Image Source: Pixabay

Today, you can discover some Canadian low yield stocks that even retirees would like because of their solid growth potential. So, what if you’re decades away from retirement? Well, they could be great for you, too. None of the usual suspects are included this time, though -- so no Alimentation Couche-Tard, Canadian National Railway, or TFI International. Curious? Well then, keep reading.

Why Low Yielders?

By selecting the right low yield stocks, you can enjoy both sustained dividend growth that exceeds inflation, as well as capital appreciation. Actually, low yield, high growth stocks often outperform more mature, high-yielding stocks in the long run, thus securing your retirement whenever that might be, as I have previously explained.

The good news is that there are plenty to choose from, and in different sectors. If you have a retirement portfolio, they can complement your income stocks often found in the Utilities, REIT, and Financials sectors, and may improve your diversification. Growth investors still in their accumulation phase will also reap the benefits.

For each stock I selected below, I will tell you why I like the stock, and include a graph showing the stock price evolution over 10 years along with the dividend triangle (the revenue, earnings per share, and dividend payment trend over 10 years). I also highlight some risks the companies may face.

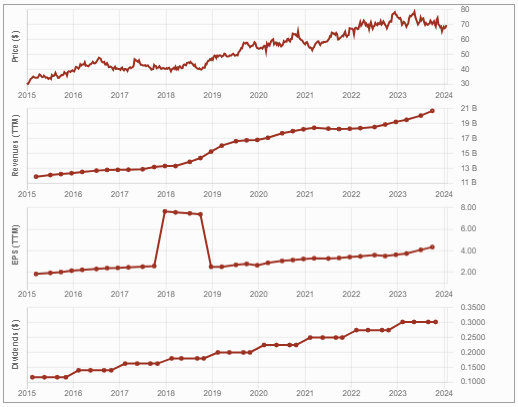

Metro (MTRAF) – Consumer Staples

Metro is the smallest, yet fastest-growing, grocery store in Canada. Metro focuses on the Quebec and Ontario markets, where population growth and the economy are quite healthy. Metro has emphasized its private-label brands, which sell for 20% less than original brand products. In a world where price is the main consumer driver, this is a key advantage.

Metro is also pushing its online services to gain customers. The grocer is impressive, as it increases sales while keeping expenses under control in this high inflation environment. So far, Metro has kept healthy margins, and benefits from higher inflation to boost its sales.

MTRAF Dividend Triangle

Metro also profits from its strong Brunet and Jean-Coutu drugstore network. However, with 71% of its food stores and 82% of its drugstores found in Quebec, there’s limited growth opportunities there; Metro must expand in other provinces where competition is fierce. Finally, Metro could unlock more value by spinning off its real estate properties.

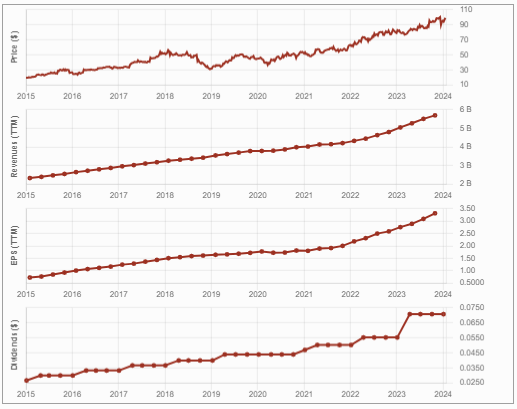

Dollarama (DLMAF) – Consumer Discretionary

You won’t be able to pay your utility bills with your Dollarama’s dividend yield. Management hasn't shared the wealth with shareholders yet, mainly because it sees so many growth opportunities. By acquiring 51% of Dollarcity, Dollarama has international growth potential in Latin America. At the same time, Dollarama continues to enjoy a stable Canadian economy, with over 1500 stores in the country.

With a possible recession looming, Dollarama is definitely a stock to look into. Many Canadians shop at Dollarama regularly to cut down their expenses. The company generates high gross margins (44%) on the many private label products (63%) it sells. The company’s growth plan is to open more stores and expand in Latin America.

Although Dollarama dominates in Canada, similar U.S. chains (e.g., Dollar Tree) are eyeing the Canadian market. Latin America shows strong potential, but comes with volatility due to occasional political and economic instability. Another problem is pressure on margins due to inflation making it harder to sell inexpensive items, even with large volumes. So far, Dollarama has proven to be highly resilient, and it displays a strong dividend triangle.

DLMAF Dividend Triangle – Constant Upwards Trend

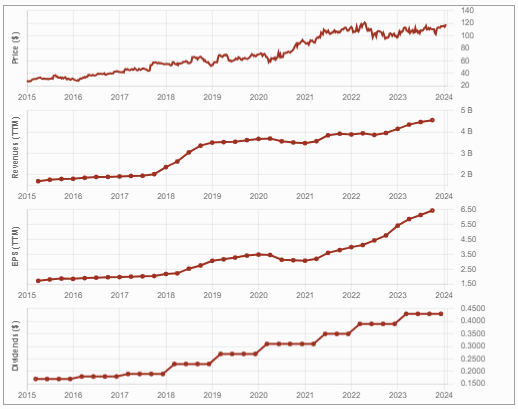

Toromont Industries (TMTNF) – Industrials

If you want to make a play on infrastructure spending, Toromont could be a good candidate. Toromont is one of Caterpillar’s largest dealerships in Canada. Toromont covers industries from roadbuilding to mining and telecommunications to food and beverage processing.

In addition to relying on mining (20%) and construction (38%) to grow organically, Toromont also buys smaller dealerships, such as Hewitt (acquired in 2017). Revenue growth wasn’t impressive since the height of the pandemic, but it has picked up in the recent quarters.

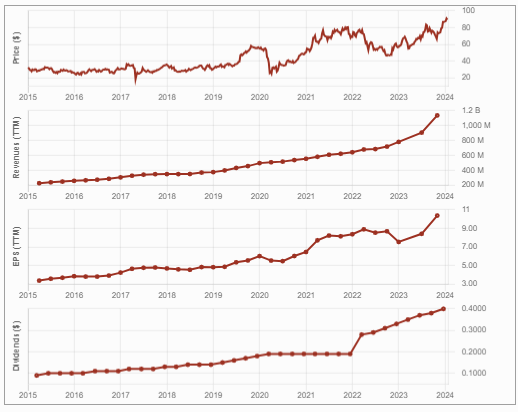

TMTNF – Revenue Growing Again, Strong Earnings Growth, & Steady Dividend Increases

Toromont continues to face construction delays and inflationary pressure. Its mining and construction customers have cyclical and capital-intensive businesses that are sensitive to high interest rates and a slowing economy. A recession would cause weaker results.

Considering the massive infrastructure spending needs in Canada in the coming years, though, Toromont could do very well.

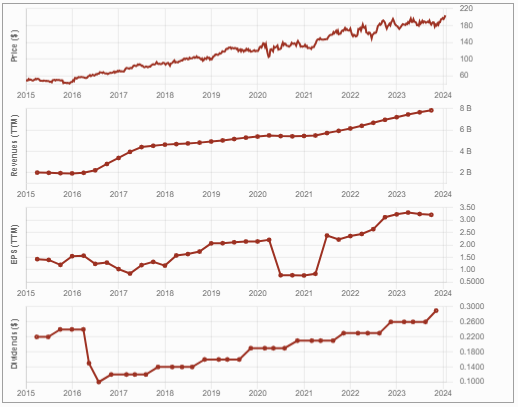

Waste Connections (WCN) – Industrials

An integrated solid waste services company, Waste Connections provides non-hazardous waste collection, transfer, and disposal services, as well as resource recovery through recycling and renewable fuels generation. So long as we consume stuff, demand will be high for Waste Connections' services. Waste Connections is a classic “I like this business, but it’s too expensive” play.

The company shows an impeccable dividend triangle as it continues to grow by acquisition. Management has been adept in integrating their acquisitions. Therefore, it’s not only growing, but becoming more profitable.

WCN – Strong Dividend Triangle

EQ Bank (EQGPF) – Financials

This company supplies diversified banking services through its EQ Bank platform and has two divisions: Personal Banking and Commercial Banking. Its non-conventional business (including online presence and reverse mortgage products), along with its aggressive dividend growth policy, made EQ Bank popular among investors. The innovative bank shows impressive growth across all loan products and deposits over the past five years.

EQ Bank built a fast-growing business while being surrounded by giants. This small fish in a big pond is going for quickness, simplicity, and seamless digital banking. Let’s just admit the big six are decades behind in that regard. While I’m a big fan of National Bank, I must admit that EQB shows quite the record in the past few years.

EQGPF – Small Player Finding A Lot Of Growth In Canadian Banking

EQ Bank has a very strong dividend triangle, but keep in mind that higher interest rates have a lagging impact on the economy. Make sure it just doesn’t look good on Prom night; review quarterly results to detect growth slowdowns or higher provisions for credit losses.

Final Thoughts

As a dividend growth investor, I prefer low yield, high growth stocks. Retirees often hesitate to buy such stocks for various reasons, as some explained in a previous article. I believe that income-seeking investors benefit immensely by having a balance in their portfolio between low yield, high growth stocks and more traditional, high yield stocks.

More By This Author:

Buy List Stock For February 2024: American TowerWhy Not Simply Invest In ETFs?

Best Income Stocks 2024

Comments

Log in or sign up to join the conversation.