For The ECB, Only Next Year’s Inflation Matters

At next week's ECB meeting any changes to the communication and policy stance look unlikely. Nothing else matters – only the inflation outlook. If this outlook or the take on second-round effects changes, will the ECB significantly alter its course.

ECB President Christine Lagarde in Brussels

Last month, Metallica and millions of fans around the world celebrated the 30th anniversary of the black album, one of the most sold albums, cds or – for the younger ones – streams and downloads. The song ‘Nothing else matters’ is probably one of the most popular power ballads ever. We are not too sure whether Christine Lagarde really is a lover of hard rock or metal music as she once called the French electronic music band Daft Punk punk rock, but we do know that currently nothing else than the inflation forecast for next year matters to the ECB.

More dovishness over the summer

Over the summer, the ECB has clearly become more dovish with its new monetary policy strategy. The clear intention is to bring inflation expectations sustainably back to 2% and change forward guidance on interest rates. This new additional dovishness was confirmed by recent comments and interviews by Philip Lane and Isabel Schnabel, who mainly stressed that too low inflation was still a much more severe risk than too high inflation. Even if some ECB hawks reemerged over the last days, we don’t expect their pushback to be strong enough to deliver any changes to the ECB’s monetary policy stance and communication next week.

What to watch next week

Staff projections. A fresh round of ECB staff projections will in our view present slight upward revisions to growth and inflation for this year but hardly any changes for 2022 and 2023. In particular, the inflation outlook will be crucial. With the ECB’s new forward guidance on rates, we know that the ECB would not be satisfied if inflation returns to target in the year t+2, it has to be in year t+1. Also, given that the standard macro models do not capture a situation in which higher producer prices meet excess demand and excess savings, we doubt that the ECB will change its rather benign view of inflation being driven by a series of one-off factors without any second-round effects in sight. The ECB will rather stick to the narrative and analysis that second-round effects, be it from producer to consumer prices or from consumer prices to wages, are unlikely. In June, the staff projections expected GDP growth to come in at 4.6%, 4.7% and 2.1% in 2021, 2022 and 2023, respectively. Inflation was expected to come in at 1.9%, 1.5% and 1.4% over the same period.

Tapering. Any announcement of tapering will not be on the cards next week. However, the question is whether the ECB wants to communicate a very hypothetical exit plan between the lines. This is probably what the hawks have been pushing for with their latest comments. Don’t forget that the new forward guidance is on rates not asset purchases. In theory, asset purchases could be reduced even with a benign inflation outlook.

Defining the ‘P’. Looking for any tapering clues it will be important how the ECB defines the ‘P’ of the PEPP, which stands for pandemic and not permanent (asset purchases), and the end of the pandemic. Is it related to herd immunity, the number of infections, the economy returning to pre-crisis level or inflation returning to its pre-crisis path? Or something else. Up to now, the PEPP will run until March 2022.

Front-loading. Finally, we will watch closely whether or not the ECB extends the front-loading of its monthly asset purchases. With the eurozone’s vaccination campaign having reached 60% of the population being fully vaccinated, the economy returning to the pre-crisis level in the first half of next year, labour markets recovering swiftly, bond yields close to record lows and a weak euro exchange rate, question is whether front-loading to ensure favourable financing conditions is really still needed. This could be a very heated debate. Also given that Philip Lane recently said that the volume of asset purchases might become less relevant but that maintaining favourable financing conditions was more essential. However, as ending the front-loading would be perceived as de facto tapering by financial markets, we assume the ECB will stick to front-loading. Not so much as a conviction call but rather bourne out of the necessity not to start tapering before the Fed.

Indeed, monetary policy can hardly bring down inflation driven mainly by one-off factors. Therefore, the ECB’s current benign stance on inflation makes sense, even if some acknowledgement that people actually do have to pay higher prices would help future dialogues with eurozone citizens. Looking ahead to next week’s meeting, it is hard to see that the ECB will change anything in its communication and policy stance. Nothing else than the inflation outlook matters. Only if this outlook or the take on second-round effects changes, will the ECB significantly alter its course. Even if some Germans rather think of another Metallica song from the black album when they currently look at inflation: Enter Sandman.

For rates, it’s (mostly) about the APP

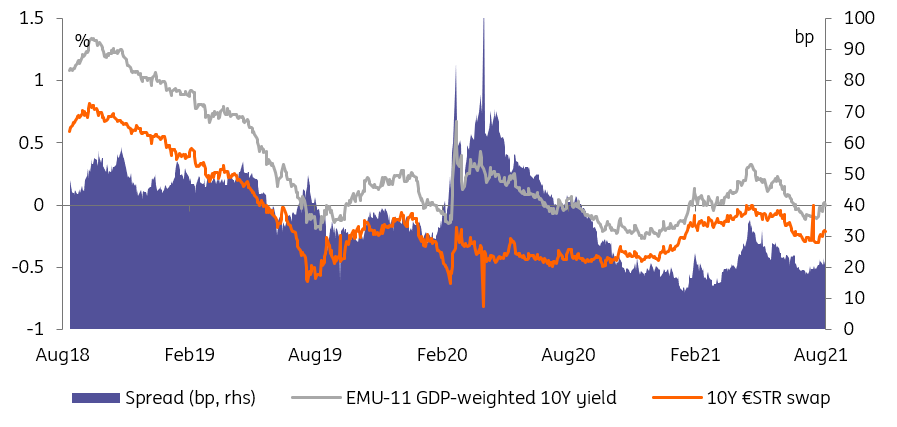

How the ECB communicates its decision regarding the pace of PEPP purchases (currently running at around €80bn/month) will make a world of difference to government bonds. The jump in yields in recent days is a sign that consensus is shifting towards a reduction, perhaps to the roughly €60bn/month that was carried out in 1Q21. Fundamentally, this shouldn’t make a huge difference to rates markets. The challenge is, as often, that investors will be tempted to extrapolate.

By itself, a reduction in PEPP purchases shouldn’t matter much to core rates

Source: Refinitiv, ING

After all, the ECB decides on the pace of purchases on a quarterly basis, and the programme has only two more quarters to run. A reduction will be seen by investors as a tacit acknowledgement that the programme is due to end at the planned date in March 2022. Assuming a further reduction to €30bn/month in 1Q22, this would leave only €75bn unused of the total €1,850bn ‘envelop’. Referring back to our Bund fair value model, this would only push yields up by 2bp compared to a scenario where the envelope is spent in full.

The more momentous decisions will concern the future of the other programme, the APP. Firstly, the ECB needs to decide before March next year whether to boost it when the PEPP expires. Secondly, it needs to decide whether the new rates forward guidance applies to the APP. Together, they could make a bigger difference to the rates fair value, as both the speed and duration of the APP programme are at stake.

The risk of a faster convergence to 0% in Bunds, and of wider spreads

In a PEPP tapering scenario, and where APP does not accelerate next year, we see roughly €314bn of purchases of government and SSA bonds in 2022, compared to around €500bn in net supply. Bear also in mind that it will come as the ECB faces repayment of TLTRO loans in the second half of 2022 when the special interest period expires. If the ECB tapers PEPP in September, markets will price this scenario with a much greater probability. This could not only result in 10Y Bund yields converging to 0% earlier than we forecast but, more importantly, in a higher volatility regime reflecting lower central banks support, including from the Fed.

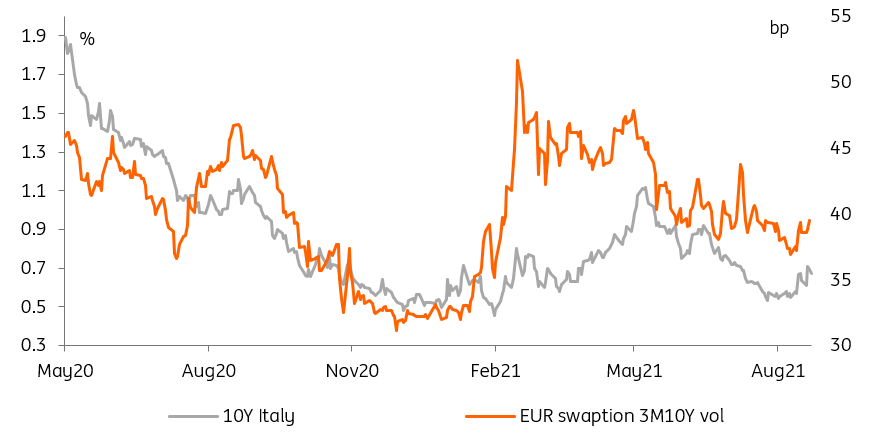

Italian yields are most sensitive to a jump in rates volatility

Source: Refinitiv, ING

As often, the bond markets most vulnerable to a rise in rates volatility will be the higher-yielding ones, such as Italy’s. When no idiosyncratic factor comes into play, as was the case in the past year, the two are closely linked. In a tapering scenario, and as inflation continues to climb pushed by base effects, 10Y Italian yields could easily scale the recent peaks of 1.1% in the coming weeks. Should the ECB provide reassurances as to the future of the APP, the spike will prove smaller in magnitude, and be short-lived.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more