Canadian Household Leverage Has Been On The Decline For A Decade

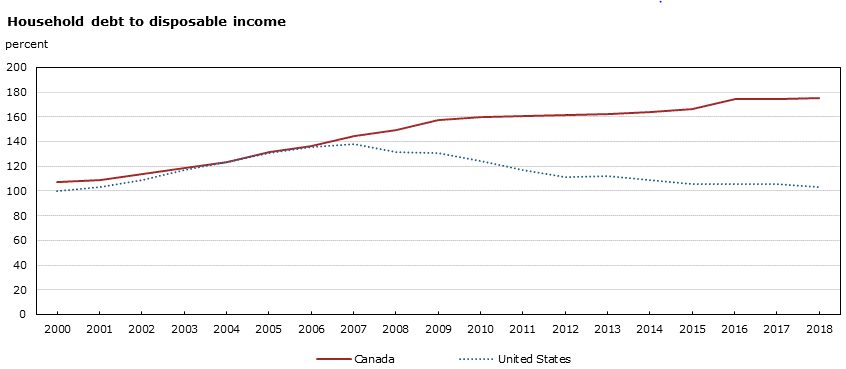

A constant theme running through the financial press is that Canadians are deep in debt, that we are heading for a major debt crisis and that the government should do something about curtailing the growth of household indebtedness. This view is reinforced by statements from the Governor of the Bank of Canada, fretting over the household debt and the need to monitor debt levels in setting monetary policy. And, indeed, the debt-to-income levels among Canadian households has steadily edged higher over the past decade following the 2009 financial crisis. The ratio rose sharply in 2015-2016, as oil prices collapsed, and has since leveled off. In particular, the financial pundits have zeroed in on the average household’s ability to manage debt loads, particularly mortgages, in the face of rising home prices and a slowdown in wage growth. Household spending has been the driving force behind economic growth. So, should the consumer stumble because of high debt levels, economic growth will decline. Unfavorable comparisons are constantly made to the U.S. indebtedness which has persistently declined since the 2008 financial crisis.

But is debt-to-income a valid measure of the systematic risks in Canada? The measure is seriously flawed because it measures one year’s income against debt that has many years to be amortized. Economists avoid using measures that compare a “stock” such as debt with a “flow” such as yearly income. After all, no one is expected to pay their mortgage off in full within a year, so measuring the outstanding debt against one year’s income reveals very little about risk-taking by the borrower. So, what should be the relevant measure of indebtedness for a household?

(Click on image to enlarge)

Figure 1

In a rare admission by a major bank president, Bank of Montreal chief executive Darryl White, referring to the issue of household indebtedness, stated:

I think the most important point to think about is when you look at household indebtedness, you also have to consider the other side of the household’s balance sheet. We’re also seeing the other side of the household’s balance sheet with liquid investments, illiquid investments, and the wealth effect is very positive. [1]

The Canadian banks are the largest supplier of household mortgages and if they seem comfortable with household balance sheets in support of outstanding debt, then the hand-wringing expressed by analysts is completely misplaced.

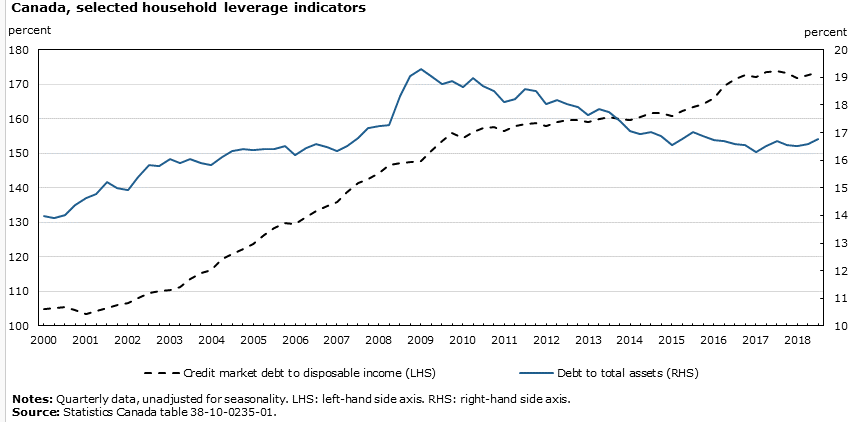

So, let's examine leverage in the economy. Figure 2 traces the growth in household leverage since 2000. Leverage grew steadily from 2000 to 2008, then surged in 2008-9 in response to the financial crisis. It has steadily declined to the point where the leverage is now back to the level of 2007. Put simply, Canadians have reduced their exposure to debt for nearly a decade and thus have reduced any systematic risk.

The Bank of Canada loathes dropping the bank rate to support economic growth because it fears an outburst of consumer borrowing. But we see that, independently, a process of de-levering has been underway for several years, despite historically low-interest rates.

(Click on image to enlarge)

Figure 2

[1] Job cuts to household debt woes: One-on-one with BMO's CEO

Interesting article, prof. We wish Canada well.