The most aggressive central bank tightening cycle for decades is reaching its finale. This is our definitive guide to global central banks as we enter another round of crucial meetings over the next few weeks.

Freepik

The end of an era of aggressive tightening

There's a growing sense that the recent banking stresses will leave their mark on the global economy, even if the acute phase of the crisis seems to be over. Cracks are starting to form in the most interest-sensitive parts of the economy after what, in many cases, has been the most aggressive central bank tightening cycle in decades. Rate cuts are on the horizon, and we expect the first central banks to start loosening policy before the end of the year.

For now though, policymakers are satisfied they have the tools available to deal with fragilities in the financial system as they emerge, thus allowing monetary policy to remain focused squarely on inflation. Expect this narrative to prevail at the upcoming central bank meetings, particularly as inflation data continues to come in uncomfortably high across major economies.

With some notable exceptions, central banks across the developed world look poised to raise rates further in the short term. That's in contrast to Central and Eastern Europe and Asia, where policy rates have largely already peaked.

This article runs through our expectations for the next round of meetings, gives you the underlying rationale and, in an era of elevated uncertainty, the main risks to our calls.

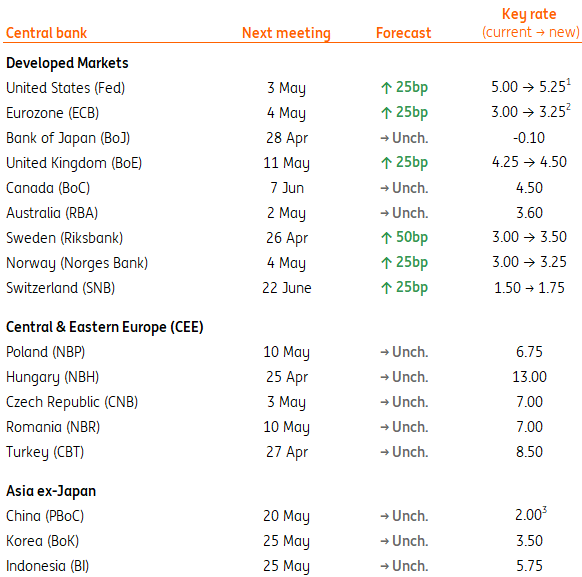

Our central bank forecasts at a glance

Source: ING forecasts

1. Fed Funds Upper Bound 2. ECB Deposit Rate 3. China 7-day Reverse Repo Rate

Developed market central banks

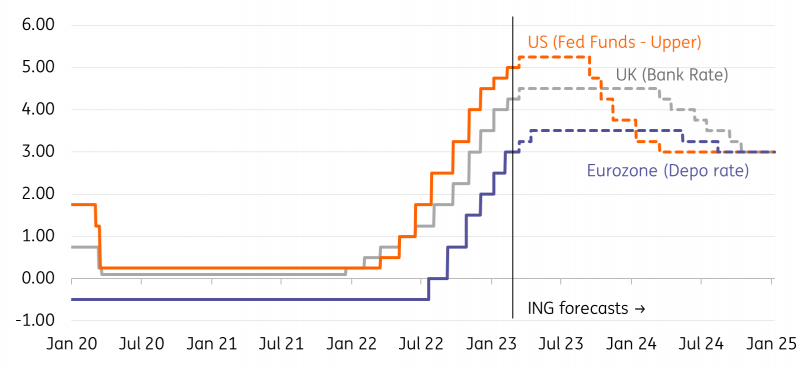

Major central bank forecasts

Source: Macrobond, ING

Federal Reserve

Our call: 25bp hike in May marks the top. A six-month pause and then 50bp of rate cuts in November and December, with Fed funds hitting 3% by the second quarter of 2024.

Rationale: After the most aggressive monetary policy tightening cycle in 40 years, cracks are starting to form. The housing market is deteriorating, business sentiment is in recession territory, and recent banking stresses mean lending conditions will tighten considerably. The chances of a hard landing for the economy are rising, which will mean inflation falls more quickly. The Fed’s dual mandate of price stability and maximum employment gives it the flexibility to respond swiftly with rate cuts.

Risk to our call: Persistent service sector inflation caused by labour market tightness could see the Fed hike for longer. Conversely, the tighter lending standards, a debt ceiling crisis/government shutdown and a restart of student debt repayments may create an even deeper downturn that triggers a more aggressive Fed rate cut response.

James Knightley

European Central Bank

Our call: 25bp hike in May and a final 25bp hike in June. The first rate cut will not be before the second half of 2024.

Rationale: The ECB no longer wants to be the unconditional lender of last resort for financial markets, eurozone governments or the area's economy. Even though headline inflation will come down further, sufficient pipeline pressure in services and stubbornly high core inflation argue in favour of more rate hikes and a ‘high for longer’ approach. Even if monetary policy tightening further undermines the economic outlook for the eurozone, the ECB will not consider any reversal of the current stance until both projected and actual inflation are clearly moving towards 2% again.

Risk to our call: In a more benign economic environment, the ECB could hike rates further than the currently expected 50bp. On the other hand, a sharper drop in inflation and an abrupt easing of monetary policy in the US could force the ECB to loosen monetary policy in early 2024.

Carsten Brzeski

Bank of Japan

Our call: Policy rate hikes are unlikely this year, but adjustments to the Yield Curve Control are possible as early as June. One option would see the BoJ target 5-year government bond yields (JGBs) instead of the current policy, which caps 10-year yields at 0.5%.

Rationale: With strong wage growth and a modest service-led recovery, core inflation is expected to stay above the long-term average in 2023. There will also be growing calls to correct distortions in the bond market. So, the BoJ should eventually adjust or abandon the YCC policy during the year and pave the way for policy rate normalization in 2024.

Risk to our call: The BoJ is concerned about the economy returning to deflation. The BoJ will carefully examine if the strong wage growth is just a one-off event this year before deciding whether to postpone the policy change to next year.

Min Joo Kang

Bank of England

Our call: 25bp rate hike in May, followed by a pause. No rate cut this year.

Rationale: It had looked like the Bank of England was done with its tightening cycle and, in recent comments, various officials have sought to keep options open. But the Bank has said that if fresh signs of “inflation persistence” emerge, it could hike further. Remember, recent wage and CPI data both came in above expectations and suggest another increase should be the base case for May. That said, policymakers have been explicit that much of the impact of past hikes is still to feed through, so we think the bar to further tightening beyond May remains high.

Risk to our call: If services inflation continues to trend higher and recent survey evidence showing reduced price pressures begin to revert, then the Bank could go further – though the three or four rate hikes markets are currently pricing appears extreme.

James Smith

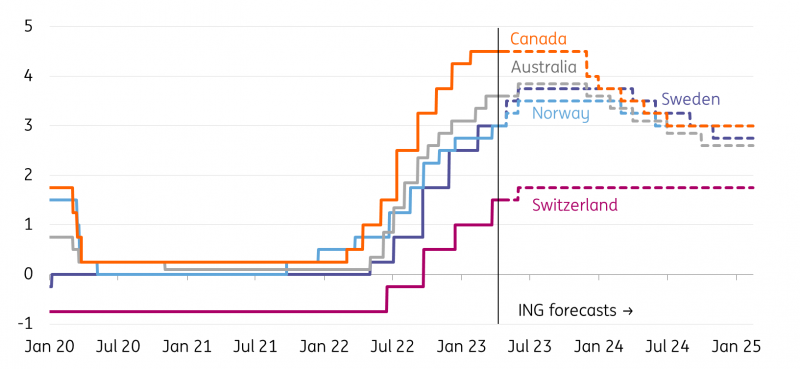

Rest of G10 - central bank forecasts

Source: Macrobond, ING

Bank of Canada

Our call: Canadian rates have peaked at 4.5%, with the first rate cut coming in the fourth quarter of 2023. Policy rate to be cut to 3% in 2024.

Rationale: The labor market is tight, yet inflation is slowing more quickly than the BoC expected. Canada is more exposed to central bank interest rate changes than the US, given that mortgage rates are fixed for a shorter duration with millions of households subject to rate resets at higher levels this year and next. Canada’s high exposure to the US via financing, exports and commodity prices adds to the downside risks for the domestic economy and inflation.

Risk to our call: The BoC is wary that while inflation is falling quickly, the tight jobs market and sticky inflation expectations mean it can’t signal the all-clear. Nonetheless, there appears little inclination to restart rate hikes with the BoC’s acknowledgement that policy is “restrictive”; it's held the policy rate at 4.5% since January.

James Knightley

Reserve Bank of Australia

Our call: No change.

Rationale: Having paused its rate tightening in April to gather more information, the RBA will likely see a further fall in inflation rates which will not provide any justification for additional tightening at this meeting.

Risk to our call: Volatile data, such as labour market figures, might create a more confusing picture for the RBA than the inflation figures alone, but it is hard to see these being sufficiently bad to justify an additional increase. Our 3.85% peak rate looks like it will have to be revised down shortly to be consistent with a more rapidly declining inflation path than the RBA itself is predicting (it doesn't see inflation settling back to target until 2025, which we believe is utterly wrong.)

Rob Carnell

Riksbank

Our call: 50bp rate hike in April and potentially another 25bp in June.

Rationale: The Swedish economy is undoubtedly struggling, and the housing market is now down 15%, given the high prevalence of variable-rate mortgages. But for now, core inflation is well above previous Riksbank forecasts, and the committee is visibly concerned about SEK weakness and its implications for future inflation. The central bank only has five meetings a year, so has to make each one count, and it has signaled it wants to stay out in front of the ECB. Still, there’s only so far that logic can go as interest rate-sensitive parts of the economy come under pressure. Read our full preview here.

Risk to our call: Heightened concern about a weak SEK dominates all other considerations, and rates go to 4% or above.

James Smith

Norges Bank

Our call: Two more 25bp rate hikes during the second quarter.

Rationale: Ongoing NOK weakness, amongst other things, saw Norges Bank add in an extra couple of rate hikes into its projections back in March. Since then, the story hasn’t changed hugely. The trade-weighted NOK has stabilized, and core inflation is roughly in line with projections. As a result, there’s currently no reason to doubt Norges Bank’s guidance that we’ll get two more 25bp hikes before a pause.

Risk to our call: Further NOK weakness and/or a renewed spike in global rates prompts rates to go towards 4%.

James Smith

Swiss National Bank

Our call: A final 25bp rate hike in June and then a long pause.

Rationale: After a rise at the beginning of the year, inflation in Switzerland fell sharply in March, from 3.4% to 2.9%, and the decline is expected to continue in the coming months. That, and the risks to financial stability, should prompt the SNB to make a final rate hike of 25bp in June, smaller than previous hikes, to bring its key rate to 1.75. This would bring the total tightening to 250bp, far less than in other developed economies. It is then expected to keep its rate unchanged until the end of 2024.

Risk to our call: If inflation proves more persistent than expected, the SNB rate could rise further to 2%.

Charlotte de Montpellier

Central and Eastern Europe central banks

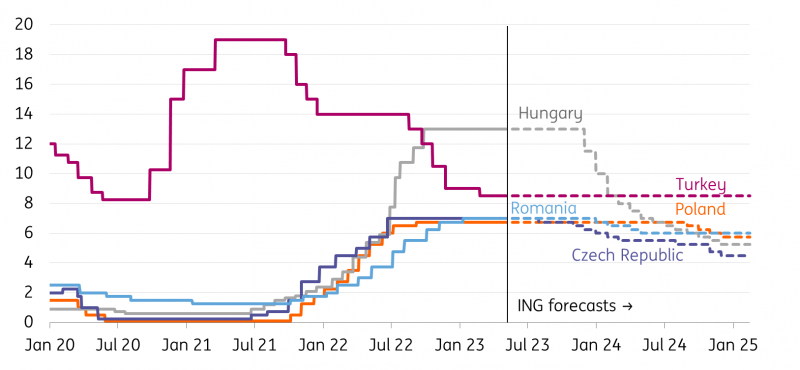

CEE - central bank forecasts

Source: Macrobond, ING

National Bank of Poland

Our call: No room for rate cuts this year. Monetary easing to start in the third quarter of 2024.

Rationale: The monthly growth of core inflation is as high as in the worst months of 2022, despite a fall in consumer spending over the last two quarters. That presumably is what prompted the Monetary Policy Council to amend its communication and no longer flag a willingness to consider rate cuts in late 2023. Prices are sticky, and disinflation is taking place mainly on the back of the reversal of higher energy prices. Inflation is far from being contained, and policymakers cannot afford to ease policy despite signs of weakness in the real economy. While the drop in headline inflation is likely to be fast in the near term, it will slow, and the NBP’s target of 2.5% (+/- 1 percentage point) is not in sight any time soon. The NBP March macroeconomic projection, which assumed unchanged interest rates, envisages CPI returning to target no earlier than 2025.

Risk to our call: A global slowdown induced by a credit crunch or a faster-than-expected slide in local CPI may prompt the NBP to deliver rate cuts in 2H23, the market is betting. This would be marginally negative for PLN (with a structural current account improvement at the same time).

Adam Antoniak and Rafał Benecki

National Bank of Hungary

Our call: A dovish pivot is in the making.

Rationale: The NBH made a marked difference between the base rate and the Temporary Targeted Tools (TTT) introduced in mid-October 2022. The base rate takes care of price stability. As the fight against inflation will be a long one in Hungary, we don’t see a change in the base rate until late 2023. The effective instrument is the overnight quick deposit (part of TTT), and it is there to have ultimate control over market stability. Recent positive developments in market stability have opened the door to a monetary policy pivot. It will start with a huge cut in the overnight repo rate in April, followed by a rate cut cycle affecting the 18% effective rate in May or June. For an in-depth look, read our NBH Preview here.

Risk to our call: Stickier core inflation and worsening risk sentiment could only delay the inevitable easing cycle.

Peter Virovacz

Czech National Bank

Our call: Hawkish, limited scope for rate cuts in 2023.

Rationale: Inflation remains high and above target, and the CNB wants to see progress in taming inflation before it starts the process of interest rate normalization. New board members have even mentioned the possibility of a rate hike if wage growth remains too high, presenting a risk of a wage-inflation spiral. It seems likely the normalization of interest rates will start only when inflation markedly slows down.

Risk to our call: If wage growth markedly exceeds 10%, then the CNB could even flirt with a rate hike.

Vojtech Benda

National Bank of Romania

Our call: On hold at 7.00% for the rest of 2023, first rate cuts in early 2024.

Rationale: Unless a serious recession occurs (currently unanticipated), the NBR is most likely to wait for a consolidation of the current disinflationary trend before making its next move, with real positive rates possibly being the trigger for switching to rate cuts. We think this is possible in the first quarter of 2024. In practice, the central bank has already switched to a looser policy stance by tolerating a historically high liquidity surplus in the money market. This has been pushing market rates below the key rate and made the 6.00% deposit facility more relevant than the 7.00% key rate.

Risk to our call: Geo-politics (and its side-effects) aside, we pay close attention to other regional central banks' behaviour (especially the NBP), while internally, the fiscal side of the policy mix shows some signs of weakness as revenues undershoot expectations in 1Q23.

Valentin Tataru

Central Bank of Turkey

Our call: May elections are a key catalyst for the rate outlook.

Rationale: While the current account deficit has continued to expand, the data also signal a challenging external financing environment, given that almost all the deficit was financed through reserves, as inflows from errors and omissions stopped. For inflation, the extra fiscal burden of reconstruction costs and the CBT’s supportive stance will likely create further pressure on already elevated headline inflation. We have seen a widening in the budget deficit, rising to 2.4% of GDP on a 12-month cumulative basis vs 0.9% at the end of last year. These indicators point to a need to rebalance the economy.

Risk to our call: The current policy setup relies not only on low interest rates but also a selective credit policy and “liraisation strategy”. The election outcome will determine whether we will see the preference for low interest rates continue or see a shift to monetary policy normalization with an adjustment in the policy rate.

Muhammet Mercan

Asia ex-Japan

Asia (ex Japan) - central bank forecasts

Source: Macrobond, ING

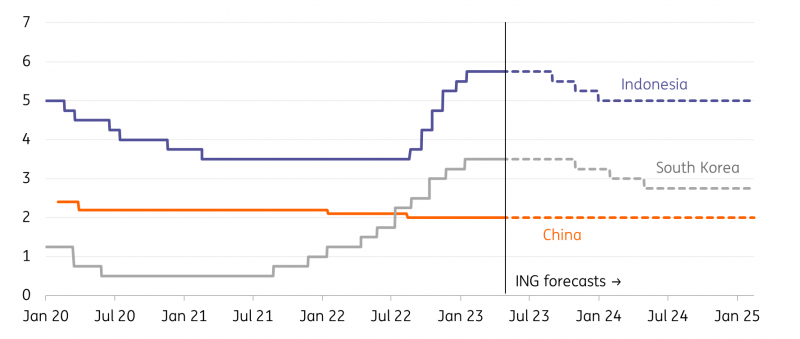

People’s Bank of China

Our call: No more easing from the PBoC unless the economy unexpectedly deteriorates.

Rationale: GDP grew faster than expected at 4.5% year-on-year in 1Q23, and retail sales jumped 10.6%YoY in March, signalling that the domestic economy is on track to recover.

Risk to our call: Exports from China have generally been contracting even though the data point in March showed a rebound. Weakening export demand could put pressure on wages in the manufacturing sector and slower consumption growth nearer the end of the year. The PBoC might pre-emptively lower interest rates and/or inject extra liquidity by cutting the Reserve Requirement Ratio to support infrastructure projects. This should help local governments suppress interest costs to deliver the investments, with their fiscal ability still weak in the middle of the recovery.

Iris Pang

Bank of Korea

Our call: The BoK is done with hiking at current rates of 3.50%, with the first rate cut coming in the fourth quarter of this year.

Rationale: Inflation is expected to head down towards 2% throughout the year.

Risk to our call: The BoK is expected to remain hawkish for the time being due to uncertainty surrounding global commodity prices. If inflation becomes stickier than expected, a BoK cut could come later next year.

Min Joo Kang

Bank Indonesia

Our call: Bank Indonesia kept rates unchanged at 5.75% earlier in the year, but rate cuts will only likely happen by late 3Q.

Rationale: Price pressures have faded somewhat, but headline inflation remains well above target. This should delay potential easing to around September.

Risk to our call: A more pronounced drop in inflation and a further strengthening of the Indonesian rupiah could open the door for the central bank to bring forward its first rate cut to early in the third quarter.

More By This Author:

FX Daily: European FX showing Some Resilience

The Commodities Feed: Brent Declines

Asia Week Ahead: Bank Of Japan’s First Meeting With New Governor

Comments

Log in or sign up to join the conversation.