Today’s release of Canadian GDP for the fourth quarter of 2018 provides evidence that the Canadian economy is in recession. Whether one sticks to the technical definition of a recession (two successive quarters of declining output) or just a more broadly-based definition, the economy is clearly slumping. Canadian GDP just contracted for the second month in a row, leaving the headline Canada GDP up just 0.4% for all of the fourth quarter, 2018.

(Click on image to enlarge)

Figure 1 Canadian GDP Growth

The most disturbing aspects of the Statistics Canada release today was the 0.4% contraction in final domestic demand. This measures the actual products and services that are consumed by individuals and business locally. It is what actually goes out the door and does not include any build up in inventory for future sales. Here are the details of all the major components of GDP:

- Annual growth was 1.8% for 2018, following a 3.0% increase in 2017;

- Business investment spending fell 10.9% annualized in Q4;

- Residential investment fell 14.7% annualized in Q4;

- Exports of goods and services declined -0.1% in December;

- Businesses accumulated unwanted inventories of C$12.5 billion; the economy-wide stock-to-sales ratio increased from 0.825 in the third quarter to 0.840 in the fourth quarter;

- Canada's terms of trade—the ratio of prices of exports to prices of imports—fell 3.6% in the fourth quarter, the largest terms of trade decline since the first quarter of 2009.

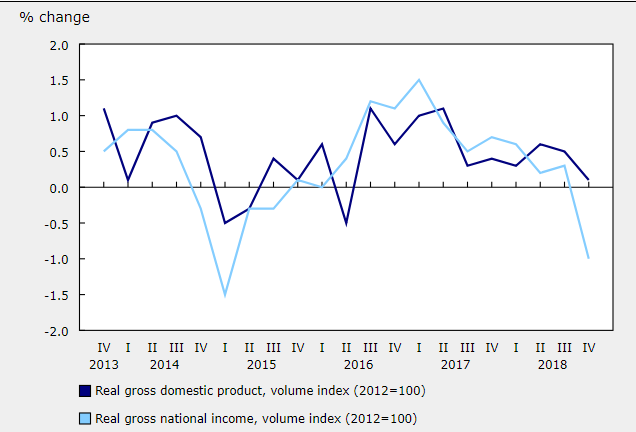

What is far more worrisome is the declines in national income along side declines in domestic output. Both are heading in the wrong direction (Figure 2).

(Click on image to enlarge)

Figure 2 Changes in Volume of Gross Domestic Product and Gross Real National Income

In a recent speech, the Governor Poloz of the Bank of Canada fretted that the path towards higher interest rates is “highly uncertain”, citing worries about housing and business investment. Today’s data release justifies his worries. At the same time, he stressed that borrowing costs eventually will need to go higher. It is hard to square this conviction that rates have to move up with an economy that has been slowing for nearly a half year and went into outright decline in the last two months of 2018. Perhaps, it is time the Governor to introduce the notion that the Bank expects to consider cutting rates.

Comments

Log in or sign up to join the conversation.