Rates Spark: Duck-Diving The Fourth Wave

EUR Rates Caught Between Pandemic Surge And Hawkish ECB

Left to their own devices with holidays in the US, the European rates markets will continue to assess the potential impact of governments’ stricter containment measures as Covid caseloads continue to climb and with hospitalization rates at critical levels.

That this has not resulted in even lower core yields is at least in part also owed to the ECB sticking to its guns - PEPP will end as planned after March next year. ECB’s Villeroy reiterated this just yesterday, although suggesting again that the flexibility could be kept in a “virtual toolbox”. Sovereign spreads over Bunds are creeping wider, and US Treasuries and Bund received a significant bid for safety overnight on concerns of the emergence of a new, more transmissible, Covid-19 variant in South Africa.

The ECB had only just started acknowledging the increasing upside risks to its inflation outlook

Sure, uncertainty over the economic backdrop has increased with the fourth Covid wave in full swing, but the ECB had only just started acknowledging the increasing upside risks to its inflation outlook. Yesterday’s ECB meeting minutes were a testament to that, although it refers to a policy-setting meeting that predates the prominent speeches of ECB officials over recent days. Nonetheless, money markets stubbornly pricing in 10bp higher overnight rates by the end of next year is likely a direct reflection of the ECB’s desire to maintain "sufficient optionality in the calibration of its monetary policy measures".

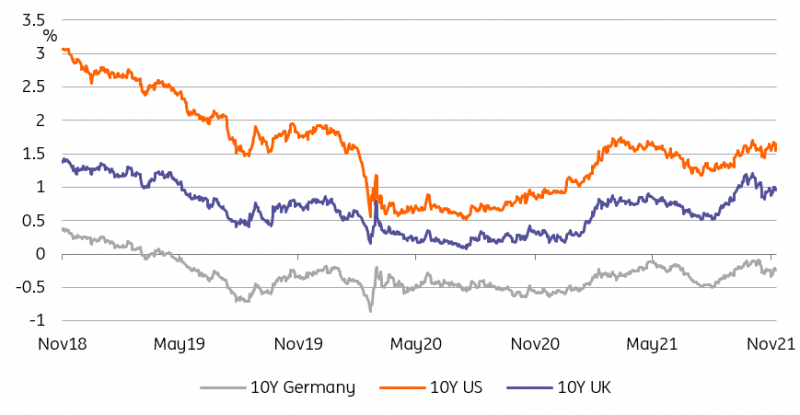

Fears Over A New Covid-19 Variant Have Sent Yields Lower Overnight

Image Source: Refinitiv, ING

What Lies Beyond Forward Guidance

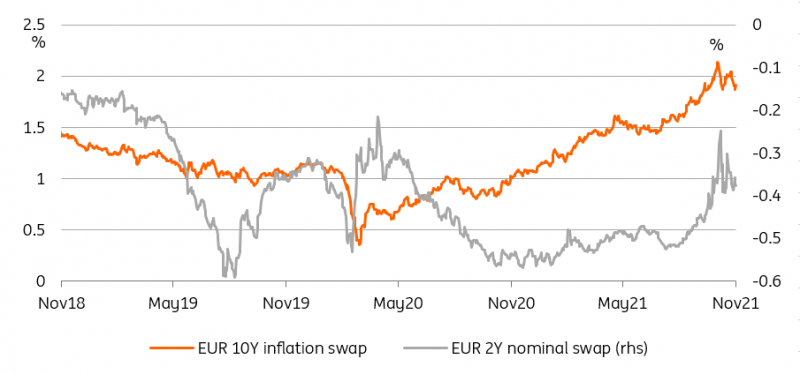

If even the ECB is hedging its bets, then this may already answer the question ECB officials discussed, as to “whether the jump in short-end EUR rates is as a result of markets questioning the new ECB forward guidance or its inflation forecast.” It is probably both. Market measures of expected inflation - such as the 5y5y inflation swap jumping over 2% around the time of the meeting - indeed indicate the fears that the overshoot of inflation could force the ECB’s hand, but naturally, the forward guidance in turn is based on the forecasts (FXE).

Looking ahead that situation could persist for quite a while if the ECB were to consistently underestimate inflation, forecasting that it will drop below its 2% target again.

On the other end, a quick glance to the UK shows us that the BoE is also one step ahead when it comes to forward guidance. Governor Bailey stated that the Bank has moved on to guidance which is “reminding people of the policy framework” - which is the “price stability business”. A 10bp hike at least is fully discounted by markets for December, with close to another 100bp of hikes over the course of 2022.

Higher Front-end EUR Rates Reflect Genuine Inflation Worries

Image Source: Refinitiv, ING

Today’s Events And Market Trend

The long Thanksgiving weekend will keep market activity depressed. The main focus is on the pandemic situation across Europe. In Germany chancellor Merkel called for stricter measures yesterday as infection rates continue to spike higher, though without going into details. Countries such as Belgium and the Netherlands are anticipated to announce stricter measures today.

Quite a few ECB members are again scheduled to speak, though the venue suggests topics outside of current monetary policy: Lagarde, Schnabel, Panetta and Lane all speak at the ECB’s Legal Conference.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more