider a significant devaluation of the renminbi. Although it's a tantalizing thought, we don’t see this happening anytime soon. A sudden, steep depreciation (more than 5%) could cause more problems than it solves. For now, it seems China is sticking to its 'crawling peg' exchange rate regime.

The main argument for a devaluation is to boost China’s economy, much like the recent performance of the Japanese yen. Over the past three years, the yen has dropped from just over 100 to nearly 160, which has helped lift Japan’s consumer prices above the Bank of Japan’s 2% inflation target. Compare this to Japan's average inflation of just 0.5% from 2012 to 2021. So, the idea is that a cheaper renminbi could stave off disinflationary or deflationary pressures in China.

However, a large renminbi devaluation isn’t without its pitfalls. It could trigger capital outflows and financial instability. Even though Beijing has tightened capital controls since the mid-2010s, money still slips through the cracks. In 2023, corporate and household capital outflows exceeded inflows by $68.7 billion for the first time in five years. A rush of capital outflows could erode the banking sector’s deposit base and tighten domestic credit, further straining China’s already under the microscope due to asset quality issues in the residential property and local government financing sectors. These local entities are essential for building infrastructure so that any additional pressure could be problematic.

Weakening the renminbi also risks further aggravating China’s relationship with the West. The U.S. Treasury might label Beijing a currency manipulator, and Washington could ramp up tariffs on Chinese goods, especially with an election around the corner. Plus, a renminbi devaluation could prompt competitive devaluations across the Asia-Pacific region as countries strive to keep their exports competitive.

Despite these potential issues, China’s exporters seem to be doing just fine. Merchandise exports in USD grew by 7.6% year-over-year in May, stronger than expected. Chinese exporters have enjoyed a competitive edge from a nearly 15% depreciation in the real effective exchange rate since early 2022. As the interest rate gap between the U.S. and China narrows, the renminbi will likely appreciate from nearly 7.3 to around its fair value of 6.8 to the U.S. dollar.

So, the rumours that China is using its currency to jumpstart its economy might be more smoke than fire. The risks of such a move are likely too high for an economy already juggling numerous challenges. For now, it seems China will keep its currency strategy steady, much like a tightrope walker who knows that balance is key.

More By This Author:

S&P 500 Edges Back From Record Highs As Bond Yields Rise

Cutting Rates Might Be The Most Effective Strategy To Reduce Inflation In The U.S

U.S. Consumers Are Feeling The Pinch Of Higher Prices

Comments

Log in or sign up to join the conversation.