Even in the face of denials, markets are excited at the prospect of a joint EU fiscal response to the energy crisis. From an investors’ point view, this could solve many problems, and hence justify unwinding some of the ‘crisis pricing’ seen in rates markets. Near-term financial stability concerns are still prevalent, however.

Extrapolating from the EU’s COVID-19 fiscal response

Joint EU fiscal response to the energy crisis has become one of the hot topics, alongside geopolitical tensions and sanctions, ahead of tomorrow’s EU summit. Bond yields shed some of their crisis valuations yesterday when Bloomberg reported that the EU was considering ‘massive’ joint debt issuance to finance energy and defence spending. The report was later denied by EU commissioner Timmermans, but we think it will be difficult to put the genie completely back into the bottle.

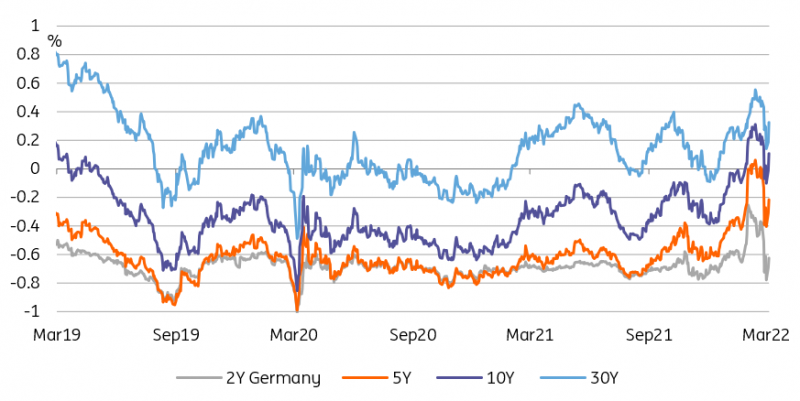

Hopes of fiscal spending sent 10Y Bund yields above 0%

Source: Refinitiv, ING

This is because a joint EU fiscal response is an alluring prospect in the eyes of financial markets. At face value, it would seem to address many of investors’ concerns:

- The impact of energy inflation on consumption

- The risk of a political backlash

- The risk of economic divergence between the EU countries most and least affected

- The risk of a financial shock to countries faced with a higher energy bill and higher financing costs

The reality is always more complicated and we will leave it to our economics team to address the likelihood and potential forms this could take (size, grants vs loans, etc) if the original report is confirmed.

One additional step away from negative yields, potentially

The way rates markets reacted to the news is telling. Firstly, it shows that the widespread assumption is that the EU COVID-19 fiscal response is the template for future fiscal decisions. This is understandable given the similarities between both crises: an external and asymmetric shock faced by member states. One has to expect some resistance from some corners of the EU however, as the funds from NGeu, a supposed 'one-off', are not even spent yet. Their persistent enthusiasm in the face of denials also shows that markets think this is not only an appropriate solution, it is also unavoidable.

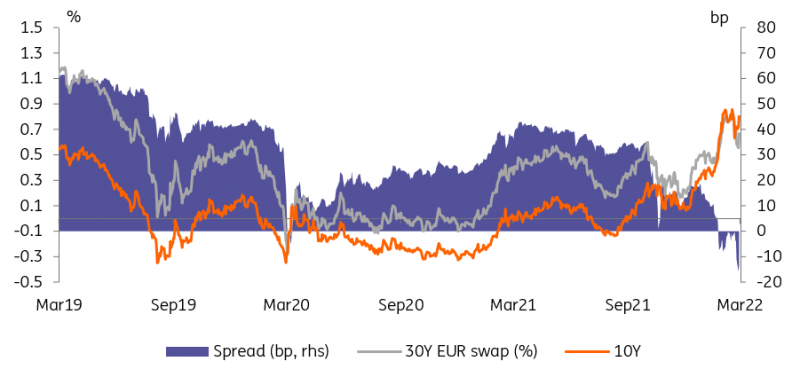

Rates are higher but the 10s30s curve is still inverted

Source: Refinitiv, ING

If there are no truth in these reports, denials will pour in over the coming days and that will be the end of it. In any case, the jump in outright rates, re-tightening of sovereign spreads and German swap spreads, and curve steepening reinforce our view that negative yields are only a temporary by-product of the current geopolitical tensions. As long as ECB normalisation is on the table, any drop below 0% yields for 10Y Bunds will prove short-lived.

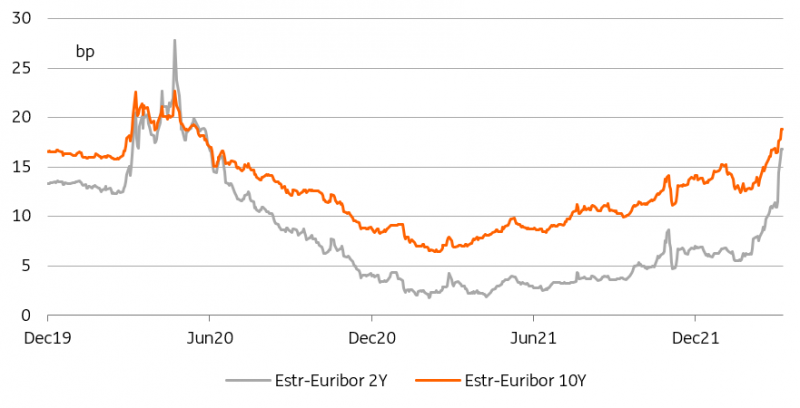

The widening €STR-Euribor basis shows financial concerns remain

Source: Refinitiv, ING

It is also noticeable that not all risk measures improved on the news. The basis between Euribor and €STR swaps, a proxy for bank risk, continue widening. This makes sense. Even if a joint fiscal response would address many of the economic ills, the risk of financial stress brought about, among other factors, by commodities short squeezes and by deleveraging, is still a prime concern.

Today’s events and market view

On the economic calendar today: Italian industrial production and US job openings. Realistically, these pale in comparison to other events later this week (ECB meeting, EU summit, US inflation) and to the importance of geopolitical and financials developments.

One topic that has emerged as a key driver of euro rates is the possibility of a joint EU fiscal response to the current energy crisis (see above). Ahead of tomorrow’s EU summit, we expect more headlines on the topic.

Markets cheered at possible concession offered by Ukrainian president Zelensky yesterday, although his comments were originally made on Monday. As foreign ministers from Ukraine and Russia are due to meet tomorrow, we would expect further headlines on the topic in the run up to the meeting.

Portugal is due to auction 5Y and 12Y bonds. The US Treasury will sell 10Y notes.

Comments

Log in or sign up to join the conversation.