The UK energy package being mooted could reduce the depth of a winter recession and shave up to 6 percentage points off January's inflation peak. But depending on how it's financed, private investors will be asked to increase exposure to gilts by a record amount. And that could leave the pound even more vulnerable.

UK energy package would reduce recession risk and lower inflation

Liz Truss has been formally sworn in as the UK’s new prime minister and it looks like her first act will be to cap energy prices for both households and some businesses. Press reports vary on the finer details, but most suggest that electricity and gas costs could be fixed around their current level of £2,000 for the average household per year. That would avoid the planned increase to £3,500 in October and potentially well over £5,000 next April, on an annualized basis.

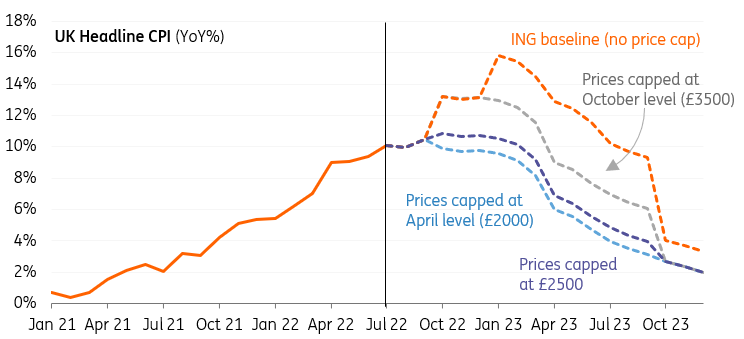

There’s plenty to debate about a blanket price cap, but the obvious benefit is it’s clear and straightforward for consumers and should have a material impact on confidence. It should reduce the depth of a winter recession, and would also mean inflation has already more-or-less peaked; January’s inflation rate would be roughly six percentage points lower.

Headline inflation would be 6pp lower if the average energy bill capped at the current level

Image Source: Macrobond, ING

As we see it, there are three main criticisms. The first is that fixing unit prices does little to incentivize consumers to reduce energy demand this winter (albeit there’s only a limited amount many households can do in this respect).

Secondly, it’s not targeted, though admittedly channeling support in an efficient manner in the time available is not a straightforward task. The sheer scale of the energy price shock means that most households will be paying more than 10% of their disposable incomes on energy without government intervention, which means some form of blanket support was always going to be required. Even within income brackets, energy usage can vary considerably depending on household size, making a targeted package harder to implement.

But that does mean it’s going to be very expensive. Energy providers will need to cover the shortfall between the capped price and wholesale costs, which we estimate will amount to roughly £70bn (or 3% of GDP) over the next year. That’s based on our expectations for Ofgem’s energy price cap, which in turn is based on futures prices.

The cost of fixing household energy prices below levels dilated by wholesale costs

Image Source: ING *Prices are for the average household on an annual basis. Calculations based on the total number of household customers and ING estimates of where the Ofgem regulated price cap in future quarters assuming no extra government support. For ease, we make the simplifying assumption that all households are duel-fuel direct-debit customers

That estimate falls to around £30bn if the government were to fix costs after October, once the planned 80% increase in household bills has taken place. Add to that the cost of supporting businesses, which Bloomberg News reports could amount to around £40bn.

But the key point is that these are just estimates – they aren’t fixed. They are based on futures prices today, and depending on the scheme’s final design, risk leaving the UK Treasury with an open-ended liability should wholesale energy prices surge once again.

Add to that the potential for additional tax cuts for households and corporates, and gilt markets are unsurprisingly nervous.

Extra government support is a double-edged sword for the Bank of England

A large portion of the move in UK rates this summer can be explained by investors ramping up rate hike expectations. The sheer scale of the government support being mooted is clearly influencing how hawkish rates market participants expect the BoE to be. The Gilt 2s10s curve inverting in August and the overnight swap curve pricing a terminal rate of nearly 4.5% are both indications that investors expect a robust monetary policy response to a new government support package.

We tend to agree with that assessment – even if we disagree with the scale of tightening being priced, not least because the introduction of a price cap is a double-edged sword for the Bank of England.

The fact that headline inflation will potentially be much lower in the near term should reduce fears about inflation expectations (at least among households) becoming less anchored. The YouGov/Citi measure of long-term expectations has risen to just shy of 5%, up from a pre-virus range of 3-3.5%. These surveys have a history of being closely linked to actual inflation.

We expect the Bank Rate to peak around 3% or a little below

But the Bank of England has also recently forecast a sharp rise in unemployment and a prolonged recession, helping to lower wage pressure and pricing power by 2024/5. All of that is less likely to happen under an energy price cap, and in theory that could lead to more tightening. That doesn’t necessarily mean a dramatically higher terminal rate but does mean that the BoE is less likely to start the firing gun on rate cuts in early/mid-2023, unlike some other central banks.

We expect the Bank Rate to peak around 3% or a little below (from 1.75% now), and we’re still inclined to say policymakers will opt for a 50bp rate hike next week over a more aggressive, 75bp move. Until August, the Bank had shown itself reluctant to move in larger increments. As other central banks have found, accelerating rate hikes sets a precedent for expected future moves, something we suspect the BoE won’t want to do. It’s also not clear yet how much of the energy plan will be announced before the next meeting, and the Bank typically operates based on whatever is formal government policy at the time of a decision.

That said, there’s little doubt the hawks will be worried about sterling weakness over recent weeks, so a more aggressive move shouldn't be ruled out. Another 50bp hike in November is also likely.

Energy package is a heavy burden for gilt markets to shoulder

Away from the Bank of England, the secondary but almost equally important aspect of the upcoming support package is how it is financed. News reports are mixed on this, so we’ll consider two extreme scenarios here, with the understanding that the ultimate financing of it will probably entail a mixed financing strategy.

In one extreme, the additional support could translate pound for pound into an equal about of gilt issuance. In the alternative, the treasury manages to shift the entire borrowing burden onto energy companies, for instance by guaranteeing loans granted by other lenders such as banks.

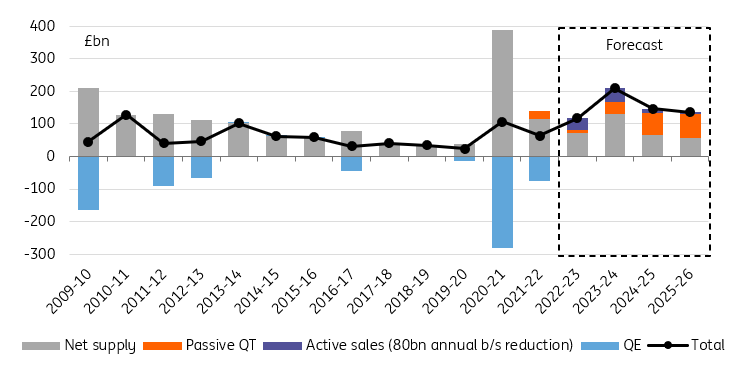

Private investors will be asked to buy a record amount of gilts in the coming years

Image Source: Debt Management Office, Bank of England, ING

From the point of view of gilt investors, any additional debt issuance would come on top of the planned deficit, on top of the cost of any additional tax cut, and on top of the extra amount of debt released into the hands of private investors by the BoE through Quantitative Tightening (QT). The cost of the energy package is still subject to much uncertainty but assuming £110bn (£70bn for households and £40bn for companies) spread equally between this and the next fiscal year, private investors will be asked to increase their exposure to gilts by a record amount (the black line on the chart above): around £120bn this year, and £210bn next.

Another consequence is that funding through gilt issuance is likely to have a much longer average maturity from the start. For instance, the average maturity of existing gilts is almost 15 years. Should energy companies borrow from banks, it is unlikely this will be at such an average maturity, and that banks will finance it with equally long liabilities, so the overall market impact on interest rates will be much lower.

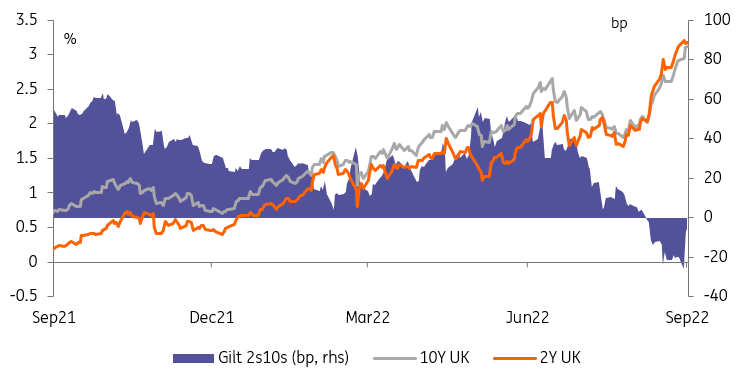

The re-steepening of the gilt curve may be in anticipation of greater supply

Image Source: Refinitiv, ING

Suffice it to say that the gilt market’s preference is for the energy package to be financed through other forms of funding. The question is whether lenders will be able to stump up such a sum in a short period of time, even helped by government guarantees. The re-steepening of the gilt curve suggests anticipated long-dated issuance, and the cheapening of gilts relative to swaps suggests markets are braced for at least some extra direct financing by the Treasury.

Markets are bracing for at least some extra direct financing by the Treasury

This in turn raises the issue of who in the private sector would be willing to increase their gilt issuance by such an amount. Inevitably, questions will be asked about the UK’s reliance on the ‘kindness of strangers' as its twin deficits widen.

Markets are already pricing in some increase in gilt supply. But don't underestimate the gilt markets’ ability to absorb more debt. At the start of FY 2020-21, the Debt Management Office planned to issue £156bn in gilts, it ended up selling £486bn. However, the more relevant metric here is the increase in net private investor exposure to gilts, which increased only £107bn that year, compared to £117bn and £210bn this and next year according to our forecast.

10Y gilts are already trading more than 150bp above the 10Y Bund to reflect this possibility. In the event where the majority of it is financed through issuance, we would expect this to rise to 200bp putting gilts above 3.5% in the coming weeks with both domestic and foreign investors spooked at the sharp increase in gilts outstanding, but also in foreign capital needs. We doubt this will be sustainable, however, and a decline to 2.5% in 2023 is still possible even in that scenario assuming the tone at the BoE turns progressively less hawkish.

GBP: Sovereign risk makes a comeback

Sterling has been grabbing the headlines for all the wrong reasons over recent weeks. Since early August, it has been under pressure not only against the mighty dollar but also against most of the currencies with which the UK trades. That puts the Bank of England’s broad trade-weighted sterling index back to the lows last seen in late 2020 and down nearly 4% on the month.

That sterling decline seemed to go hand-in-hand with the sell-off in the UK gilt market and also the relatively sharp widening in the UK’s sovereign Credit Default Swap (CDS). This is the cost of insuring against UK sovereign default. It is hard to avoid the conclusion that a UK sovereign risk premium has been going into the pound – presumably on doubts about at what price investors would be prepared to fund future UK borrowing plans.

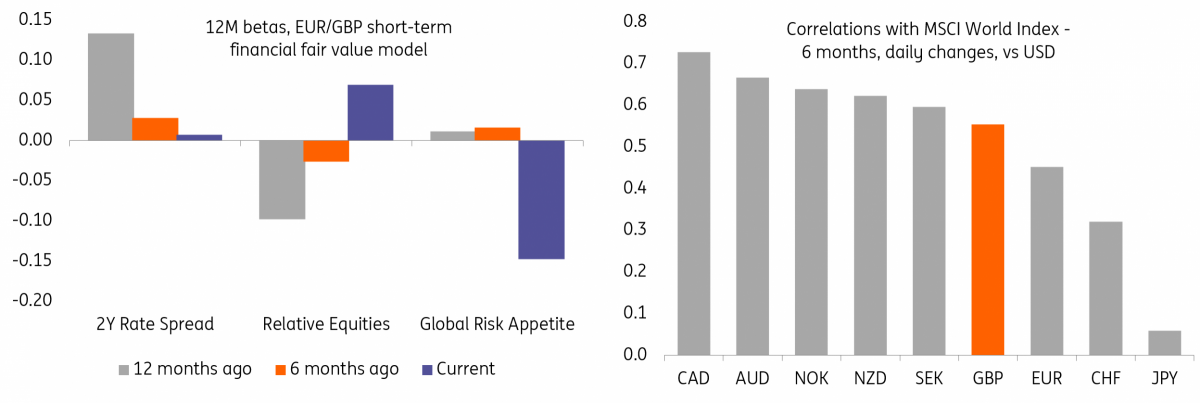

That the hawkish BoE policy has had little effect on supporting the pound can be seen by some of the betas in our Financial Fair Value (FFV) model. 12 months ago two-year rate spreads were the most important driver of EUR/GBP short-term valuation. Today it is global risk appetite and the relative performance of Eurozone versus UK equities.

And that should serve as a reminder that sterling can be considered a ‘pro-cyclical’ or ‘growth’ currency. Its correlation with global equity markets is more akin to the commodity currencies in the G10 space than to the more defensive currencies of the yen and Swiss franc. Driving that relationship is the UK’s large current account deficit (probably an overstated 8% of GDP in 1Q22) and the relatively large share of the financial sector in the UK economy.

Sterling's sensitivity to equities increases - and to rate spreads, decreases

Image Source: ING, Refinitiv

We do not think that sterling is particularly cheap at these levels based on our medium-term fair values. Indeed EUR/GBP looks around fair value. That means sterling would be vulnerable should some of the more extreme outcomes materialize for gilts, as we discuss above.

Our baseline forecasts see both GBP/USD and EUR/GBP trading around current levels into the end of the year. But the risks are skewed to the downside for sterling – perhaps for another 5% of independent sterling weakness.

EUR/GBP looks around fair value on our medium-term models

Image Source: ING, Macrobond

More By This Author:

FX Daily: 75bp Hike Seen In Canada, 25bp Hike Expected In Poland

Australian GDP Growth Remains Strong

Rates: Government Cash Management Set To Worsen The Euro Collateral Shortage

Comments

Log in or sign up to join the conversation.