Image Source: Pexels

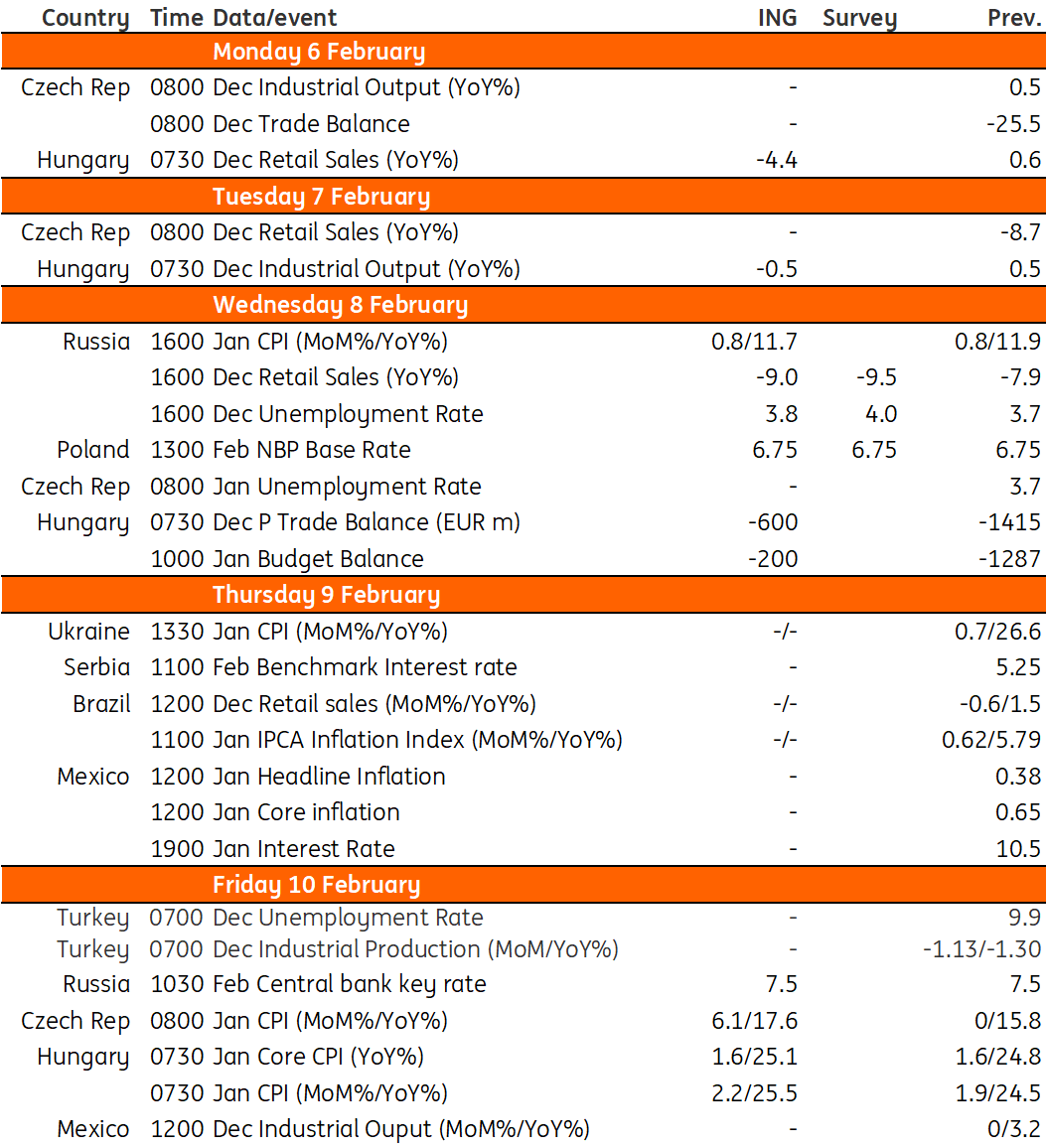

An action-packed week ahead for Hungary. As the government had abolished the fuel price cap, we expect signs of a downturn in retail sales and industrial production figures, while headline and core CPI move above 25% year-on-year. In the Czech Republic, we see headline inflation accelerating further to 17.6% year-on-year, while core prices remain at 13%.

Czech Republic: Spikes in CPI unlikely to influence the CNB's decision

In the Czech Republic, we expect CPI to increase by 6.1% month-on-month in January and hence the headline inflation likely accelerated further from 15.8% to 17.6% year-on-year. This increase was likely owing to the rise in regulated prices by around 40% YoY, while core inflation still remained strong at 13% YoY. This is in line with the new Czech National Bank (CNB) forecast. We see a risk, however, that some upward repricing was made later in January hence it will instead be reflected in the February CPI reading. Even a further spike in headline inflation is unlikely to persuade the CNB board to change its stance to keep rates unchanged at the next meeting in March.

Hungary: Data impacted by the abolishment of the fuel price cap

After a quite boring week, next week’s calendar will be action-packed. On Monday and Tuesday, the Hungarian Statistical Office is going to release the December retail sales and industrial production figures. We expect to see major signs of a downturn. In retail sales, the government has scrapped the fuel price cap, which has led to fuel sales falling off a cliff, while food and non-food retailers are suffering from lower demand due to the drop in household purchasing power. As the industry had two fewer working days to produce in December 2022 than a year ago, we expect the year-on-year performance to shrink, though the seasonally and working day adjusted print will show a slightly more favorable picture.

Wednesday will be about balances. We see the January budget balance in deficit due to a one-off expenditure item related to a publicly financed acquisition. Meanwhile, the December trade balance will bring some good news, as lower commodity prices will finally be filtering through the energy balance, as new energy contracts in the private and public sectors are following global stock prices with a two-month lag. Last, but definitely not least, Friday brings the first inflation print of 2023. We see both headline and core CPI moving above 25% year-on-year, mainly driven by a strong start-of-the-year repricing in food and services and the continued impact of the abolition of the fuel price cap. In contrast, price changes in household energy and durable goods will limit the upside in the acceleration, in our view.

Key events in EMEA next week

Image Source: Refinitiv, ING

More By This Author:

FX Daily: Eyes Back On Data After Fed And ECB Communication Troubles

Bank Of England Hikes By 50bp But Hints At Tightening Cycle Nearing Its End

Credit Squeezing Into Central Banks – What Next?

Comments

Log in or sign up to join the conversation.