Image Source: Pixabay

Poland's central bank meeting is the key event and rates are expected to be increased further.

Poland's central bank to keep hiking

The negative short-term impact on GDP from the war in Ukraine is limited. With a high level of production backlogs, output growth remains high, but the contraction in new orders is significant, which bodes ill for the rest of 2022. Meanwhile, CPI is sticky and may be persistent, requiring further rate hikes to offset the fiscal expansion (c.3% GDP).

We believe the MPC will continue to raise rates, bringing the reference rate to the target level of 8.5% in late 2022/early 2023. With expansionary fiscal policy, we see rate cuts no sooner than 2024.

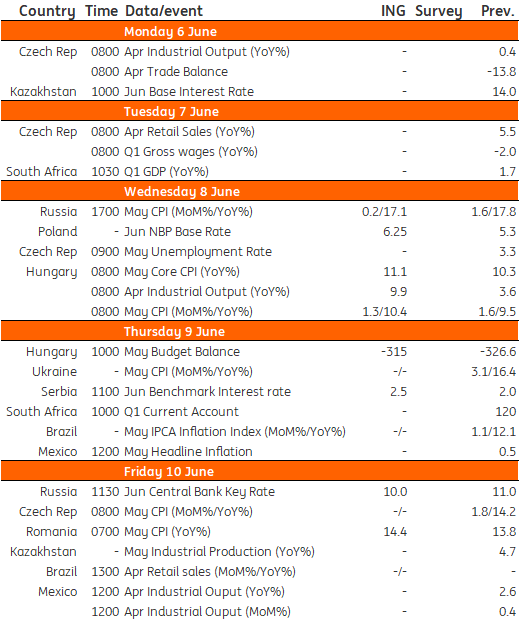

Key events next week

Image Source: Refinitiv, ING

Comments

Log in or sign up to join the conversation.