Below-target inflation forecasts, more muted language on future tightening, and a warning about the impact of past rate hikes, all signal that Bank Rate is close to peaking. We expect one further 25bp rate hike in March, though we think a rate cut is unlikely for at least a year.

Further increases in both wage growth and service sector inflation were enough to convince Bank of England (BoE) policymakers to hike interest rates by a further half a percent this month. But it’s abundantly clear from both the press release and the new forecasts that the Bank is laying the groundwork for the end of the current tightening cycle.

For several months now, the Bank has been warning that it expects to continue hiking and that it could do so forcefully. The minutes of the last meeting confirmed that "forcefully" can be understood as meaning 50bp rate hike increments. So the fact that the Bank has dropped this reference suggests any future rate rises are likely to be smaller – and that’s further reinforced by an admission that the impact of past rate hikes is still largely to feed through to the economy.

The Monetary Policy Committee voted by a majority of 7-2 to raise #BankRate to 4%. Find out more in our #MonetaryPolicyReport: https://t.co/n7j94kKQlp pic.twitter.com/wudQD5gZy5

— Bank of England (@bankofengland) February 2, 2023

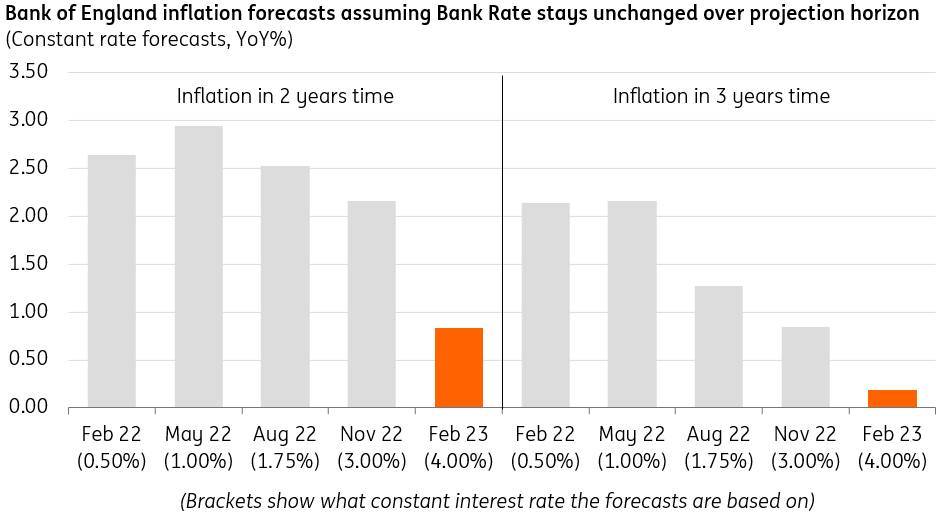

The Bank’s two-year-ahead inflation forecast – the time horizon over which BoE policy has the most impact – is now well below target. That's even true under an assumption that rates increase no further from here, though the impact of lower energy prices is also likely a driving factor.

BoE is forecasting below-target inflation in two and three years' time

(Click on image to enlarge)

Source: Bank of England

The counterpoint is that the vote split wasn’t particularly close, and seven out of nine policymakers backed today’s 50bp move. But as we warned in our preview, a large contingent of the committee has shown a tendency to act by consensus and move together. We therefore shouldn’t infer from today’s vote that a decision to slow the pace of hikes next time would necessarily be that divisive.

So what next? We are skeptical that today’s rate hike will be the last. The Bank says it would continue tightening policy “if there were to be evidence of further persistence [in inflation]”. Unlike the US, there are fewer signs that either wage growth or service sector inflation has peaked, and we’re unlikely to see this story change sufficiently to stop the Bank hiking again in March, albeit this time by a more modest 25bp. An additional move in May is possible if core inflation is still showing few signs of easing, though for now that’s not our base case.

Ultimately, a recession is still likely – albeit milder than first anticipated – and we think there are limits to how much higher Bank Rate can go without prompting more serious dislocations in the housing market and among corporate borrowers (SME lending is overwhelmingly done on floating interest rates).

That said, we think the BoE will be less rapid to turn to rate cuts than the Federal Reserve, given core inflation is likely to prove stickier. That suggests policy easing is unlikely for at least a year.

How our forecasts compare to market pricing

(Click on image to enlarge)

Source: Refinitiv, ING

Dovish BoE means further converge between GBP and EUR rates

The dovish theme running through today’s BoE communication comforts us in our view that sterling yield curves should now shed the hawkish bias acquired last summer. This should also add to the reluctance of sterling rates to rise (remember the Fed also turned less hawkish yesterday) but the most visible effect should be a further narrowing of the spread with euro rates, for instance at the 5Y point. For now, expect a further inversion of 2s5s as more cuts get baked in 2024 forwards, but it will become increasingly tempting for the curve to extrapolate this and price even earlier cuts. When this occurs, the stage will be set for re-steepening in the second half of 2023.

Euro and sterling swap rates to continue converging

(Click on image to enlarge)

Source: Refinitiv, ING

More By This Author:

Credit Squeezing Into Central Banks – What Next?

FX Daily: A More Relaxed Fed Powers The Rally

U.S. Slowdown Continues, Which Will Hit Jobs

Comments

Log in or sign up to join the conversation.