Image Source: Pixabay

Next week’s data calendar features several economic activity data from Korea, inflation from Japan, Singapore, and Australia, job and growth data from Taiwan plus PMI data from China. Japan's central bank will meet for the first time under new governor Kazuo Ueda.

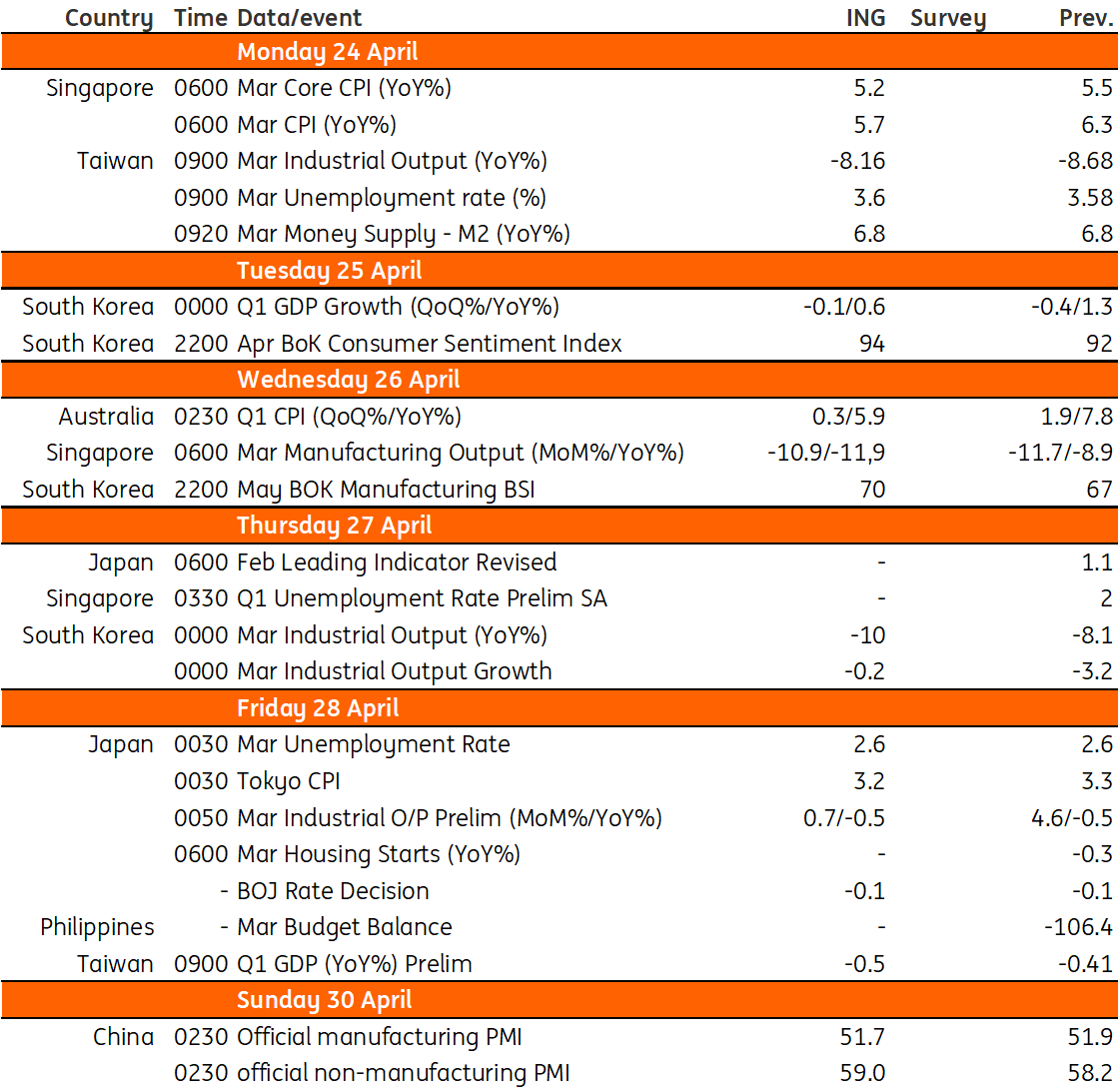

Inflationary pressures expected to ease in Australia

March inflation will probably fall substantially on base effects alone, as March 2022 saw a 1.1% month-on-month increase following Russia’s invasion of Ukraine and the resulting spike in energy and agriculture prices. But we may also have some additional help from volatile food prices, which rose 1.0%MoM in February, but will probably ease back to something closer to 0.3-0.4% in March.

Some additional decline in alcohol and tobacco prices may provide a further pushdown, and offset slightly higher gasoline prices for the month, resulting in a total CPI index increase of 0.3 %MoM, and 5.9% year-on-year, down from 6.8% in February. This should be enough to at least put the Reserve Bank of Australia on hold at the April meeting. And may also be enough to draw a line under this entire rate-tightening cycle.

Weak semiconductor demand could hinder Korea’s economy

We expect first quarter GDP to post a mild contraction of -0.1% quarter-on-quarter seasonally adjusted (vs -0.4% in 4Q22) mainly due to sluggish exports and investment. Weak global demand for semiconductors is a major reason behind this development. However, private consumption and construction are expected to hold up relatively well despite higher borrowing costs and a sharp decline in real estate, while inventory also contributes positively to growth.

We believe March industrial production will contract again as we expect that chipmakers cut production further in March to unload inventory. Meanwhile, the increase in auto sector activity should partially offset the overall decline.

Meanwhile, sentiment survey data is expected to improve as the Bank of Korea maintained its policy rates and market rates have fallen gently. China’s reopening, as well as the calming of financial market jitters triggered by the banking sector, have also probably helped to boost consumer and business sentiment.

Ueda’s first meeting as Bank of Japan governor

The Bank of Japan (BoJ) will hold its monetary policy meeting on 27 and 28 April, the first time under Governor Kazuo Ueda, amid speculation about the timing of the monetary policy adjustment. We believe the BoJ will opt to keep all settings untouched given the recent banking sector jitters in the US and Europe. Yet, it is still worth watching how the new governor will shape his views on monetary policy and macroeconomic conditions.

The BoJ will also release its latest macro outlook report. The key takeaway will be the inflation forecasts and whether the BoJ sees inflation undershooting its 2% target in the near future, which will give us more hints about the BoJ’s reaction to the CPI in coming meetings.

Other than that, Tokyo CPI inflation is expected to cool down further in April while labor market conditions are expected to remain solid mainly led by the service sector. March industrial production is expected to slow on the back of the weak global demand for IT products.

The gloomy economic outlook for Taiwan

Taiwan will release its first quarter GDP report next Friday, and we expect a mild contraction of 0.5%YoY from a 0.41%YoY contraction in 4Q22. This should mean that Taiwan fell into a recession in the first quarter. The dip in semiconductor demand has hurt the economy in terms of production and exports. We will wait to see the negative impact on industrial production in March and we expect another contraction of around 8%YoY in March after an 8.7% contraction in February.

The unemployment rate in Taiwan should therefore edge up to 3.6% in March from 3.58% in February. All of this points to a gloomy outlook for Taiwan. However, there is a low base effect for the second quarter, which should help GDP growth turn positive again. This technical rebound may not imply improvements in global demand for semiconductors as the US economy is slowing.

Upcoming PMI data from China

China will release official manufacturing and non-manufacturing PMIs on 29 April. We expect services to grow faster than manufacturing activities as there was a short holiday in April, and tourism-related activities increased. Meanwhile, manufacturing activities could grow slightly slower in April due to the shorter month.

Inflation to trend lower in Singapore

Singapore reports March inflation next week and we expect both headline and core inflation to moderate from the previous month. Headline inflation could settle at 5.7%YoY from 6.3%, while core inflation could dip to 5.2% from 5.5%. Slowing inflation could be one of the reasons why the Monetary Authority of Singapore (MAS) opted to retain policy settings last week after growth disappointment. We can expect inflation to grind lower in the coming months but given that it remains well above the central bank’s target, the MAS may be limited in its ability to ease settings to help support sagging growth momentum.

Key events in Asia next week

Image Source: Refinitiv, ING

More By This Author:

FX Daily: A Glimpse Of Future Easing

Looking Past The Peak Of Fed Key Rates

FX Daily: Time For Some Stabilization?

Comments

Log in or sign up to join the conversation.