Image Source: Pexels

November retail sales exceeded expectations as purchases continued to improve after a surprisingly weak September. Data indicates that private consumption, which hit a soft patch in 3Q24, improved again, remaining the main driver of economic growth in 2024. We see upside risk to our forecast of economic growth of 2.7% this year.

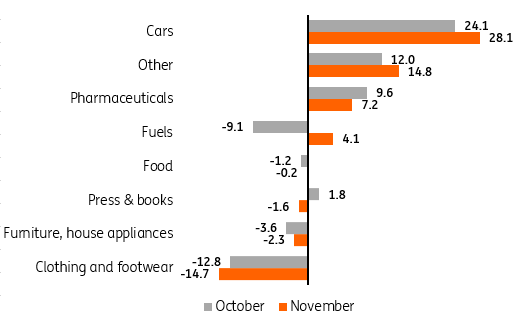

Retail sales of goods jumped by 3.1% year-on-year, surpassing the market forecast of 1.2% and our forecast of 1.0% as well as the increase of 1.3% in October. Seasonally adjusted data points to 1.0% month-on-month growth following a 5.6% MoM expansion in the previous month. In annual terms, the highest rise was reported in the sales of motor vehicles (+28.1% YoY). Demand for cars was robust throughout 2024 but started gaining momentum in 4Q24 ahead of new, more restrictive European emission standards coming into force in 2025. Buoyant growth was also reported in the “other” sales category (+14.8YoY), pharmaceutical sales (+7.2%YoY) and fuel sales (+4.1% YoY). However, sharp declines were still seen in clothing and footwear (-14.7% YoY), which suggests that some households are still postponing less urgent purchases.

Sales of motor vehicles gain momentum in late 2024

Retail sales of goods (real), %YoY

Source: GUS.

Following a surprisingly weak September, and some recovery in October, sales continued to rebound and in seasonally adjusted terms were close to August's level in November. The data indicates that private consumption has rebounded and should be stronger in 4Q24 after a disappointingly soft 3Q24 (+0.3% YoY). This is particularly important given the sluggish fixed investment this year, as private consumption is the main driver of domestic demand and economic growth this year. Economic growth in 4Q24 is likely to be stronger than the 2.7% YoY observed in 3Q24. Solid Christmas holiday sales may push both consumption and GDP growth above 3% YoY in 4Q24. We see upside risks to our forecast of 2024 GDP growth at 2.7%.

More By This Author:

The Commodities Feed: Stronger USD Prompts Oil Sell-OffEuropean Homeowners Decide With Their Wallets When It Comes To Energy-Efficient Renovation

The Yen Weakens As The BoJ Holds

Comments

Log in or sign up to join the conversation.